India EV Market: Current Analysis and Forecast (2025-2033)

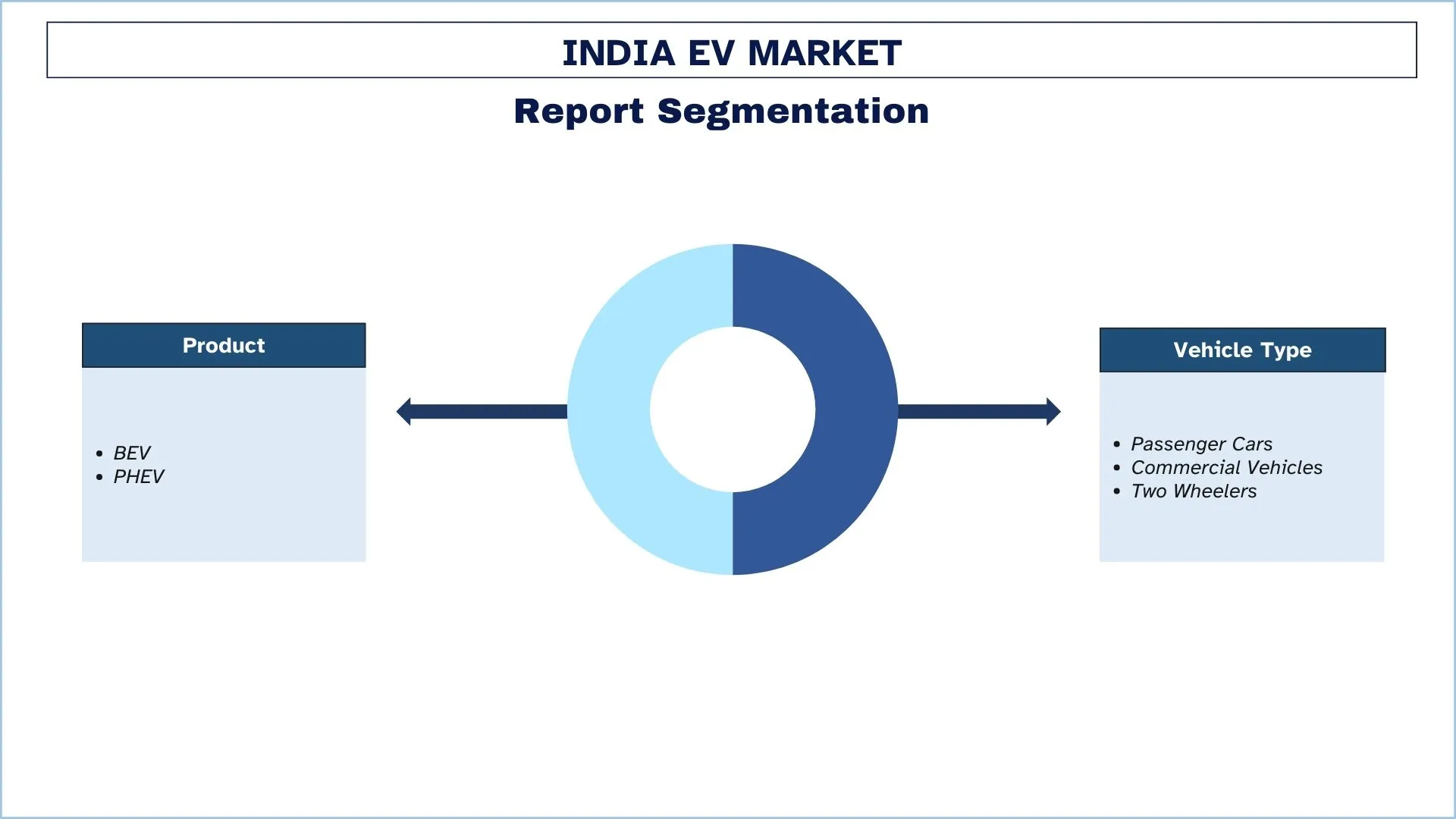

Emphasis on Product (BEV and PHEV); Vehicle Type (Passenger Cars, Commercial Vehicles, and Two Wheelers); and Region/Country

India EV Market Size & Forecast

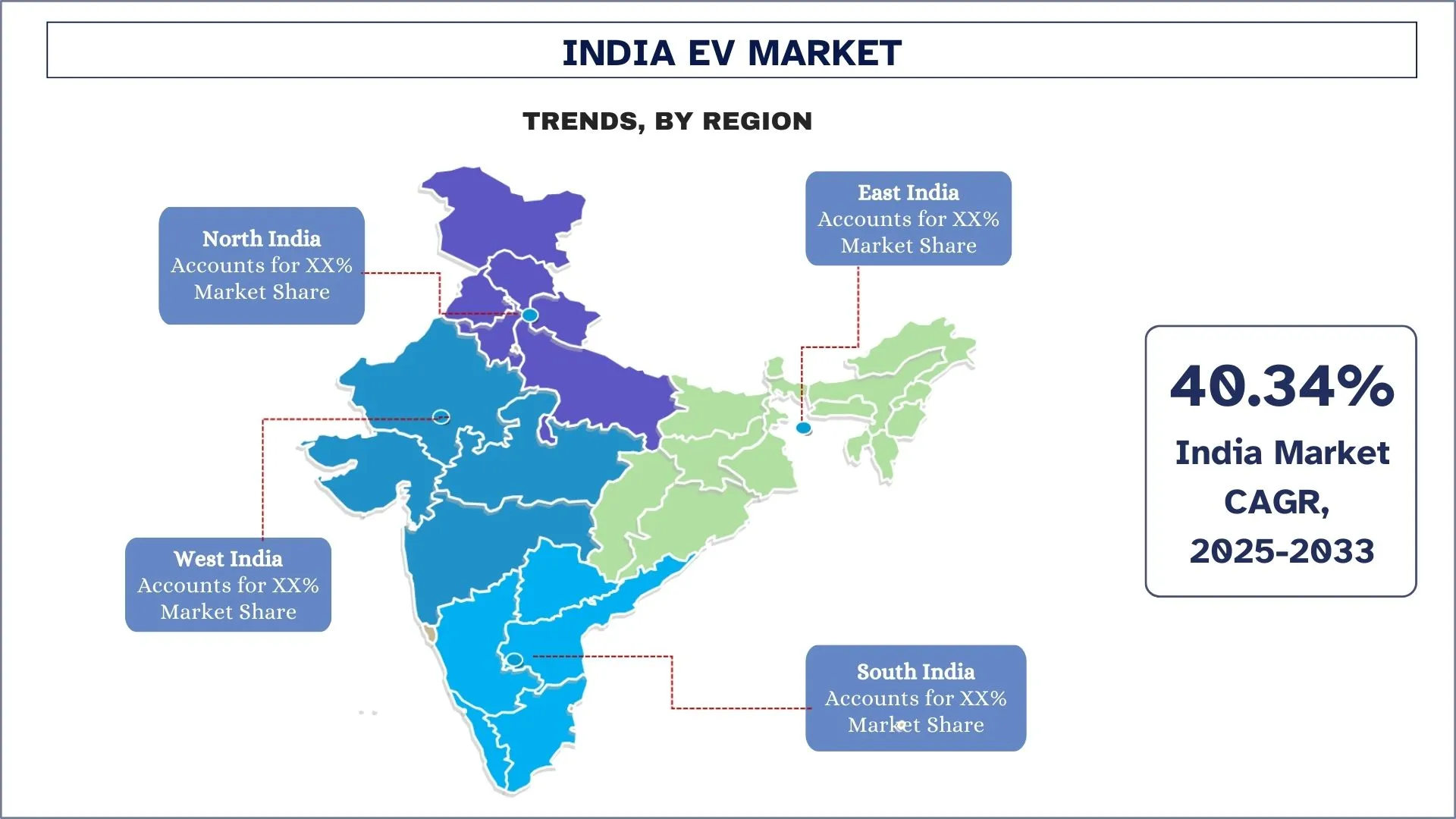

The Indian EV Market was valued at USD 4.8 billion in 2024 and is expected to grow at a strong CAGR of around 40.34% during the forecast period (2025-2033), owing to the rising urbanization, affordability, increasing disposable income, and the shift towards electric mobility.

India EV Market Analysis

India’s EV industry is gaining momentum, aided by government initiatives and rising oil prices. However, the massive shift from internal combustion engine vehicles (ICE) to electric vehicles requires the expansion of infrastructure facilities, including charging stations, and vehicles capable of providing longer range (KM range on a single charge). Moreover, several initiatives taken by the government to support the manufacturing and adoption of electric vehicles in the country should help in achieving the target of 100% EV adoption by 2030, according to the India Brand Equity Foundation (IBEF). These initiatives include the Battery Swapping Policy. On April 22, 2022, NITI Aayog published a draft battery replacement policy effective until March 31, 2025. The policy will be implemented for one to two years from the implementation date and will cover all large cities with a population of 4 Mn or more. The second phase will run for two to three years from the policy’s launch date and will cover all Union Territories (UTs) and major cities with a population of 500,000 or more.

India EV Market Trends

This section discusses the key market trends that are influencing the various segments of the India EV market, as identified by our team of research experts.

Rising Focus on Domestic EV Manufacturing and Localized Supply Chains

The Indian EV market develops under a main trend which involves the rising domestic manufacturing sector alongside local supply chain networks. Indian and global EV companies establish assembly facilities and battery production plants, and component manufacturing units through government incentive schemes, including the Production Linked Incentive (PLI) scheme and FAME II, and import duty advantages. Manufacturing and supply chain activities within India lower both EV import dependency and production costs, which results in affordable prices for the mainstream market. India becomes a frontrunner in developing into an electric vehicle manufacturing center by supporting innovation and employment opportunities through this emerging trend.

India EV Industry Segmentation

This section provides an analysis of the key trends in each segment of the India EV market report, along with forecasts at the regional levels for 2025-2033.

The BEV Market Holds the Largest Share of the India EV Market.

Based on the product, the market is classified into BEV and PHEV. The BEV segment catered to a dominating share of the EV market in India in 2024. The segment's dominant market share can be attributed to consumers' growing preference for EVs over internal combustion engine (ICE) cars and regulations on vehicle CO2 emissions. BEVs have the potential to drastically lower vehicle emissions as well as the long-term cost of ownership. Over the projected period, it is also anticipated that improvements in battery technology and falling lithium-ion battery prices will fuel demand for BEVs.

The Commercial Electric Vehicles Market Holds the Largest Share of the India EV Market.

Based on vehicle type, the market is divided into passenger cars, commercial vehicles, and two-wheelers. Commercial vehicles include electric buses, three-wheelers, and electric cars, and this segment held a significant share of the market in 2024. The ongoing deployment of electric light-duty commercial vehicles and electric buses in the nation is responsible for the segment's expansion. As the government pursues aggressive plans to increase the number of electric cars on the road to minimize vehicle pollution in the nation's major cities, electric buses are already gaining popularity. Electric light-duty commercial vehicles and electric buses are already on the market in the nation because of companies like Tata Motors, Mahindra & Mahindra Ltd, and Olectra Greentech Limited.

North India Leads the Market

The growth of the EV market in North India is fueled by government incentives and policies that make EVs more affordable, rising urban pollution that drives the demand for cleaner transport, and increasing fuel prices that highlight the cost-effectiveness of electric vehicles. Additionally, improving infrastructure such as charging networks and battery-swapping stations, combined with rising disposable income, further supports the market’s expansion. These factors collectively contribute to the increasing adoption of EVs in North India, reflecting a shift towards more sustainable and economically efficient transportation solutions.

India EV Industry Overview

The Indian EV market is competitive and fragmented, with the presence of several country market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top India EV Companies

Some of the major players operating in the market include AUDI AG (Volkswagen Group), BMW AG, Hyundai Motor Company, Jaguar Land Rover Automotive PLC (Tata Motors Limited), Mahindra & Mahindra Limited, The Mercedes-Benz Group AG, MG MOTOR UK Limited (SAIC Motor Corporation Limited), Olectra Greentech Limited (MEIL), Tata Motors Limited, and Toyota Motor Corporation.

Recent Developments in the India EV Market

- For instance, in 2024, Electric scooter maker Ather Energy launched a new range of scooters focused on the family market called Rizta.

- For instance, Honda Global has confirmed plans to launch an electric motorcycle equivalent to 110-125 cc commuters in India next year. The announcement was a part of Honda Motor Co.’s new motorcycle electrification strategy, which will see the manufacturer invest $3.4 billion by 2030 in new products and development. The two-wheeler giant also revised its global sales target from 3.5 million to 4 million electric motorcycles by 2030.

India EV Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 40.34% |

Market size 2024 | USD 4.8 Billion |

Regional analysis | North India, South India, East India, and West India |

Major contributing region | North India is expected to dominate the market. |

Companies profiled | AUDI AG (Volkswagen Group), BMW AG, Hyundai Motor Company, Jaguar Land Rover Automotive PLC (Tata Motors Limited), Mahindra & Mahindra Limited, The Mercedes-Benz Group AG, MG MOTOR UK Limited (SAIC Motor Corporation Limited), Olectra Greentech Limited (MEIL), Tata Motors Limited, and Toyota Motor Corporation |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

By Product, By Vehicle Type, By Region |

Reasons to buy the India EV Market Report:

- The study includes market sizing and forecasting analysis validated by authenticated key industry experts.

- The report presents a quick review of overall industry performance at a glance.

- The report covers an in-depth analysis of prominent industry peers with a primary focus on key business financials, product portfolios, expansion strategies, and recent developments.

- Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

- The study comprehensively covers the market across different segments.

- Deep dive regional-level analysis of the industry.

Customization Options:

The Indian EV Market can further be customized as per the requirements of any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the India EV Market Analysis (2025-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the India EV market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the India EV value chain. After validating market figures through these interviews, we used top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed data triangulation techniques to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the India EV market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including product, vehicle type, and regions within the India EV market.

The main objective of the India EV Market Study.

The study identifies current and future trends in the India EV market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

- Market Size Analysis: Assess the current and forecast market size of the India EV market and its segments in terms of value (USD).

- India EV Market Segmentation: The study segments the market by product, vehicle type, and region.

- Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the India EV industry.

- Regional Analysis: Conduct detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the India EV market and the growth strategies adopted by the market leaders to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the current market size and growth potential of the Indian EV market?

The Indian EV market was valued at USD 4.8 million in 2024 and is projected to grow at a CAGR of 40.34% from 2024 to 2032.

Q2: What are the driving factors for the growth of the Indian EV market?

Strong government support through incentives, subsidies (like FAME II), and a regulatory push for cleaner mobility is fueling rapid EV expansion.

Q3: Which segment has the largest share of the India EV market by product?

The BEV Market holds the largest market share in the India EV market by product segment.

Q4: What are the trends in the India EV market?

Increased investment in EV charging infrastructure by private and public players is accelerating adoption and confidence among EV users.

Q5: Which region will dominate the Indian EV market?

North India is expected to dominate the Indian EV market.

Q6: What are the biggest challenges in the India EV market?

Limited battery manufacturing capabilities and raw material dependency on imports hinder cost efficiency and supply chain resilience.

Q7: Who are the key players in the India EV market?

The leading companies driving innovation in India's EV industry include:

• AUDI AG (Volkswagen Group)

• BMW AG

• Hyundai Motor Company

• Jaguar Land Rover Automotive PLC (Tata Motors Limited)

• Mahindra & Mahindra Limited

• The Mercedes-Benz Group AG

• MG MOTOR UK Limited (SAIC Motor Corporation Limited)

• Olectra Greentech Limited (MEIL)

• Tata Motors Limited

• Toyota Motor Corporation

Q8: What are the key investment opportunities in the India EV market for OEMs and technology providers?

Major investment opportunities lie in domestic EV manufacturing, battery production (under PLI schemes), EV charging infrastructure, and software platforms for fleet and energy management. Collaborations with government initiatives and local partnerships can offer strategic market entry advantages.

Q9: How is government policy shaping the future of the electric vehicle ecosystem in India?

Government policies like FAME II, state-specific EV subsidies, and tax incentives are crucial in driving adoption. The focus on localizing battery production, reducing GST on EVs, and setting up EV-only zones in cities is building a supportive ecosystem for long-term growth.

Related Reports

Customers who bought this item also bought

Micro Mobility Data Analytics Market: Current Analysis and Forecast (2026-2034)

Emphasis on Component (Software / Platform, Services); Analytics Type (Descriptive, Predictive, Prescriptive); Application (Fleet Management, Route Optimization, Demand Forecasting, Rider Behavior Analysis); End-User (Micro Mobility Operators, City Governments/Smart Cities, Transit Agencies); Deployment Mode (Cloud-Based, On-Premises); and Region/Country

Middle East & Africa Automotive Composites Market: Current Analysis and Forecast (2025-2033)

Emphasis By Material Type (Carbon Fiber Composites, Glass Fiber Composites, Natural Fiber Composites, Hybrid Composites, and Others), by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles, and Others), By End-User (OEM and Aftermarket), By Country (Saudi Arabia, UAE, Egypt, South Africa, Turkey, Israel, and the Rest of Middle East & Africa)

Southeast Asia Two-wheeler E-Axle Market: Current Analysis and Forecast (2025-2033)

Emphasis on Type (Hub Motor E-Axle, Mid Drive E-Axle, Integrated E-Axle); Application (Electric Scooters, Electric Motorcycles, Cargo & Delivery Bikes, Shared Mobility Fleets); and Country.

Truck Trailer Landing Gear Market: Current Analysis and Forecast (2025-2033)

Emphasis on Operation (Manual Truck Landing Gear and Automatic Truck Landing Gear); Lifting Capacity (Less Than 20,000 LBS, 20,000 LBS to 50,000 LBS, and More than 50,000 LBS); Sales Channel (OEM and Aftermarket); and Region/Country