Agri-Photovoltaik-Markt: Aktuelle Analyse und Prognose (2024-2032)

Schwerpunkt auf Systemdesign (Fest installierte Solarmodule über Feldfrüchten und dynamische Agri-Photovoltaik); Pflanzenart (Blattgemüse, Wurzelgemüse und Früchte); und Region und Land

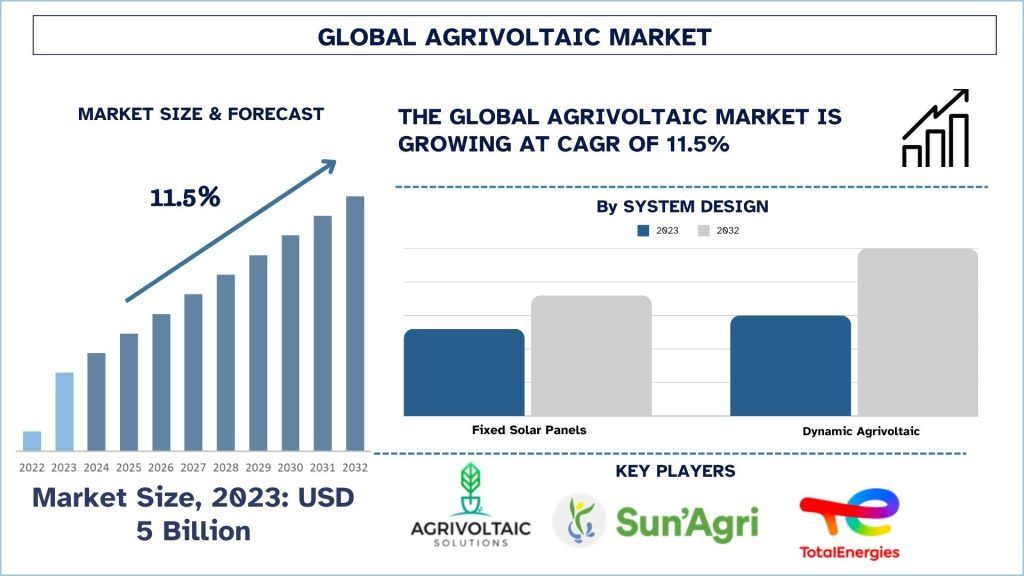

Agrivoltaik Marktgröße & Prognose

Der Agrivoltaik-Markt wurde im Jahr 2023 auf etwa 5 Milliarden USD geschätzt und wird voraussichtlich im Prognosezeitraum (2024-2032) mit einer beträchtlichen jährlichen Wachstumsrate von etwa 11,5 % wachsen, was auf den wachsenden Bedarf an erneuerbaren Energiequellen zurückzuführen ist, der die Einführung von Agrivoltaik-Systemen vorantreibt.

Agrivoltaik Marktanalyse

Agrivoltaik bedeutet, dass sich solare Photovoltaik-(PV)-Systeme auf demselben Grundstück befinden, auf dem landwirtschaftliche Aktivitäten durchgeführt werden. Ein solches System ermöglicht die Integration von zwei Prozessen, einem Solarenergieprozess und einem landwirtschaftlichen Prozess, entweder Pflanzenanbau oder Tierhaltung. Die Solarmodule werden in der Regel in einer bestimmten Höhe oder Position so angebracht, dass die Sonnenstrahlen auf die Feldfrüchte gelangen können, wenn sie auf andere Strukturen treffen, je nachdem, wie das Land genutzt wird, und tragen dazu bei, Schatten zu spenden und die Wasserverdunstung im Prozess zu reduzieren.

Die steigende Nachfrage der Welt nach der Produktion erneuerbarer Energieressourcen erhöht die Nutzung desselben Grundstücks für die Produktion von Energie und Feldfrüchten. Darüber hinaus machen zunehmende Technologie-Features und Fortschritte in der Struktur der Module, einschließlich bifazialer Solarmodule und Neigungsmontagen, Agrivoltaik-Systeme effizienter und rentabler. Im Dezember 2021 arbeitete der US-amerikanische Solarentwickler iSun mit dem deutschen Agrivoltaik-Montageunternehmen Next2Sun zusammen, um gemeinsam ein vertikales Agrivoltaik-System in den Vereinigten Staaten zu entwickeln. iSun installiert das erste US-System von Next2Sun in Vermont. Darüber hinaus führen wachsende Bedenken hinsichtlich des Umweltschutzes und der sozialen Verantwortung von Unternehmen dazu, dass Verbraucher und Investoren eher geneigt sind, Agrivoltaik-Lösungen zu nutzen und in sie zu investieren.

Agrivoltaik Markttrends

Dieser Abschnitt behandelt die wichtigsten Markttrends, die die verschiedenen Segmente des Agrivoltaik-Marktes beeinflussen, wie sie von unseren Forschungsexperten identifiziert wurden.

Segment der festen Solarmodule transformiert die Agrivoltaik-Industrie

Die Verwendung von Solarmodulen, die fest installiert sind, trägt zum Wachstum des Agrivoltaik-Marktes bei, da sie ein nachhaltiges Mittel und eine Methode zur Bereitstellung von Solarenergie in landwirtschaftlichen Betrieben darstellen. Dies ist auf ihre statische Natur und das Fehlen beweglicher Teile zurückzuführen, was ihre Installation recht einfach macht und weniger Wartung für große Agrivoltaik-Anwendungen erfordert. Einige der festen Module können der Sonne zugewandt platziert werden, um den Pflanzen zu helfen, optimales Sonnenlicht zu erhalten, während gleichzeitig einige der Pflanzen vor der vollen Sonne geschützt werden, indem eine teilweise Beschattung ermöglicht wird, um die Pflanzenproduktion zu verbessern. Sie tragen zur Steigerung der Effizienz und Nachhaltigkeit von Agrivoltaik-Projekten in Bezug auf die Betriebskosten bei. Darüber hinaus kann die Einführung fester Module die Akzeptanz durch eine erhöhte Verfügbarkeit einer getesteten und leicht skalierbaren Technologie beschleunigen, die die aktuellen Anbaumethoden ergänzt. Beide tragen gleichermaßen dazu bei, das Wachstum des Marktes zu steigern, indem sie häufigere und vielfältigere Installationen von Agrivoltaik ermöglichen.

Frankreich hatte 2023 einen bedeutenden Marktanteil.

Frankreich hält aufgrund günstiger staatlicher Maßnahmen und Subventionen, die eine nachhaltige Landbewirtschaftung und Energieversorgung unterstützen, den größten Anteil an der Entwicklung des Agrivoltaik-Marktes. Die französische Regierung hat sich zu mehr Ökostrom- und Klimainitiativen verpflichtet, die dazu geführt haben, dass sie Subventionen und Steueranreize für Agrivoltaik-Initiativen gewährt. Frankreich hat eine große Landwirtschaftsindustrie, was bedeutet, dass dieser Sektor viele Möglichkeiten für den Einsatz von Solarmodulen bietet und somit die Produktivität des Landes erhöht. Im September 2024 erhielt der französische Solarprojektentwickler Green Lighthouse Développement die Genehmigung der französischen Regierung für sein 450-MW-Agrivoltaik-Projekt Terr'Arbouts in Landes (Südfrankreich). Das Projekt soll 46 landwirtschaftliche Blöcke mit einer Gesamtfläche von etwa 7 km2 umfassen, wobei die Installation von 2 km2 Modulen geplant ist. Die installierte Leistung des Projekts von 450 MW soll voraussichtlich etwa 650 GWh/Jahr erzeugen, genug, um 140.000 Haushalte mit Strom zu versorgen, sobald es bis 2028 in Betrieb genommen wird. Auch in Frankreich betonen die Beobachtung und Innovation, die in Agrivoltaik-Systemen und -Konfigurationen vorangetrieben werden, die Verbesserung der Beziehung zwischen Photovoltaik-Betrieb und Landwirtschaft. Derzeit entwickeln französische Firmen und Kooperationen einzigartige, innovative Agrivoltaik-Lösungen, was sehr ermutigend ist. Ein unterstützendes regulatorisches Umfeld und der Fokus auf Nachhaltigkeit erklären auch die Investitionen und die Implementierung von Agrivoltaik-Systemen in Frankreich.

Agrivoltaik Branchenüberblick

Der Agrivoltaik-Markt ist wettbewerbsintensiv und es gibt mehrere globale und internationale Akteure. Die wichtigsten Akteure verfolgen unterschiedliche Wachstumsstrategien, um ihre Marktpräsenz zu verbessern, wie z. B. Partnerschaften, Vereinbarungen, Kooperationen, neue Produkteinführungen, geografische Expansionen sowie Fusionen und Übernahmen. Einige der wichtigsten Akteure auf dem Markt sind Agrivoltaic Solutions LLC, Sun’Agri, Enel Spa, BayWa r.e. AG, TotalEnergies, Vattenfall AB, RWE, REM TEC s.r.l., Boralex, Next2Sun Technology GmbH.

Agrivoltaik Marktnachrichten

Im Februar 2023 investierte Vattenfall in ein 76-Megawatt-Agrivoltaik-Projekt. Vattenfall wird dieses innovative Konzept der Landnutzung mit Partnern in kommerziellem Maßstab umsetzen. Das Projekt in Tützpatz zielt darauf ab, auf einer Fläche von 95 ha Modultypen auf verschiedenen Montagesystemen mit geeigneten landwirtschaftlichen Nutzungen zu kombinieren und so weitere praktische Erfahrungen für zukünftige kommerzielle Projekte dieser Art zu sammeln.

Im April 2024 unterzeichneten Lesaffre, ein wichtiger Akteur im Bereich Fermentation und Mikroorganismen seit über 170 Jahren, und Qair, ein unabhängiges Unternehmen für erneuerbare Energien, einen Vertrag über den direkten Bezug von erneuerbarem Strom (CPPA) aus einer Agrivoltaik-Anlage.

Im Mai 2024: Baywa re nahm ein 54-MW-Agrivoltaik-Solarprojekt in Spanien in Betrieb. Das dänische Unternehmen Velux hat sich bereit erklärt, den größten Teil seiner jährlichen Produktion von 96,8 GWh im Rahmen eines langfristigen Stromabnahmevertrags (PPA) zu beziehen.

Agrivoltaik Marktbericht Abdeckung

Berichtsattribut | Details |

Basisjahr | 2023 |

Prognosezeitraum | 2024-2032 |

Wachstumsdynamik | Beschleunigung mit einer CAGR von 11,5 % |

Marktgröße 2023 | 5 Milliarden USD |

Regionale Analyse | China, Japan, Indien, Südkorea, Frankreich, Italien, Deutschland, USA, Rest der Welt |

Wichtigste beisteuernde Region | Es wird erwartet, dass China im prognostizierten Zeitraum mit einer signifikanten CAGR wachsen wird. |

Abgedeckte Schlüsselregionen | China, Japan, Indien, Südkorea, Frankreich, Italien, Deutschland, USA, Rest der Welt |

Profilierte Unternehmen | Agrivoltaic Solutions LLC, Sun’Agri, Enel Spa, BayWa r.e. AG, TotalEnergies, Vattenfall AB, RWE, REM TEC s.r.l., Boralex, Next2Sun Technology GmbH. |

Berichtsumfang | Markttrends, Treiber und Beschränkungen; Umsatzschätzung und Prognose; Segmentierungsanalyse; Angebots- und Nachfrageanalyse; Wettbewerbslandschaft; Unternehmensprofilierung |

Abgedeckte Segmente | Nach Systemdesign, nach Pflanzenart, nach Region/Land |

Gründe für den Kauf dieses Berichts:

- Die Studie umfasst Marktgrößen- und Prognoseanalysen, die von authentifizierten wichtigen Branchenexperten validiert wurden.

- Der Bericht bietet einen schnellen Überblick über die Gesamtleistung der Branche auf einen Blick.

- Der Bericht umfasst eine detaillierte Analyse prominenter Branchenkollegen mit einem primären Fokus auf wichtige Unternehmenskennzahlen, Produktportfolios, Expansionsstrategien und aktuelle Entwicklungen.

- Detaillierte Untersuchung der Treiber, Hemmnisse, wichtigsten Trends und Chancen, die in der Branche vorherrschen.

- Die Studie deckt den Markt umfassend über verschiedene Segmente hinweg ab.

- Tiefgreifende regionale Analyse der Branche.

Anpassungsoptionen:

Der globale Agrivoltaik-Markt kann je nach Anforderung oder einem anderen Marktsegment weiter angepasst werden. Darüber hinaus versteht UMI, dass Sie möglicherweise Ihre eigenen geschäftlichen Anforderungen haben. Zögern Sie daher nicht, sich mit uns in Verbindung zu setzen, um einen Bericht zu erhalten, der Ihren Anforderungen vollständig entspricht.

Inhaltsverzeichnis

Forschungsmethodik für die Agrivoltaik-Marktanalyse (2024-2032)

Die Analyse des historischen Marktes, die Schätzung des aktuellen Marktes und die Prognose des zukünftigen Marktes des globalen Agrivoltaik-Marktes waren die drei Hauptschritte, die unternommen wurden, um die Einführung von Agrivoltaik in wichtigen Regionen weltweit zu erstellen und zu analysieren. Es wurde eine umfassende Sekundärforschung durchgeführt, um die historischen Marktzahlen zu erfassen und die aktuelle Marktgröße zu schätzen. Zweitens wurden zahlreiche Erkenntnisse und Annahmen berücksichtigt, um diese Erkenntnisse zu validieren. Darüber hinaus wurden umfassende Primärinterviews mit Branchenexperten entlang der Wertschöpfungskette des globalen Agrivoltaik-Marktes geführt. Nach der Annahme und Validierung der Marktzahlen durch Primärinterviews haben wir einen Top-Down-/Bottom-Up-Ansatz verwendet, um die vollständige Marktgröße zu prognostizieren. Danach wurden Methoden zur Marktaufschlüsselung und Datentriangulation angewendet, um die Marktgröße von Segmenten und Untersegmenten der Branche zu schätzen und zu analysieren. Die detaillierte Methodik wird im Folgenden erläutert:

Analyse der historischen Marktgröße

Schritt 1: Eingehende Untersuchung von Sekundärquellen:

Es wurde eine detaillierte Sekundärstudie durchgeführt, um die historische Marktgröße des Agrivoltaik-Marktes aus unternehmenseigenen Quellen wie Jahresberichten und Finanzberichten, Performance-Präsentationen, Pressemitteilungen usw. sowie aus externen Quellen wie Fachzeitschriften, Nachrichten und Artikeln, Regierungsveröffentlichungen, Wettbewerbsveröffentlichungen, Branchenberichten, Datenbanken von Drittanbietern und anderen glaubwürdigen Veröffentlichungen zu erhalten.

Schritt 2: Marktsegmentierung:

Nachdem wir die historische Marktgröße des Agrivoltaik-Marktes erhalten hatten, führten wir eine detaillierte Sekundäranalyse durch, um historische Markteinblicke und Anteile für verschiedene Segmente und Untersegmente in wichtigen Regionen zu sammeln. Die wichtigsten Segmente, die in dem Bericht enthalten sind, sind Systemdesign, Art der Kulturpflanze und Regionen. Darüber hinaus wurden länderbezogene Analysen durchgeführt, um die allgemeine Akzeptanz von Testmodellen in der jeweiligen Region zu bewerten.

Schritt 3: Faktorenanalyse:

Nachdem wir die historische Marktgröße der verschiedenen Segmente und Untersegmente ermittelt hatten, führten wir eine detaillierte Faktorenanalyse durch, um die aktuelle Marktgröße des Agrivoltaik-Marktes zu schätzen. Darüber hinaus führten wir eine Faktorenanalyse unter Verwendung von abhängigen und unabhängigen Variablen wie Systemdesign, Art der Kulturpflanze und Regionen des Agrivoltaik-Marktes durch. Es wurde eine gründliche Analyse der Angebots- und Nachfrageszenarien unter Berücksichtigung der wichtigsten Partnerschaften, Fusionen und Übernahmen, Geschäftsexpansionen und Produkteinführungen im Agrivoltaik-Marktsektor weltweit durchgeführt.

Schätzung und Prognose der aktuellen Marktgröße

Aktuelle Marktgrößenbestimmung: Basierend auf den verwertbaren Erkenntnissen aus den oben genannten 3 Schritten haben wir die aktuelle Marktgröße, die wichtigsten Akteure auf dem globalen Agrivoltaik-Markt und die Marktanteile der Segmente ermittelt. Alle erforderlichen prozentualen Anteile und Marktaufschlüsselungen wurden unter Verwendung des oben genannten sekundären Ansatzes ermittelt und durch Primärinterviews verifiziert.

Schätzung & Prognose: Für die Marktschätzung und -prognose wurden verschiedene Faktoren wie Treiber & Trends, Einschränkungen und Chancen, die den Stakeholdern zur Verfügung stehen, gewichtet. Nach der Analyse dieser Faktoren wurden relevante Prognosetechniken, d. h. der Top-Down-/Bottom-Up-Ansatz, angewendet, um die Marktprognose für 2032 für verschiedene Segmente und Untersegmente in den wichtigsten Märkten weltweit zu erstellen. Die zur Schätzung der Marktgröße angewandte Forschungsmethodik umfasst:

Die Marktgröße der Branche in Bezug auf den Umsatz (USD) und die Akzeptanzrate des Agrivoltaik-Marktes in den wichtigsten Märkten im Inland

Alle prozentualen Anteile, Aufteilungen und Aufschlüsselungen von Marktsegmenten und Untersegmenten

Die wichtigsten Akteure auf dem globalen Agrivoltaik-Markt in Bezug auf die angebotenen Produkte. Auch die Wachstumsstrategien, die diese Akteure anwenden, um in dem schnell wachsenden Markt zu konkurrieren

Validierung der Marktgröße und des Marktanteils

Primärforschung: Es wurden ausführliche Interviews mit den wichtigsten Meinungsführern (Key Opinion Leaders, KOLs) geführt, darunter Top Level Executives (CXO/VPs, Vertriebsleiter, Marketingleiter, Betriebsleiter, Regionalleiter, Länderleiter usw.) in den wichtigsten Regionen. Die Ergebnisse der Primärforschung wurden dann zusammengefasst und eine statistische Analyse durchgeführt, um die aufgestellte Hypothese zu beweisen. Die Ergebnisse der Primärforschung wurden mit den Sekundärergebnissen zusammengeführt, wodurch Informationen in verwertbare Erkenntnisse umgewandelt wurden.

Aufteilung der primären Teilnehmer in verschiedenen Regionen

Markt-Engineering

Die Datentriangulationstechnik wurde angewendet, um die gesamte Marktschätzung abzuschließen und präzise statistische Zahlen für jedes Segment und Untersegment des globalen Agrivoltaik-Marktes zu erhalten. Die Daten wurden in mehrere Segmente und Untersegmente aufgeteilt, nachdem verschiedene Parameter und Trends im Systemdesign, in der Art der Kulturpflanze und in den Regionen des globalen Agrivoltaik-Marktes untersucht wurden.

Das Hauptziel der globalen Agrivoltaik-Marktstudie

Die aktuellen und zukünftigen Markttrends des globalen Agrivoltaik-Marktes wurden in der Studie genau bestimmt. Investoren können strategische Einblicke gewinnen, um ihre Entscheidungen für Investitionen auf der Grundlage der in der Studie durchgeführten qualitativen und quantitativen Analyse zu treffen. Aktuelle und zukünftige Markttrends bestimmten die Gesamtattraktivität des Marktes auf regionaler Ebene und boten dem industriellen Teilnehmer eine Plattform, um den unerschlossenen Markt zu nutzen und von einem First-Mover-Vorteil zu profitieren. Weitere quantitative Ziele der Studien sind:

- Analyse der aktuellen und prognostizierten Marktgröße des Agrivoltaik-Marktes in Bezug auf den Wert (USD). Analyse der aktuellen und prognostizierten Marktgröße verschiedener Segmente und Untersegmente.

- Zu den Segmenten der Studie gehören Bereiche des Systemdesigns, der Art der Kulturpflanze und der Regionen.

- Definition und Analyse des regulatorischen Rahmens für die Agrivoltaik

- Analyse der Wertschöpfungskette unter Einbeziehung verschiedener Intermediäre sowie Analyse des Kunden- und Wettbewerbsverhaltens der Branche.

- Analyse der aktuellen und prognostizierten Marktgröße des Agrivoltaik-Marktes für die wichtigste Region.

- Zu den wichtigsten Ländern der in dem Bericht untersuchten Regionen gehören der asiatisch-pazifische Raum, Europa, Nordamerika und der Rest der Welt.

- Unternehmensprofile des Agrivoltaik-Marktes und die von den Marktteilnehmern angewandten Wachstumsstrategien, um den schnell wachsenden Markt zu erhalten.

- Tiefgehende regionale Analyse der Branche

Häufig gestellte Fragen FAQs

F1: Wie groß ist der aktuelle Markt für Agri-Photovoltaik und welches Wachstumspotenzial hat er?

F2: Was sind die treibenden Faktoren für das Wachstum des Agri-Photovoltaik-Marktes?

F3: Welches Segment hat den größten Anteil am Agrivoltaik-Markt nach Systemdesign?

F4: Was sind die wichtigsten Trends im Agrophotovoltaik-Markt?

F5: Welche Region wird den Agrivoltaik-Markt dominieren?

Verwandt Berichte

Kunden, die diesen Artikel gekauft haben, kauften auch

Indien Dekarbonisierungs-HLK-Markt: Aktuelle Analyse und Prognose (2026–2034)

Schwerpunkt Produkttyp (Heizgeräte, Lüftungsgeräte, Klimageräte, Sonstige); Dekarbonisierungstyp (direkt, indirekt); Kapazität (bis zu 5 Tonnen, 5-20 Tonnen, über 20 Tonnen); Endnutzer (Gewerbegebäude, Wohngebäude, Industrieanlagen, Gesundheitseinrichtungen, Rechenzentren, Sonstige); und Region/Bundesstaaten

Midstream-Öl- und Gasfiltrationsmarkt: Aktuelle Analyse und Prognose (2026-2034)

Schwerpunkt auf Filtertechnologie (Koaleszenzfilter, Patronenfilter, Mechanische Filter, Beutelfilter, Partikelfilter, Aktivkohlefilter, Siebe und Sonstige); nach Anwendung (Gasaufbereitungsanlagen, Verdichterstationen, Lagerung und Verteilung, Pipeline-Transport, LNG-Verarbeitung und Sonstige); nach Filtrationsstufe (Ölfiltration und Gasfiltration), nach Endverbraucher (Raffinerien und petrochemische Industrie) und Region/Land

Markt für wasserstoffbetriebene Krankenhaus-Backup-Systeme: Aktuelle Analyse und Prognose (2026-2034)

Schwerpunkt auf Systemtyp (Mobil, Stationär, Hybrid); Leistungskapazität (Unter 100 kW, 100–500 kW und Über 500 kW); Endverbraucher (Öffentliche Krankenhäuser, Private Krankenhäuser, Fachkliniken und Notfallversorgungseinrichtungen); und Region/Land

Wind LiDAR Markt: Aktuelle Analyse und Prognose (2025-2033)

Fokus auf Produkttyp (Vertikal profilierendes Wind-LiDAR, bodengestütztes Wind-LiDAR, gondelmontiertes Wind-LiDAR, luftgestütztes Wind-LiDAR und andere); Komponente (Sensor, Navigator, Laser und andere); Standort (Onshore und Offshore); Anwendung (Windkraft, Meteorologie & Umwelt und Luftfahrt); und Region/Land