Digital Health Market: Current Analysis and Forecast (2025-2033)

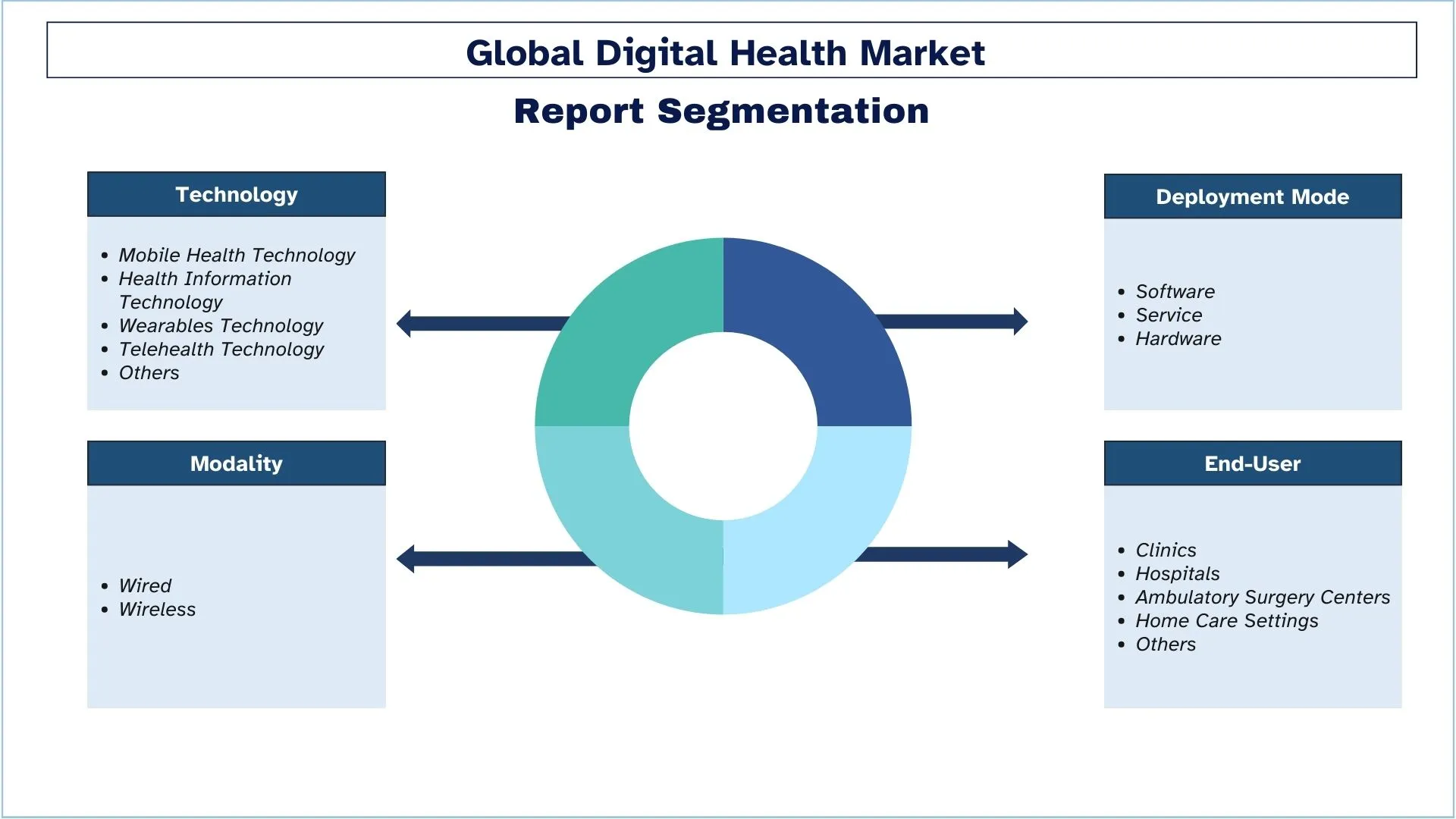

Emphasis on Technology (Mobile Health Technology, Health Information Technology, Wearables Technology, Telehealth Technology, Others), Component (Software, Service, Hardware); Modality (Wired, Wireless); End-Users (Clinics, Hospitals, Ambulatory Surgery Centers, Home Care Settings, Others); and Region & Country.

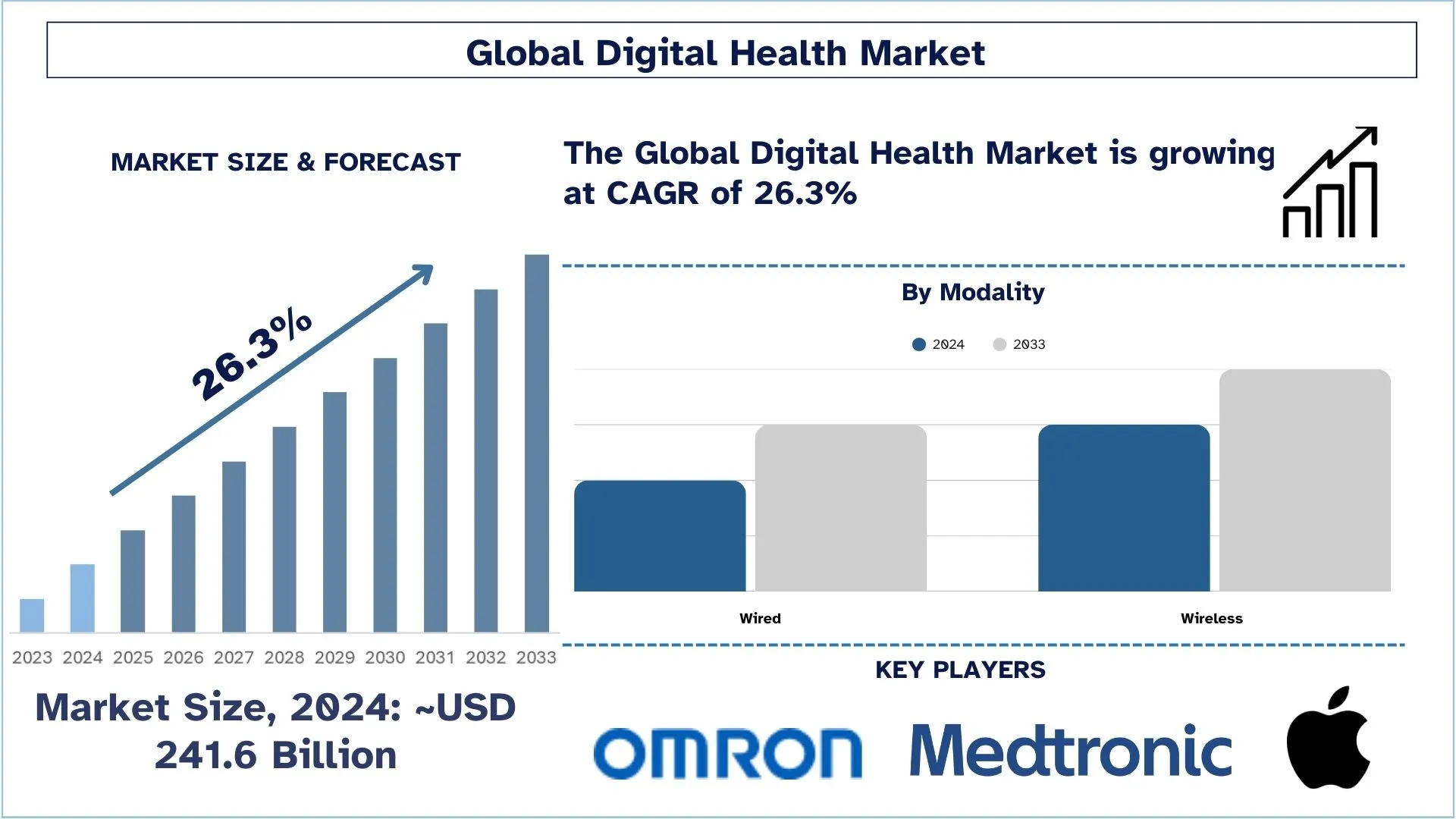

Digital Health Market Size & Forecast

The Digital Health Market was valued at approximately USD 241.6 billion in 2024 and is expected to grow at a substantial CAGR of around 26.3% during the forecast period (2025-2033), owing to the rising demand for remote healthcare services.

Digital Health Market Analysis

Digital health uses technology to help people get better with their health. Wearable devices, mobile health apps, ingestible sensors, electronic health records, and automated care-like devices are mainly used in the case of Digital health. Several government organizations are taking the initiative to promote digital health in their country. For instance, the Australian Government has taken the initiative to promote healthcare IT in Australia through a lifetime policy, PCEHR (Personally Controlled Electronic Health Record) for each of its citizens.

The demand for digital health is increasing on account of the growing number of smartphone users across the globe, rapidly growing healthcare IT infrastructure in developed and developing countries, the growing awareness about the importance of health and fitness among the population, increase in the use of numerous health and medical apps to maintain fitness. Moreover, the growing geriatric population, rising healthcare expenditure levels, and increasing prevalence of diseases, including Chronic Obstructive Pulmonary Disease (COPD), diabetes, and cancer, also propel the market growth. According to the National Institutes of Health (NIH), more than 16 million Americans are suffering from chronic obstructive pulmonary disease (COPD).

Digital Health Market Trends

This section discusses the key market trends influencing the various segments of the digital health market as identified by our research experts.

The rapid integration of AI and machine learning across various healthcare applications

One of the most emerging trends in the development of the digital health industry is the growing application of AI and machine learning in some or most of the healthcare uses. From the diagnosis of the likelihood of disease outbreaks to early identification and offering of treatment plans, AI is shifting healthcare from guesswork to data-driven decisions. Some new-generation companies concentrate on the real-time processing of vast amounts of data and learning from them to detect diseases at an early stage and prescribe treatments. It is beneficial not only for the patients as it enables them to obtain higher quality treatment, but it also helps to overcome the healthcare problems by increasing the speed and simplifying some of the clinical work.

Digital Health Industry Segmentation

This section provides an analysis of the key trends in each segment of the global Digital Health report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Mobile Health Technology Segment Holds the Largest Share of the Market.

Based on technology, the market is fragmented into mobile health technology, health information technology, wearables technology, telehealth technology, and others. The mobile health technology accounted for the largest share in 2024, is anticipated to register a lucrative CAGR during the forecast period. The increase in the use of MHealth apps, increasing penetration of internet connectivity & smartphones, and the high adoption of digital health technologies by patients and physicians mainly drive segment growth. For example, Teva, a pioneer in enhancing health and improving access to quality healthcare for society, has launched a Bluetooth-enabled albuterol sulfate rescue inhaler. The new inhaler is available by prescription to U.S. patients aged 4 and older, according to the Tel Aviv, Israel-based company. ‘ProAir Digihaler’ connects with the smartphone to detect and record COPD and Asthma symptoms.

The Software Segment is Expected to Witness a Higher CAGR than the Digital Health Market.

Based on component, the market is fragmented into software, service, and hardware. The software segment is expected to register the highest CAGR in the upcoming period, owing to the rising demand for reducing medical costs, and several initiatives taken by government organizations to boost healthcare IT also propel the market growth.

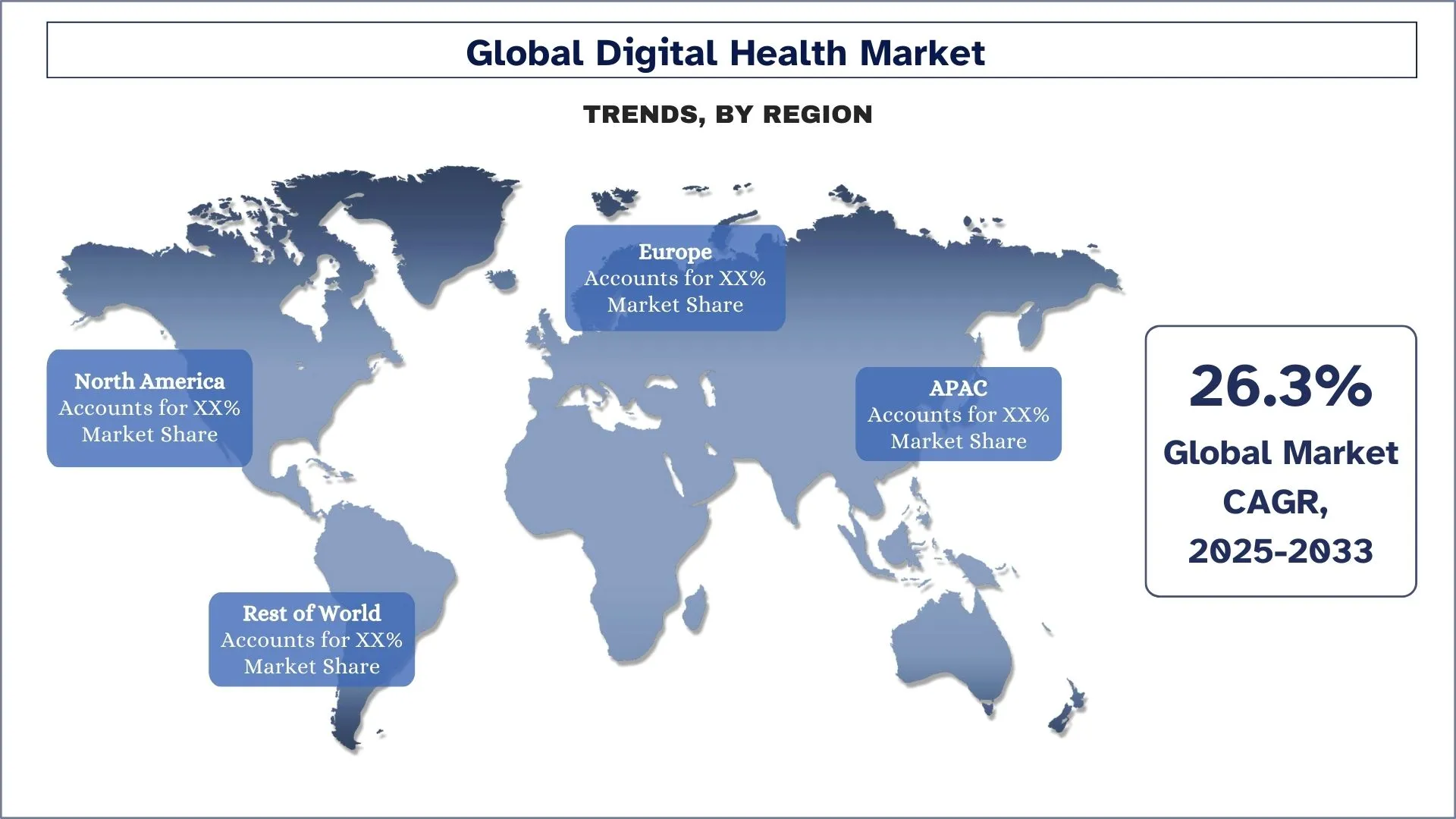

North America has a significant share of the market in 2024.

APAC countries are major Digital Health markets because of the energy demands, government support budgets, and intent to have an enhanced percentage of renewable energy in their total power generation, such as China, India, Japan, South Korea, and Australia. This makes solar power more affordable since APAC is the manufacturing hub of most of the solar parts and gets to enjoy economies of scale and technological improvements. The region is observed to be gradually deploying large-scale solar power plants as well as rooftop systems with the help of favorable policies, decreasing cost of modules, and climate initiatives declaring a shift toward renewable power.

U.S. Dominates the North American Digital Health Market

The digital health industry is in constant growth in the United States due to technological innovation, consumer interest, and government promotion. It includes not only telemedicine, wearable technology, health apps, and AI solutions in the sphere of healthcare. Given the increasing costs of healthcare and the growing need by the patient society for proper, efficient treatment services, technological innovation in the health scene is taking center stage as a way of providing proper care, enhancing patient results, and integrating efficiency in service delivery. It has given rise to public and private investments in the industry to put forward the US as a dominant player in the global digital health market.

Digital Health Industry Competitive Landscape

The Digital Health market is competitive, with several global and international players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top Digital Health Companies

Some of the major players operating in the market are Koninklijke Philips N.V., Medtronic, GE Healthcare, Abbott, OMRON Corporation, Johnson & Johnson Private Limited, Siemens Healthineers AG, Apple, Inc., AT&T, Inc., and Veradigm LLC

Recent Developments in the Digital Health Market

In May 2023, Medtronic (Ireland) acquired EOFlow Co. Ltd. (South Korea) to expand its ability to treat patients with diabetes. In March 2023, GE HealthCare (US) partnered with Advantus Health Partners (US) to sign a multi-year contract to expand access to Healthcare Technology Management Services.

In April 2023, Abbott (US) acquired Cardiovascular Systems, Inc. (CSI) (US) to gain a complementary treatment option for vascular illness. The highly advanced atherectomy technology from CSI prepares vessels for angioplasty or stenting to restore blood flow.

Digital Health Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 26.3% |

Market size 2024 | USD 241.6 Billion |

Regional analysis | APAC, Europe, Asia-Pacific, Rest of the World |

Major contributing region | North America is expected to grow at the highest CAGR during the forecasted period. |

Key countries covered | U.S., Canada, Germany, France, UK, Spain, Italy, China, Japan, and India |

Koninklijke Philips N.V., Medtronic, GE Healthcare, Abbott, OMRON Corporation, Johnson & Johnson Private Limited, Siemens Healthineers AG, Apple, Inc., AT&T, Inc., and Veradigm LLC. | |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Technology, By Component, By Modality, By End-Users, By Region/Country |

Reasons to Buy the Digital Health Market Report:

The study includes market sizing and forecasting analysis validated by authenticated key industry experts.

The report presents a quick review of overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers with a primary focus on key business financials, product portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional-level analysis of the industry.

Customization Options:

The Global Digital Health Market can be customized further as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for Digital Health Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global Digital Health market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the Digital Health value chain. After validating market figures through these interviews, we used top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed data triangulation techniques to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global Digital Health market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including technology, component, modality, End-Users, and regions within the global Digital Health market.

The main objective of the Global Digital Health Market Study

The study identifies current and future trends in the global Digital Health market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

- Market Size Analysis: Assess the current and forecast market size of the global Digital Health market and its segments in terms of value (USD).

- DIGITAL HEALTH Market Segmentation: The study segments the market by technology, component, modality, end-users, and region.

- Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the Digital Health industry.

- Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

- Company Profiles & Growth Strategies: Company profiles of the Digital Health market and the growth strategies adopted by the market leaders to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the Digital Health market's current size and growth potential?

As of 2024, the global digital health market is valued at approximately USD 241.6 billion and is projected to grow at a CAGR of 26.3% through 2033.

Q2: What are the driving factors for the growth of the Digital Health market?

The rising demand for remote healthcare services, driven by aging populations and chronic disease prevalence, is accelerating the adoption of digital health technologies like telemedicine and mobile health apps.

Q3: Which market has the largest share of the Digital Health market by technology?

The Mobile Health Technology dominates the global Digital Health market by technology segment.

Q4: What are the major trends in the Digital Health market?

Increasing integration of AI and machine learning in diagnostics, patient monitoring, and personalized treatment is transforming digital health, enhancing speed, accuracy, and scalability of healthcare delivery.

Q5: Which region will dominate the Digital Health market?

The North America region currently dominates the global Digital Health market.

Q6: What are the biggest challenges in the Digital Health market?

Data privacy and cybersecurity concerns remain a major challenge, as digital health platforms collect and store vast amounts of sensitive patient information that must comply with strict regulatory frameworks.

Q7: Who are the Top players in the global Digital Health market?

The leading companies driving innovation in Digital Health include:

• Koninklijke Philips N.V.

• Medtronic

• GE Healthcare

• Abbott

• OMRON Corporation

• Johnson & Johnson Private Limited

• Siemens Healthineers AG

• Apple, Inc.

• AT&T, Inc.

• Veradigm LLC

Q8: What are the key regulatory challenges for digital health companies operating in the U.S.?

Digital health companies in the U.S. must navigate complex regulatory frameworks, including the FDA’s oversight of medical devices, HIPAA compliance for patient data security, and the FDA’s 21st Century Cures Act that influences telemedicine and digital therapeutics. These regulations are critical to ensuring safety and efficacy while expanding digital health innovations.

Q9: How are telemedicine and remote patient monitoring transforming healthcare delivery in the U.S.?

Telemedicine and remote patient monitoring are significantly improving healthcare access, particularly in rural areas. By enabling virtual consultations and continuous health tracking, these technologies enhance convenience for patients and reduce the burden on healthcare facilities, ultimately leading to better patient outcomes and cost savings.

Related Reports

Customers who bought this item also bought

Intramedullary Nail Leg Lengthening Market: Current Analysis and Forecast (2025-2033)

Emphasis on Technology (Magnetically Controlled Intramedullary Lengthening Nails, Motorized Intramedullary Lengthening Nails, Mechanical Intramedullary Lengthening Nails); Indication (Medical/Reconstructive Indication, Cosmetic/Stature Lengthening); Bone Type (Femoral Lengthening Nails, Tibial Lengthening Nails); End-use (Hospitals, Specialty Orthopedic Clinics, Other); and Region/Country

April 29, 2026

Emphasis on Technology (MRI/CT, Optic Nerve Sheath Diameter (ONSD) Ultrasound, Transcranial Doppler (TCD), Near-Infrared Spectroscopy (NIRS), and Others); Applications (Traumatic Brain Injury, Meningitis, Stroke, Intracerebral Hemorrhage, and Others); End-User (Hospitals & ICUs, Neurology Clinics, Ambulance & Emergency Services, Home Care Settings, and Others); and Region/Country

April 17, 2026

Southeast Asia Blood Glucose Monitoring Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Self-Monitoring Blood Glucose (SMBG) Systems, {Glucometers, Testing Strips, Lancets & Lancing Devices}, Continuous Glucose Monitoring (CGM) Systems, {Sensors, Transmitters, Receivers}); Application (Diabetes Management, Health & Wellness Monitoring, Others); End-User (Hospitals & Clinics, Home-Care Settings, Diagnostic Centers, Others); and Country.

April 6, 2026

Middle East & Africa Laparoscopic Devices Market: Current Analysis and Forecast (2025-2033)

Emphasis By Product (Energy Systems, Robot-Assisted Systems, Laparoscopes, Insufflation Devices, Suction Devices and Access Devices), by Application (General Surgery, Colorectal Surgery, Bariatric Surgery, Gynaecological Surgery, Others), By End-User (Hospitals & Clinics and Ambulatory Surgical ), By Country (Saudi Arabia, UAE, Egypt, South Africa, Turkey, Israel, and the Rest of Middle East & Africa)

April 2, 2026