KSA Hospital Market: Current Analysis and Forecast (2025-2033)

Emphasis on Hospital Ownership (Public Hospitals (Ministry of Health), Private Hospitals, Quasi-Government Hospitals); Bed Capacity (Up to 100 Beds, 100–500 Beds, More than 500 Beds); Hospital Type (General Hospitals, Specialty Hospitals, Multi-Specialty Hospitals); Service Type (In-Patient Services, Out-Patient Services)

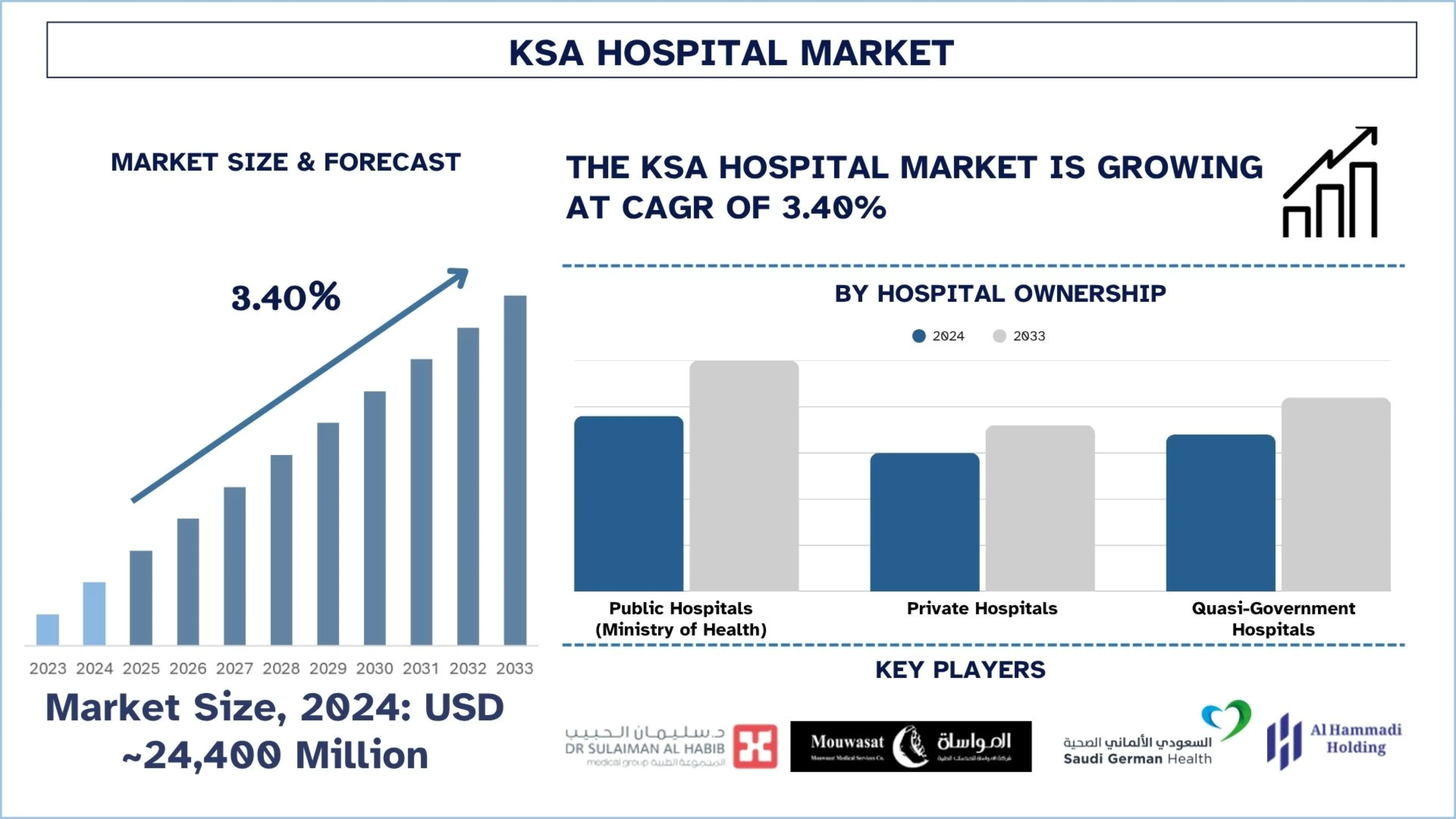

KSA Hospital Market Size & Forecast

The KSA Hospital Market was valued at USD ~24,400 million in 2024 and is expected to grow to a strong CAGR of around 3.40% during the forecast period (2025-2033F), owing to the increasing demand for hospital services in expanding cities like Riyadh and Jeddah.

KSA Hospital Market Analysis

A hospital is defined as a healthcare institution providing medical and nursing services by qualified staff that is licensed to provide medical or surgical treatment to sick or injured people. This typically is a vital point for diagnosis, treatment, emergency care, and rehabilitation, and is staffed with medical personnel and often supported by diagnostic laboratories and imaging centers and operating theatres, and intensive care units. Rising demand from a growing population, expanded private sector involvement, and increased prevalence of chronic disease are driving growth factors, as is government funding as per Vision 2030.

Hospitals in Saudi Arabia are increasingly going digital when it comes to transformations, using AI-driven diagnostics, electronic medical records (EMR), telemedicine, and automated pharmacy systems. In addition, smart infrastructure, specialist departments, and partnerships are being used by leading providers of healthcare as part of the Vision 2030 framework. In addition, decentralization of care and service delivery is being done through Public-Private Partnerships (PPPs) and regional health cluster models by the government.

On May 14, 2025, King Faisal Specialist Hospital & Research Centre (KFSHRC) signed five key international agreements during the Saudi-US Investment Forum 2025, underscoring its commitment to advancing medical innovation and strengthening strategic global collaborations. The agreements were formalized during a high-level roundtable session titled "Next-Generation Healthcare: Saudi-US Collaboration in Biotechnology and Digital Health", held at the King Abdulaziz International Conference Center in Riyadh.

KSA Hospital Market Trends

This section discusses the key market trends that are influencing the various segments of the KSA Hospital market, as found by our team of research experts.

Integration of Smart Hospital Technologies

Saudi Arabia transforms its healthcare system through the adoption of smart hospital technologies. Moreover, IoT devices and artificial intelligence–powered diagnostic tools are being integrated by hospitals to improve operational efficiency and patient care with real-time patient monitoring systems and robotic surgery. These technologies drive data-based decision making, decrease human error, and flow through workflows. This digital evolution is backed by the government’s Vision 2030, which has invested in health IT infrastructure. Moreover, smart technologies contribute to more efficient resource management and more customized treatment that allow hospitals to respond to a growing demand and standards that are increasingly raised abroad.

For example, on May 13, 2025, Dr. Sulaiman Al-Habib Medical Group launched the first-of-its-kind robotic system, AuxQ, powered by Abbott’s AlinIQ AMS technology, in collaboration with FLOW Medical Solutions. This milestone marks an unprecedented achievement and ushers in a new era in intelligent diagnostics and medical automation.

Hospital Industry Segmentation

This section provides an analysis of the key trends in each segment of the KSA Hospital Market report, along with forecasts at the regional and state levels for 2025-2033.

The public hospitals (Ministry of Health) market held the dominant share of the hospital market in 2024.

Based on the hospital ownership, the market is segmented into public hospitals (Ministry of Health), private hospitals, and quasi-government hospitals. Among these, the public hospitals (Ministry of Health) market held the dominant share of the market in 2024. The reason for this is because of extensive government funding, widespread geographic coverage, and the importance of delivering free or subsidized healthcare to citizens. The majority of the bed capacity and health infrastructure in the Kingdom is contained in these hospitals. The Ministry of Health modernizes public facilities, improves the quality of service, as well as Digital e.g, Seha Virtual Hospital, while being backed by Vision 2030. The public hospitals are also referral centers for complex and critical care cases. It still serves as a pillar of high-quality national healthcare access and especially in rural, underserved regions.

The More than 500 Beds market is expected to grow with a significant CAGR during the forecast period (2025-2033) of the KSA Hospital Market.

Based on the bed capacity, the market is segmented into up to 100 beds, 100–500 beds, and more than 500 beds. Among these, the more than 500 beds segment is expected to grow with a significant CAGR during the forecast period (2025-2033). With more than 500 beds, hospitals are key players in driving growth by delivering full, high-capacity care across multiple specialties. It can handle complex cases, decrease patient wait times, and incorporate the latest technologies such as robotic surgery and smart ICUs. These facilities are high-return opportunities for investors and companies as they lead to an increase in patient throughput & government support under Vision 2030.

Hospital Industry Competitive Landscape

The KSA Hospital Market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top KSA Hospitals

Some of the major players in the market are Dr. Sulaiman Al-Habib Medical Group, Mouwasat Medical Services, Middle East Healthcare Company (Saudi German Health), Care Medical Company, Al Hammadi Holding Company, Fakeeh Care Group, King Faisal Specialist Hospital & Research Centre (KFSHRC), International Medical Center, ALMOOSA HOSPITAL, and King Saud Medical City (KSMC).

Recent Developments in the KSA Hospital Market

On May 27, 2025, ImmunityBio, Inc. announced the signing of a strategic Memorandum of Understanding (MOU) with the Ministry of Investment of Saudi Arabia (MISA), King Faisal Specialist Hospital & Research Centre (KFSHRC), and King Abdullah International Medical Research Center (KAIMRC). This multi-party collaboration will introduce the FDA-approved Cancer BioShield platform to Saudi Arabia and the broader Middle East, paving the way for a new era of immune-restorative therapies for cancer patients.

On April 22, 2025, Saudi Arabia’s Ministry of Health announced the launch of a public electronic consultation to identify key health topics for which medical consultations should be delivered via virtual services.

On March 26, 2025, King Faisal Specialist Hospital and Research Centre launched the first dedicated palliative care program for adolescents and young adults in the Arab world. This initiative aims to improve the quality of life of young patients with life-threatening illnesses by offering integrated care throughout their treatment journey.

KSA Hospital Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 3.40% |

Market size 2024 | USD ~24,400 million |

Companies profiled | Dr. Sulaiman Al-Habib Medical Group, Mouwasat Medical Services, Middle East Healthcare Company (Saudi German Health), Care Medical Company, Al Hammadi Holding Company, Fakeeh Care Group, King Faisal Specialist Hospital & Research Centre’s (KFSHRC), International Medical Center, ALMOOSA HOSPITAL, King Saud Medical City (KSMC) |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Hospital Ownership, By Bed Capacity, By Hospital Type, By Service Type, By Region |

Reasons to Buy the KSA Hospital Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, Hospital Ownership portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional-level analysis of the industry.

Customization Options:

The KSA Hospital Market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the KSA Hospital Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the KSA Hospital market to assess its application in major regions in KSA. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the Hospital value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the KSA Hospital market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including hospital ownership, bed capacity, hospital type, and service type, within the KSA Hospital market.

The Main Objective of the KSA Hospital Market Study

The study identifies current and future trends in the KSA Hospital market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

- Market Size Analysis: Assess the current market size and forecast the market size of the KSA Hospital market and its segments in terms of value (USD).

- Hospital Market Segmentation: Segments in the study include areas of hospital ownership, bed capacity, hospital type, and service type.

- Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the Hospital industry.

- Company Profiles & Growth Strategies: Company profiles of the Hospital market and the growth strategies adopted by the market players to sustain in the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the KSA Hospital market’s current market size and growth potential?

The KSA Hospital Market was valued at USD ~24,400 million in 2024 and is expected to grow at a CAGR of 3.40% during the forecast period (2025-2033). This growth is fueled by the growing prevalence of diabetes, cardiovascular diseases, and obesity, driving long-term care needs.

Q2: Which segment has the largest share of the KSA Hospital market by Hospital Ownership?

Public Hospitals (Ministry of Health) dominate the Saudi Arabia Hospital market, benefiting from widespread government support, free/subsidized services, and extensive geographic coverage, particularly in rural and underserved areas.

Q3: What are the driving factors for the growth of the KSA Hospital market?

Key drivers include increasing population and healthcare demand, government-backed infrastructure development, a rise in private healthcare investment, and digital health transformation supported by Vision 2030 reforms.

Q4: What are the emerging technologies and trends in the KSA Hospital market?

Leading trends include the adoption of telemedicine, artificial intelligence in diagnostics, smart hospital infrastructure, and electronic health records (EHRs). Virtual healthcare systems like Seha Virtual Hospital are also expanding access to specialized care.

Q5: What are the key challenges in the KSA Hospital market?

Challenges include healthcare workforce shortages, regulatory barriers for private investment, regional disparities in service access, and the high cost of digital infrastructure implementation in remote areas.

Q6: Who are the key players in the KSA Hospital market?

Some of the leading companies in the KSA Hospital Industry include:

• Dr. Sulaiman Al-Habib Medical Group

• Mouwasat Medical Services

• Middle East Healthcare Company (Saudi German Health)

• Care Medical Company

• Al Hammadi Holding Company

• Fakeeh Care Group

• King Faisal Specialist Hospital & Research Centre’s (KFSHRC)

• International Medical Center

• ALMOOSA HOSPITAL

• King Saud Medical City (KSMC)

Q7: How is Vision 2030 influencing the hospital market in Saudi Arabia?

Vision 2030 is transforming the Saudi hospital landscape by encouraging public-private partnerships (PPPs), promoting digital health adoption, and implementing regional health clusters, leading to improved service delivery and increased investor interest.

Q8: What are the investment opportunities in the Saudi Arabia Hospital sector for foreign and private players?

The Saudi hospital market offers vast opportunities in specialty hospital development, telehealth solutions, AI integration, and medical tourism infrastructure. With favorable regulations and Vision 2030 reforms, international investors are increasingly entering the market.

Related Reports

Customers who bought this item also bought

Intramedullary Nail Leg Lengthening Market: Current Analysis and Forecast (2025-2033)

Emphasis on Technology (Magnetically Controlled Intramedullary Lengthening Nails, Motorized Intramedullary Lengthening Nails, Mechanical Intramedullary Lengthening Nails); Indication (Medical/Reconstructive Indication, Cosmetic/Stature Lengthening); Bone Type (Femoral Lengthening Nails, Tibial Lengthening Nails); End-use (Hospitals, Specialty Orthopedic Clinics, Other); and Region/Country

April 29, 2026

Emphasis on Technology (MRI/CT, Optic Nerve Sheath Diameter (ONSD) Ultrasound, Transcranial Doppler (TCD), Near-Infrared Spectroscopy (NIRS), and Others); Applications (Traumatic Brain Injury, Meningitis, Stroke, Intracerebral Hemorrhage, and Others); End-User (Hospitals & ICUs, Neurology Clinics, Ambulance & Emergency Services, Home Care Settings, and Others); and Region/Country

April 17, 2026

Southeast Asia Blood Glucose Monitoring Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Self-Monitoring Blood Glucose (SMBG) Systems, {Glucometers, Testing Strips, Lancets & Lancing Devices}, Continuous Glucose Monitoring (CGM) Systems, {Sensors, Transmitters, Receivers}); Application (Diabetes Management, Health & Wellness Monitoring, Others); End-User (Hospitals & Clinics, Home-Care Settings, Diagnostic Centers, Others); and Country.

April 6, 2026

Middle East & Africa Laparoscopic Devices Market: Current Analysis and Forecast (2025-2033)

Emphasis By Product (Energy Systems, Robot-Assisted Systems, Laparoscopes, Insufflation Devices, Suction Devices and Access Devices), by Application (General Surgery, Colorectal Surgery, Bariatric Surgery, Gynaecological Surgery, Others), By End-User (Hospitals & Clinics and Ambulatory Surgical ), By Country (Saudi Arabia, UAE, Egypt, South Africa, Turkey, Israel, and the Rest of Middle East & Africa)

April 2, 2026