- Home

- About Us

- Industry

- Services

- Reading

- Contact Us

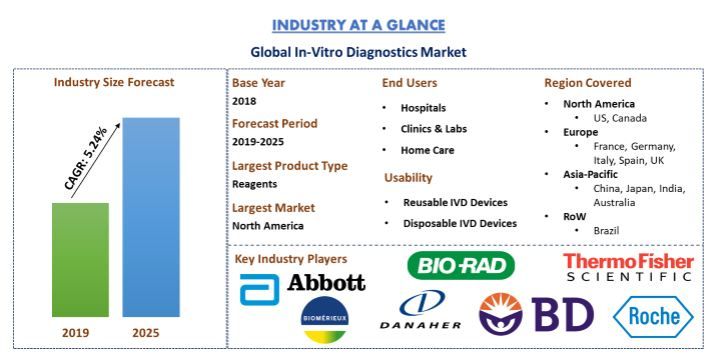

In-Vitro Diagnostics Market: Current Analysis and Forecast 2019-2025

Emphasis on Product (Reagents, Instruments Services), Techniques (Immunoassay, Clinical Chemistry, SMBG, Molecular Diagnostics, Hematology, Microbiology, Point-of-Care, Hemostasis), Application (Infectious Disease, Diabetes, Oncology, Cardiology, Nephrology, Autoimmune Disease, Others), End-Users (Hospitals, Clinics & Labs, Home Care, Others), Usability (Disposable IVD Devices, Reusable IVD Devices) and Region/Country

Global In-Vitro Diagnostics Market was valued at US$ 68.92 billion in 2018 and is anticipated to reach US$ 98.18 billion by 2025 displaying a reasonable CAGR of 5.24% over the forecast period (2019-2025). Global In-Vitro Diagnostics (IVDs) are medical devices and accessories used to perform tests on samples, (e.g., blood, urine and tissue that has been taken from the human body) in order to detect infection, diagnose a medical condition, prevent disease and monitor drug therapies. The market of In-Vitro Diagnostics market is anticipated to grow enormously owing to factors such as rising geriatric population, increasing prevalence of chronic diseases, increasing adoption of Point-of-care diagnosis, and technology advancement in the In-Vitro Diagnostics technology. Rising demand for Point-of-Care (POC) devices is expected to fuel the market growth in near future. In addition, introduction of advanced technologies, such as biochips and nano-biotechnology, and miniaturization of microfluidics are expected to increase the demand for PoC products. These advancements have enabled easy access to PoC diagnostic tests and are likely to facilitate quick and effective test results, thereby boosting the overall market growth. The changing reimbursement models and regulations, investing in unifying technology would mark as a trend in this industry. However, stringent government regulations for the manufacturing of IVD products will act as the major challenges in the growth of this market.

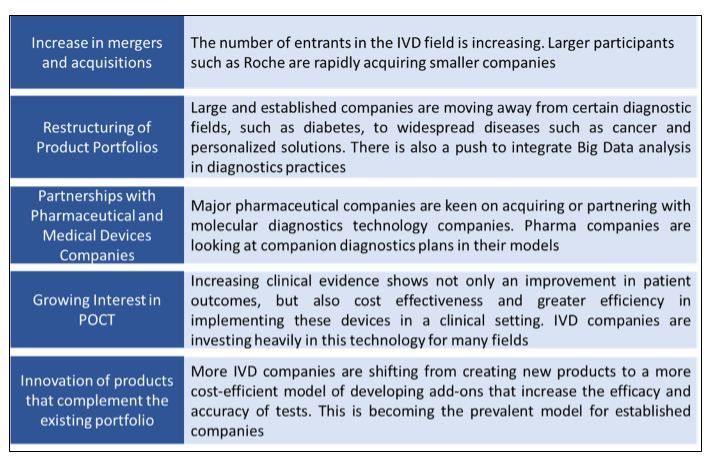

Factors Influencing IVD Companies’ Business Models

“Reagents dominated the product segment of the global In-Vitro Diagnostics market with 69.0% share in 2018”

Based on Product type the global in-vitro diagnostics market is segmented into reagents and Instruments Services. The market of the Reagents segment is expected to grow tremendously and is projected to dominate the market in 2025 due to its high demand in over-the-counter diagnostic tests, paired with rising demand of these for tests at non-medical facilities such as home.

“Immunoassay technique of In-Vitro Diagnostic dominated the market in 2018”

Based on techniques the global In-Vitro Diagnostics market is segmented into Immunoassay, Clinical Chemistry, SMBG, Molecular Diagnostics, Hematology, Microbiology, Point-of-Care and Hemostasis. The Immunoassay technique occupied the largest share of 24.7% in 2018 and is expected to maintain its dominance throughout the forecast period 2019-2025. However, Molecular Diagnostics and Point-of-Care testing techniques are expected to witness highest CAGR growth during the analyzed period, owing to increasing demand for such tests at home.

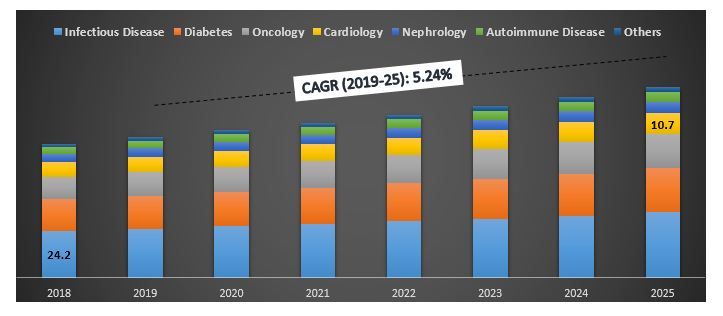

“In-Vitro Diagnostic technology was majorly applied for the treatment or diagnosis of Infectious Disease”

Infectious Diseases, Diabetes, Oncology, Cardiology, Nephrology, Autoimmune Diseases are the major applications of In-Vitro Diagnostics technology. In 2018, IVD was majorly used for the treatment and diagnosis of Infectious Diseases. The segment is expected to witness CAGR 4.89% during the forecast period 2019-2025 to generate revenue of US$ 33.73 billion by 2025. However, Oncology treatment using IVD is expected to grow at the highest rate during the analyzed period.

In-Vitro Diagnostics Market Size, by Application, Global, 2018-25 (US$ Bn)

“Hospitals were the major end-users of In-Vitro Diagnostic technology in 2018”

Based on end-users, the global In-Vitro Diagnostics market is bifurcated into hospitals, clinics & labs, home care and other healthcare facilities. In 2018, hospital segment occupied 47.6% share. However, use of the technology for home disease treatment is expected to witness highest CAGR growth dusting the forecast period 2019-2025. The growing elderly population and associated diseases would help the segment to witness such growth.

“Reusable IVD Devices are expected to dominate the usability segment of the global in-vitro diagnostics market during the analyzed period.”

In-Vitro Diagnostics market segmented based on usability include reusable and disposable IVD devices. The Reusable IVD Devices occupied the largest share and is expected to maintain its dominance throughout the forecast period 2019-2025.

“North America represents one of the largest markets of In-Vitro Diagnostics market globally in 2018”

For a deep-dive analysis of the industry and its adoption rate, detailed regional/country-level analysis was conducted for regions including North America (US, Canada, Rest of North America), Europe (Germany, France, Spain, Italy, UK and Rest of Europe), Asia-Pacific (China, Japan, India, Australia and Rest of Asia-Pacific) and Rest of the World (Brazil and Others). In 2018, North America dominated the market, however growing elderly population in Europe and Asia-Pacific would help the region to use more of in-vitro diagnostic technology for disease detection and treatment.

Competitive Landscape-Top 10 Market Players

Abbott Laboratories, Becton Dickinson and Company, Biomerieux SA, Bio-Rad Laboratories, Inc., Danaher Corporation, Johnson & Johnson, Roche, Siemens Healthineers AG, Sysmex Corporation and Thermo Fisher Scientific are some of the prominent players operating in the Global In-Vitro Diagnostics market industry. Several M&A’s along with partnerships have been undertaken by these players to facilitate costumers with hi-tech and innovative products in the In-Vitro Diagnostic sector.

Reasons to buy (The research report presents):

- Current and future market size from 2018 to 2025 in terms of value (US$)

- Combined analysis of deep-dive secondary research and input from primary research through Key Opinion Leaders of the industry

- Country-level details of the overall adoption of the In-Vitro Diagnostics market

- A quick review of overall industry performance at a glance

- In-depth analysis of key industry players

- A detailed analysis of regulatory framework, drivers, restraints, key trends and opportunities prevailing in the industry

- Examination of industry attractiveness with the help of Porter’s Five Forces analysis and start-ups

- The study comprehensively covers the market across different segments and sub-segments of the technology

- Region/country Covered: North America (US, Canada, Rest of North America), Europe (Germany, France, Spain, Italy, UK and Rest of Europe), Asia-Pacific (China, Japan, India, Australia and Rest of Asia-Pacific) and Rest of the World (Brazil and Others)

Customization Options:

The Global In-Vitro Diagnostics Market can be customized to the country level or any other market segment. Besides this, UMI understands that you may have your own business need, hence we also provide fully customized solutions to clients.

Table of Content

Analyzing historical market, estimation of the current market and forecasting the future market for Global In-Vitro Diagnostics were the three major steps undertaken to create and analyze the overall adoption of in-vitro diagnostic services in major regions/countries. Exhaustive secondary research was conducted to collect the historical market of the technology and overall estimation of the current market. Secondly, to validate these insights, numerous findings and assumptions were taken into consideration. Moreover, exhaustive primary interviews were conducted with industry experts across value chain of the In-Vitro Diagnostics technology. Post assumption and validation of market numbers through primary interviews, top-down approach was employed to forecast the complete market size of In-Vitro Diagnostics market globally. Thereafter, market breakdown and data triangulation methods were adopted to estimate and analyze the overall market size of segments and sub-segments of the technology. Detailed methodology is explained below:

Analysis of Historical Market Size

Step 1: In-Depth Study of Secondary Sources:

Detail secondary study was conducted to obtain the historical market size of the Global In-Vitro Diagnostics Market through company internal sources such as annual report & financial statements, performance presentations, press releases, inventory records, etc. and external sources including trade journals, news & articles, government publications, economic data, competitor publications, sector reports, regulatory bodies publications, safety standard organizations, third-party database and other credible publications. For economic data collection, sources such as World Bank, CDC, European Commission (EC), United Nations and WHO, OECD among others were used.

Step 2: Market Segmentation:

After obtaining the historical market size of the overall market, detailed secondary analysis was conducted to gather historical market insights and share for different segments and sub-segments of the Global In-Vitro Diagnostics technology. Major segments included in the report are product, techniques, applications, end-users and usability.

Step 3: Factor Analysis:

After acquiring the historical market size of different segments detailed factor analysis was conducted to estimate the current market size of the Global In-Vitro Diagnostics technology. Factor analysis was conducted using dependent and independent variables such as accelerating aging population, rising prevalence of age-related disorders and Increasing demand for residential care facilities. Historical trends of the Global In-Vitro Diagnostics technology and their year-on-year impact on the market size and share in the recent past were analyzed. The demand and supply-side scenario were also thoroughly studied.

Current Market Size Estimate & Forecast

Current Market Sizing: Based on actionable insights from the above 3 steps, we arrived at current market size, key players in major applications and markets, market shares of these players and industry’s supply chain. All the required percentage shares split, and market breakdowns were determined using the above-mentioned secondary approach and were verified through primary interviews.

Estimation & Forecasting: For market estimation and forecast, weightage was assigned to different factors including market drivers, restraints, opportunities and trends. After analyzing these factors, relevant forecasting techniques i.e. Bottom-up/Top-down was applied to arrive at the market forecast pertaining to 2025 for different segments and sub-segments of the technology. The research methodology adopted to estimate the market size encompasses:

- The industry’s market size, in terms of value and rate of adoption of In-Vitro Diagnostics globally

- All percentage shares, splits, and breakdowns of market segments and sub-segments

- Key players in major applications and markets as well as the market share of each player. Also, the growth strategies adopted by these players to compete in the ever-growing Global In-Vitro Diagnostics market

Market Size and Share Validation

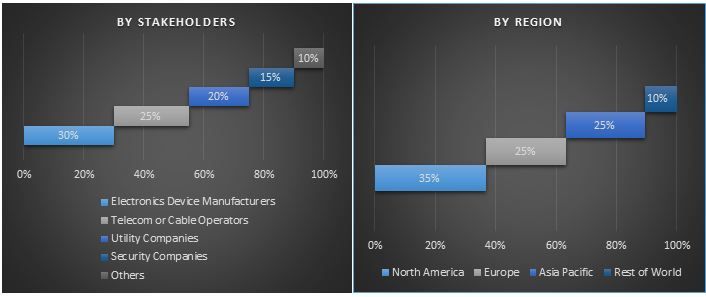

Primary Research: In-depth interviews were conducted with the Key Opinion Leaders (KOLs) including Top Level Executives (CXO/VPs, Sales Head, Marketing Head, Operational Head, and Regional Head, etc.). Primary research findings were summarised, and statistical analysis was performed to prove the stated hypothesis. Input from primary research was consolidated with secondary findings, hence turning information into actionable insights.

Split of Primary Participants

Market Engineering

Data triangulation technique was employed to complete the overall market engineering process and to arrive precise statistical numbers of each segment and sub-segment pertaining to the Global In-Vitro Diagnostics market. Data was split into several segments post studying various parameters and trends in areas such as product, techniques, applications, end-user, usability and regions such as North America, Europe, Asia-Pacific and Rest of the World.

Main objective of the In-Vitro Diagnostics Market Study

The current & future market trends of the Global In-Vitro Diagnostics market are pinpointed in the study. Investors can gain strategic insights to base their discretion for investments from the qualitative and quantitative analysis performed in the study. Current and future market trends would determine the overall attractiveness of the market, providing a platform for the industrial participant to exploit the untapped market to benefit as first-mover advantage. Other quantitative goals of the studies include:

- Analyze the current and forecast market size of the global in-vitro diagnostics market in terms of value (US$)

- Analyze the current and forecast market size of different segments and sub-segments of the global in-vitro diagnostics market

- To analyze the revenue and business models of the market players in the industry

- To understand the initiatives undertaken by diagnostics companies Vs. service providers to increase the overall analysis of in-vitro diagnostics in major regions

- Define and describe the segments and sub-segments considered in the evaluation of the global in-vitro diagnostics market and anticipate potential risk associated with the market

- Define and analysis of the government regulations for diagnostics

- Analyze the current and forecast market size of the global in-vitro diagnostics market for major regions/countries including North America (US, Canada, Rest of North of America), Europe (Germany, France, Spain, Italy, UK, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, Rest of Asia-Pacific) and Rest of World (Brazil, Others)

- Define and analyze the competitive landscape of the global in-vitro diagnostics market and the growth strategies adopted by the market players to sustain in the fast

Related Reports

Customers who bought this item also bought

KSA Hospital Market: Current Analysis and Forecast (2025-2033)

Emphasis on Hospital Ownership (Public Hospitals (Ministry of Health), Private Hospitals, Quasi-Government Hospitals); Bed Capacity (Up to 100 Beds, 100–500 Beds, More than 500 Beds); Hospital Type (General Hospitals, Specialty Hospitals, Multi-Specialty Hospitals); Service Type (In-Patient Services, Out-Patient Services)

June 9, 2025

Epigenetics Diagnostics Market: Current Analysis and Forecast (2025-2033)

Emphasis on Diagnostics Technology (DNA Methylation, Histone Modification, MicroRNA modification, and Others); Application (Oncology, Autoimmune Disorders, Neurological Disorders, Metabolic Disorders, and Others); End-User (Hospitals, Pharmaceutical & Biotechnology firms, Diagnostic Laboratories, and Others); and Region/Country

June 9, 2025

India Ayurvedic Products Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Healthcare Products: Ayurvedic Medicines, Ayurvedic Nutraceuticals and Dietary Supplements; Personal Care Products: Skin Care, Oral Care, Hair Care and Fragrances; Wellness & Lifestyle Products: Ayurvedic Oils and Massage Products, Aromatherapy and Essential Oils, Detox and Digestive Aids; Others); Distribution Channel (Offline Retail, Online Retail/E-commerce, Direct-to-Consumer (D2C) Platforms) and Region/States

June 4, 2025