- Home

- About Us

- Industry

- Services

- Reading

- Contact Us

Military Parachute Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Round Type Parachute, Cruciform Parachute, Ribbon and Ring/Annular Parachute, and Ram Air Parachute); Deployment (Static Line Deployment, Free Fall Deployment, and Rapid Deployment); Application (Military Operations, Training Exercises, and Humanitarian Aid Dropping); and Region/Country

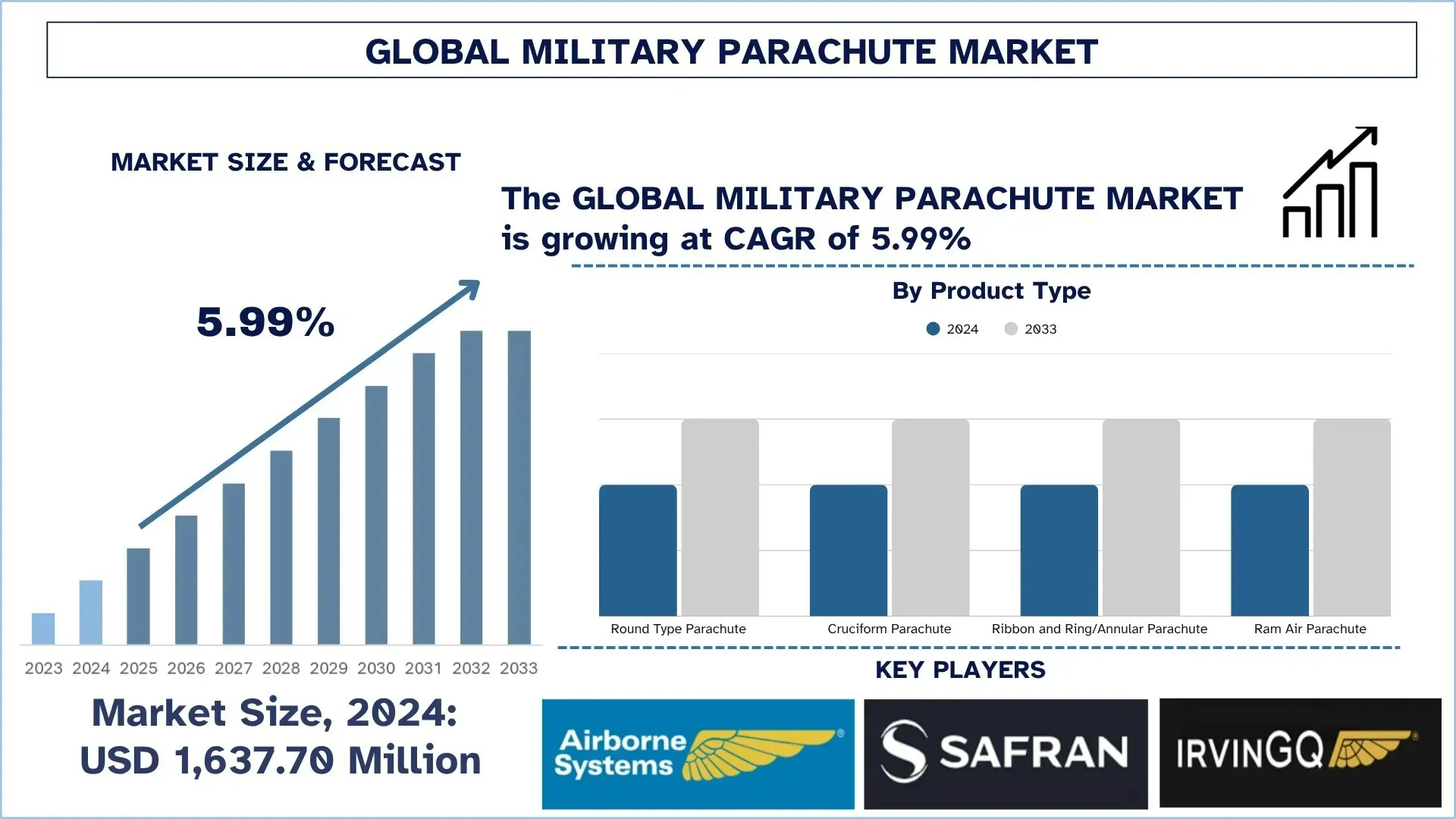

Global Military Parachute Market Size & Forecast

The Global Military Parachute Market was valued at USD 1,637.70 million in 2024 and is expected to grow at a CAGR of around 5.99% during the forecast period (2025-2033F), driven by the increased military spending globally and the growth in special forces and rapid deployment units.

Military Parachute Market Analysis

The military parachute market continues to grow, and this is due to the growing demand for mass troop deployment, tactical resupply, and enhanced aerial mobility in contemporary defense strategy. Military parachutes refer to vital gadgets that aid in the safe transportation of members into the plane overhead and rescue those who are on the ground. Such systems play an important role by facilitating accurate landings in any complex battle/ humanitarian area and making the mission and safety of personnel successful. With the modernization of armed forces on a global scale to have faster mobility and high mobility capabilities in the airborne segment, the need to have sophisticated parachute systems has increased at a higher rate. Moreover, this has been supported by the increased focus on special operations and expeditionary operations that have served to strengthen the value of parachute systems in modern warfare. The main strengths of modern military parachutes are maneuverability, allowing more control over the parachute, increased payload ability, and reliability in deployment for a variety of altitudes and terrains. Innovation in lightweight materials, steerable parameters, and automatic deployment systems further expands to make the systems more efficient, less expensive, and fully capable of adapting to the current dynamic environment in military operations.

Global Military Parachute Market Trends

This section discusses the key market trends that are influencing the various segments of the global military parachute market, as found by our team of research experts.

Adoption of Ram Air and Steerable Parachutes

The combination of ram air and steerable parachutes has proved to be a major trend in the military parachute worldwide market due to the necessity to provide much greater precision, steerability, and the ability to adapt to a variety of operations performed in the military sector. This trend can be seen in the adoption of the MC-6+ Advanced Tactical Parachute System by the U.S. Army. The MC-6+ is a derivative of the MC-6 system and is used to infiltrate heavily loaded jumpers precisely. It has a bigger canopy, greater maximum deployment weight, and slows down at a lower descent rate, and continues the tradition of safety and reliability. Just as in the original MC-6, the MC-6+ did not lose the interesting feature of letting jumpers back out in deep brakes and has more openings at higher elevations (thus preventing destruction as experienced in the MC1-1C in similar deployment circumstances). Also, there is the Joint Precision Airdrop System (JPADS), with GPS-guided Ram Air parachutes, which allows the exact drop of goods and equipment to designated drop zones, even under poor weather. This trend can be explained by the growing demands regarding precision, safety, and efficiency of use of military parachute systems that are strategic in contemporary airborne operations.

Military Parachute Industry Segmentation

This section provides an analysis of the key trends in each segment of the global military parachute market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Round Type Parachute Market Dominates the Military Parachute Market

Based on product type, the military parachute market is segmented into Round Type Parachute, Cruciform Parachute, Ribbon and Ring/Annular Parachute, and Ram Air Parachute. In 2024, the round-type parachute segment dominated the market and is expected to maintain its lead through the forecast period. Round parachutes have gained widespread popularity because of their economy, simplicity, and safety in use, in mass troop deployment and basic airdrop missions. Their durable nature and deployment ease make them perfect for large military logistics as well as training exercises. Although technological improvements have been achieved in steerable parachutes, the fact is that round parachutes are still very much in use due to their low-maintenance specifications, their historical record of safety, and most importantly, the ease with which round parachutes can be applied to a wide variety of different aircraft types. Also, their proficiency during low-altitude drops and their capacity to carry heavier payloads during non-combat areas also add to their superiority. The importance of rapid deployment, higher consumption in the training of the military, and a growing airborne infantry program with most nations worldwide are boosters that continue to see this segment grow.

The Static Line Deployment Category held the Largest Market Share in the Military Parachute Market

Based on deployment, the military parachute market is segmented into Static Line Deployment, Free Fall Deployment, and Rapid Deployment. In 2024, the static line segment held the largest share and is expected to remain at the top for the next few years. Static line parachutes are commonly deployed in the mass introduction of troops since they automatically deploy quickly, and the training required is less in comparison to the use of free-fall parachutes. This qualifies them particularly in large-scale operations involving airborne troops, training, and logistics drops. The easy and stable nature of the deployment system of the static lines makes it favorable for high volume and low jump altitude jumps, a feature necessary for rapid mobilization. Moreover, the required rapid response teams and the increased interest in paratrooper education in most countries enhance the interest in the usage of such a way of deployment. The static line systems provide operational flexibility and reliability, as military doctrines tend to pay more attention to rapid reaction, force projection, and joint operations. Their effectiveness in non-combat and combat operations strengthens their standing as the deployment method of choice in the international military parachute market.

North America Dominated the Global Military Parachute Market

North America holds the largest share in the military parachute market, and it is expected to maintain this dominance throughout the forecast period. This is mainly attributed to well-established military expenditure on defense, superiority in air transportation, and the frequent acquisition of the new generation parachute systems by the U.S. armed forces. The existence of major manufacturers, growing emphasis on modernization of paratrooper equipment, and special operations training are further contributing to the region's expansion. Also, North America is investing in troop mobility, rapid response factors, and integrated defense logistics components that factor into continually demanding needs. The strategic focus being placed on being ready and rapid deployment, as well as ongoing military modernization initiatives, is what keeps the region at the top of the world when it comes to the military parachute industry. In addition, frequent military exercises with NATO partners and rising investments in multi-domain operational preparedness are likely to further increase the need for superior parachute systems in the near future.

U.S. held a dominant Share of the North America Military Parachute Market in 2024

The U.S has the highest share in the world market of military parachutes owing to powerful government support backed by a robust defense industry and continued investment in sophisticated types of military technologies. Military organizations such as the U.S. Department of Defense and NASA commonly purchase and utilize high-technology parachutes to deploy troops, airdrop cargo, and engage in tactical operations. Intense training programs, special operations, and disaster response operations are also boosting the continuous usage of high-performance parachutes. The U.S. has developed a pre-existing system of manufactured equipment, like the Airborne Systems and NSN (National Stock Number) registered suppliers, which are ready to produce quickly and deliver. With every evolution of the lighter, more maneuverable parachute systems and with vast military training, the U.S is always on the edge of parachute technology advancements.

Military Parachute Industry Competitive Landscape

The global military parachute market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top Military Parachute Companies

Some of the major players in the market are Airborne Systems North America, Safran SA, IrvinGQ, Aerodyne Research LLC, Mills Manufacturing, Precision Aerodynamics, FXC Corporation, MarS a.s., Ordnance Parachute Factory, and Tactical Parachute Delivery Systems, Inc.

Recent Developments in the Military Parachute Market

In June 2025, A leader in advanced C4ISR and defense product innovation, BANC3, Inc., was contracted by the US Department of Defense (DoD) to develop SAFEDROP. This augmented/mixed reality (AR/MR) and computer vision (CV) application of the next generation is aimed at providing non-specialist soldiers the ability to effectively rig equipment and cargo to be used as part of an aerial delivery joint operation.

In June 2025, SERT reported being awarded a contract to supply HALO/HAHO parachute systems to the Indonesian KOPASSUS. These systems that will have the CPS Military Silhouette Series will boost the operational free-fall programs. Such a partnership will reflect the focus of SERT on providing high-end solutions to the governments in Southeast Asia for military and law enforcement.

Global Military Parachute Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 5.99% |

Market size 2024 | USD 1,637.70 Million |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | North America is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, and India |

Companies profiled | Airborne Systems North America, Safran SA, IrvinGQ, Aerodyne Research LLC, Mills Manufacturing, Precision Aerodynamics, FXC Corporation, MarS a.s., Ordnance Parachute Factory, and Tactical Parachute Delivery Systems, Inc. |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Product Type; By Deployment; By Application; By Region/Country |

Reasons to Buy Military Parachute Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional-level analysis of the industry.

Customization Options:

The global military parachute market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global Military Parachute Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global military parachute market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the military parachute value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global military parachute market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including product type, deployment, application, and regions within the global military parachute market.

The Main Objective of the Global Military Parachute Market Study

The study identifies current and future trends in the global military parachute market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current market size and forecast the market size of the global military parachute market and its segments in terms of value (USD).

Military Parachute Market Segmentation: Segments in the study include areas of product type, deployment, application, and regions.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the military parachute industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the military parachute market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global military parachute market current market size and its growth potential?

The global military parachute market was valued at USD 1637.70 million in 2024 and is expected to grow at a CAGR of 5.99% during the forecast period (2025-2033).

Q2: Which segment has the largest share of the global military parachute market by product type?

The round-type parachute segment dominated the market and is expected to maintain its leading position throughout the forecast period. Round parachutes have gained widespread popularity because of their economy, simplicity, and safety in use, in mass troop deployment and basic airdrop missions.

Q3: What are the driving factors for the growth of the global military parachute market?

• Increased Military Spending Globally: Rising defense budgets in the U.S., China, India, and NATO countries are fueling procurement of airborne systems, including tactical parachutes for rapid deployment and logistics.

• Growth in Special Forces and Rapid Deployment Units: Expansion of special operations units requires precision, maneuverable parachutes for high-altitude missions, boosting demand for advanced parachute systems.

• Frequent Multinational Military Exercises: Joint training operations and interoperability efforts are encouraging standardization and bulk acquisition of parachute systems by allied nations.

Q4: What are the emerging technologies and trends in the global military parachute market?

• Adoption of Ram Air and Steerable Parachutes: Forces are shifting from traditional round parachutes to Ram Air systems for greater maneuverability and precision landings.

• Use of Advanced Lightweight Materials: Development of high-strength, low-weight fabrics and modular systems is reducing fatigue and improving parachute portability and performance.

Q5: What are the key challenges in the global military parachute market?

• High Cost of Advanced Parachute Systems: Modern parachutes with steerable designs and integrated electronics come at a premium, limiting adoption in lower-income countries.

• Logistical Complexity in Large-Scale Deployments: Coordinating mass airborne deployments requires robust planning, training, and infrastructure, which can strain resources.

Q6: Which region dominates the global military parachute market?

North America holds the largest share in the military parachute market, and it is expected to maintain this dominance throughout the forecast period. This is mainly attributed to well-established military expenditure on defense, superiority in air transportation, and the frequent acquisition of the new generation parachute systems by the U.S. armed forces. The existence of major manufacturers, growing emphasis on modernization of paratrooper equipment, and special operations training are further contributing to the region's expansion.

Q7: Who are the key players in the global military parachute market?

Some of the key companies include:

• Airborne Systems North America

• Safran SA

• IrvinGQ

• Aerodyne Research LLC

• Mills Manufacturing

• Precision Aerodynamics

• FXC Corporation

• MarS a.s.

• Ordnance Parachute Factory

• Tactical Parachute Delivery Systems, Inc.

Q8: What is the projected ROI timeline for investments in next-generation military parachute technologies?

• Procurement Cycle Alignment: ROI typically aligns with 5–7 year defense procurement cycles, depending on contract size and deployment volume.

• Recurring Revenue Streams: Long-term government contracts and periodic restocking ensure stable returns through maintenance and training service packages.

• Margin Expansion via Innovation: Investment in lighter materials and smart deployment tech leads to higher-margin offerings and competitive differentiation.

Q9: How resilient is the military parachute supply chain to geopolitical or macroeconomic disruptions?

• Diversified Manufacturing Footprint: Leading vendors have production units in the U.S., Europe, and Asia to reduce over-reliance on single-region suppliers.

• Material Substitution Readiness: Companies are increasingly adopting alternative fibers and regionalized component sourcing to counter export controls.

• Government Buffer Contracts: Defense agencies often pre-stock critical systems, creating baseline demand stability even during global shocks.

Related Reports

Customers who bought this item also bought

Military Parachute Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Round Type Parachute, Cruciform Parachute, Ribbon and Ring/Annular Parachute, and Ram Air Parachute); Deployment (Static Line Deployment, Free Fall Deployment, and Rapid Deployment); Application (Military Operations, Training Exercises, and Humanitarian Aid Dropping); and Region/Country

August 5, 2025

5th Generation Aircraft Market: Current Analysis and Forecast (2025-2033)

Emphasis On Engine Type (Single-Engine and Double-Engine), By Take-Off (Long Take-Off, Short-Take-Off and Vertical Take-Off And Landing), By Aircraft Type (Fighter Jets, Bomber Aircrafts, and Unmanned Aerial Combat Vehicles) and , By End-User (Army, Air Force, and Navy & Marine), By Combat Capability (Supercruise and Non-Supercruise) Region/Country

July 2, 2025

India Drones Market: Current Analysis and Forecast (2025-2033)

Emphasis on Type (Fixed Wing, Rotary Wing, Hybrid VTOL); Point of Sale (Original Equipment Manufacturers (OEM), Aftermarket); Mode of Operation (Remotely Piloted Aircraft (RPA), Fully Autonomous, Semi-Autonomous); End-Users (Defense & Homeland Security, Agriculture, Infrastructure, Retail and Supply Chain, Energy and Power, Media and Entertainment, Others); and Region/States

June 5, 2025

3D-Printed Drones Market: Current Analysis and Forecast (2025-2033)

Emphasis on Type (Fixed-wing, Multi-rotor, Single-rotor, and Hybrid); Component (Airframe, Wings, Landing Gears, Propellers, Mounts & Holders, and Others); Technology (Fused Deposition Modeling (FDM), Stereolithography (SLA), Selective Laser Sintering (SLS), and Others); Application (Consumer, Military, Commercial, and Government & Law Enforcement) and Region/Country

May 20, 2025