3D-Printed Drones Market: Current Analysis and Forecast (2025-2033)

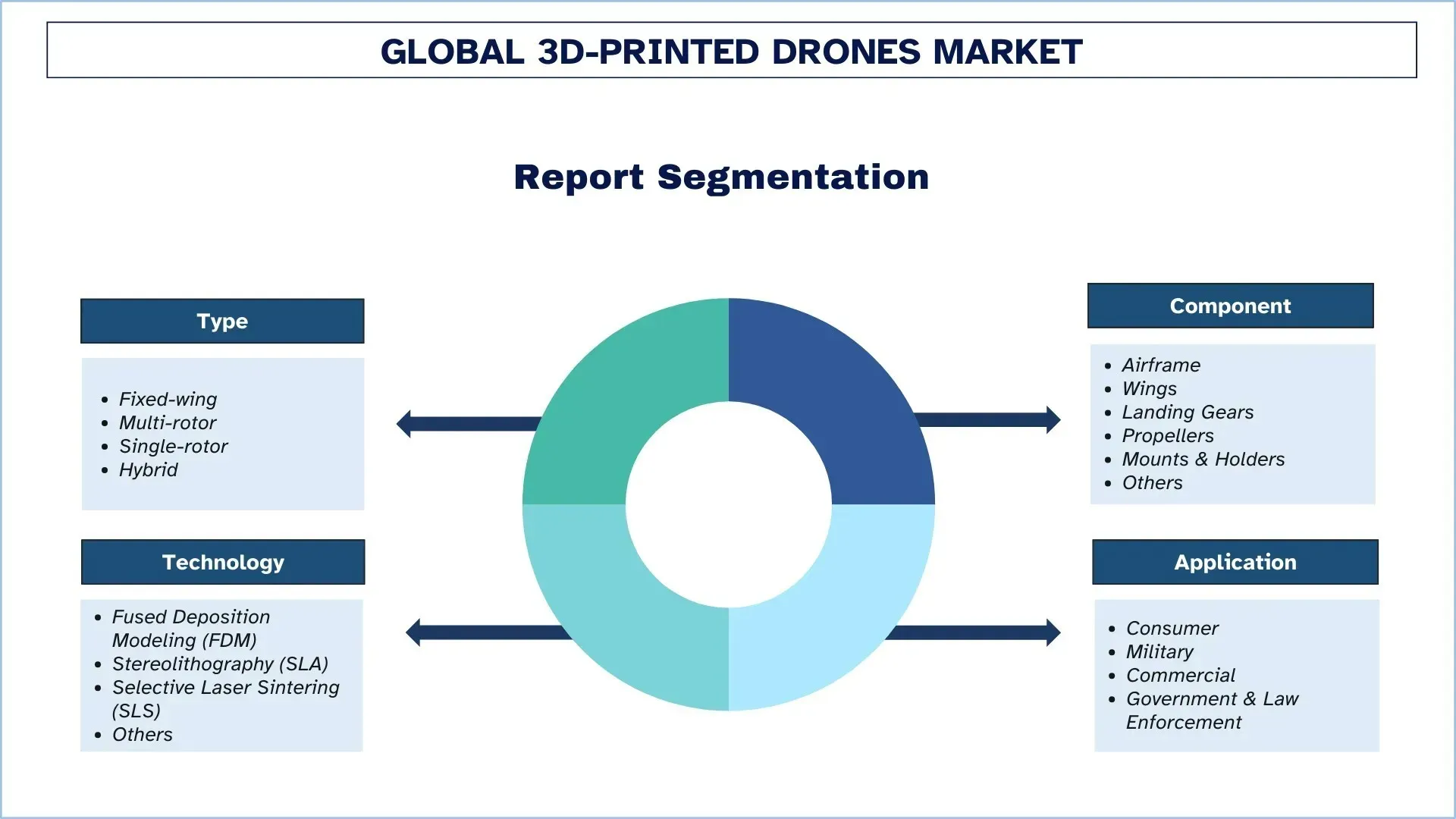

Emphasis on Type (Fixed-wing, Multi-rotor, Single-rotor, and Hybrid); Component (Airframe, Wings, Landing Gears, Propellers, Mounts & Holders, and Others); Technology (Fused Deposition Modeling (FDM), Stereolithography (SLA), Selective Laser Sintering (SLS), and Others); Application (Consumer, Military, Commercial, and Government & Law Enforcement) and Region/Country

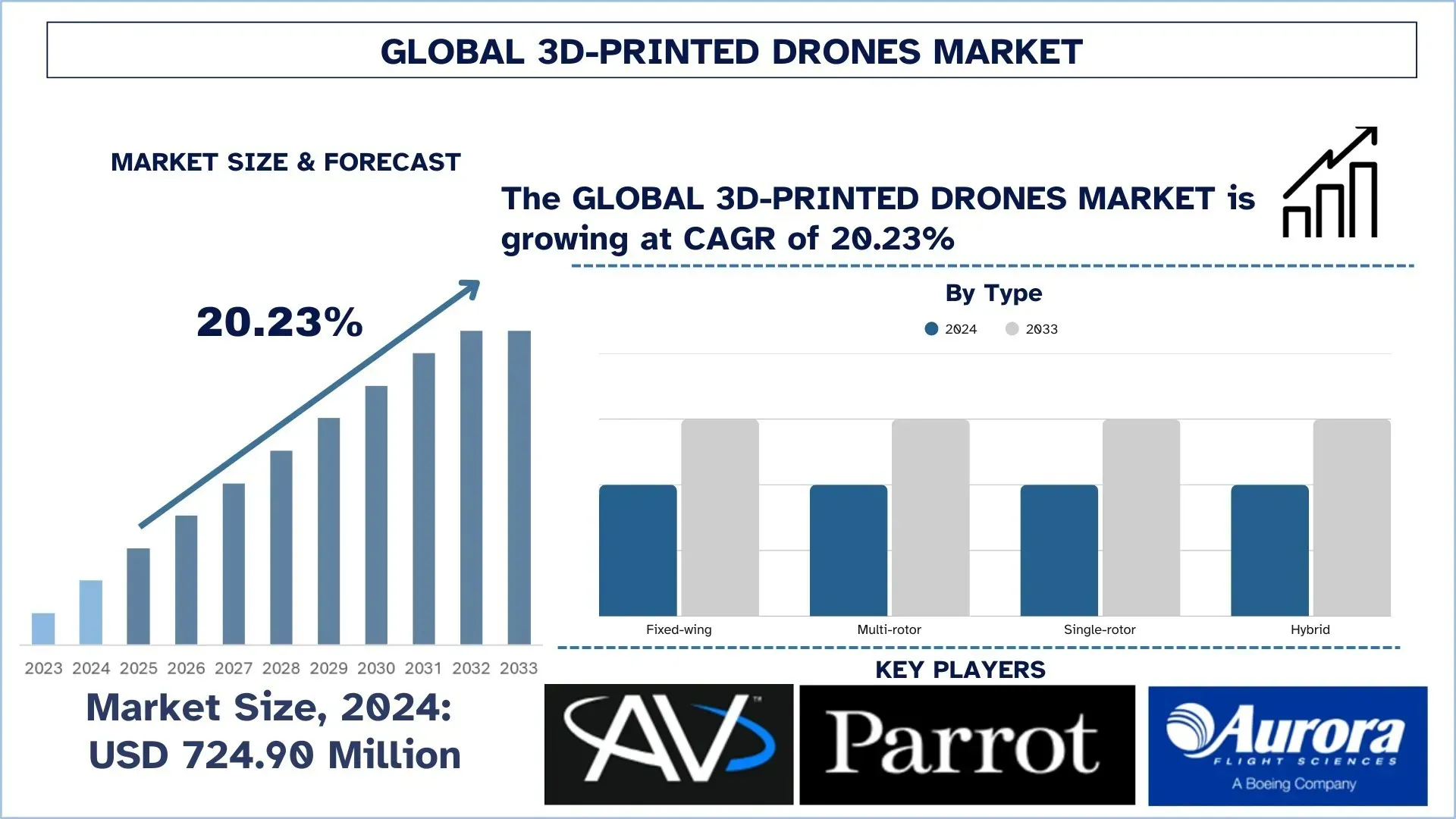

Global 3D-Printed Drones Market Size & Forecast

The Global 3D-Printed Drones Market was valued at USD 724.90 million in 2024 and is expected to grow at a robust CAGR of around 20.23% during the forecast period (2025-2033F), due to armed forces globally adopting 3D-printed drones for surveillance, reconnaissance, and tactical missions due to their modularity and fast production capabilities.

3D-Printed Drones Market Analysis

The advancement of 3D-printed drones marks an important development that produces flexible unmanned aerospace and robotic systems that are accessible at low cost across multiple sectors. The market enables revolutionary changes to modern aerial operations through its simultaneous delivery of rapid prototyping with design flexibility and material efficiency capabilities. Technology enables rapid production of low-cost intricate components, which accelerates simple drone part prototyping. Applications exist in defense operations as well as agriculture and logistics sectors, and environmental checks and emergencies. Drone technology has transformed market delivery schedules while creating independent supply networks and advancing creative industrial processes throughout different sectors. Their requirements call for drones that are lightweight with aerodynamic design and quick mission profile adaptation through the possibilities provided by additive manufacturing. Unmatched deployment speed and customizable operations are the key advantages of drones printed by 3D technology. The rising product demand results from breakthroughs in composite materials and Artificial Intelligence-controlled navigation systems, as well as drone usage in enterprise operations and smart city infrastructure. In April 2024, the U.S. Air Force demonstrated its capability to create fully functional 3D-printed unmanned aerial systems (UAS), which required only 24 hours from design until deployment at Eglin Air Force Base, Florida. The demonstration from the Blue Horizons fellowship program showed six drone assemblies, including an 8-pound personnel recovery system, that took only 22.5 hours to complete. The Black Phoenix team partnered with Titan Dynamics to leverage automated design software, which optimized drone aerodynamics within less than 10 minutes.

Global 3D-Printed Drones Market Trends

This section discusses the key market trends that are influencing the various segments of the global 3D printed drones market, as found by our team of research experts.

Integration of Lightweight Composite Materials

Among the major trends in the 3D-printed drones market, the integration of lightweight composite materials is the most prominent one. These materials include carbon-fiber-reinforced polymers and advanced thermoplastics. These materials are lightweight, highly strong further contribute to doing so much in giving drones flight duration, payload capacity, and maneuverability. The first Australian UAV company, Carbonix, pioneered the application of carbon-reinforced FDM printing in the manufacture of long-endurance UAVs for environmental monitoring and surveying. In March 2024, the company cut turnaround time by 60% and realized major weight savings per drone, thus actually improving air efficiency and durability of operations in a demanding work environment. Similarly, aerospace research houses are investigating generative design software in conjunction with additive manufacturing to come up with drones having lattice structures and internal geometries that minimize material usage and maximize strength. This not only revolutionizes how drones are aerodynamically designed and made to be sturdy, but it also fits well with the global sustainability agenda by cutting material waste and carbon footprint during manufacturing.

3D-Printed Drones Industry Segmentation

This section provides an analysis of the key trends in each segment of the global 3D printed drones market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Multi-Rotor Drones Market Dominates the 3D-Printed Drones Market

Based on type, the 3D-printed drones market is segmented into Fixed-wing, Multi-rotor, Single-rotor, and Hybrid. In 2024, the multi-rotor 3D-printed drones market dominated and is expected to maintain its leading position throughout the forecast period. The ever-burgeoning growth of multi-rotor unmanned aerial vehicles is attributable to their high versatility, stability, and ease of modification in design achieved through additive manufacturing. Multi-rotor drones are best suited for applications that require hovering, vertical take-off and landing (VTOL), and precise maneuvering, such as in aerial photography, surveillance, inspection, and delivery. 3D printing in this domain allows for a lightweight yet strong frame, fast prototyping, and an economical production method- a necessity in the commercial and defense sectors where customization for specific missions and rapid deployment is critical. Furthermore, the growth of the segment is also supported by increased funding into AI-integrated drones, improvements in batteries, and the increased demand for on-demand manufacturing capability. The possibilities for rapid customization of the drone components for unique flying needs have favored 3D-printed multi-rotor drones across various industries, including agriculture, urban logistics, and disaster response.

The Airframe Segment Dominates the 3D-Printed Drones Market.

Based on components, the 3D-printed drones market is segmented into Airframe, Wings, Landing Gears, Propellers, Mounts & Holders, and Others. The airframe segment held the largest market share in 2024. The Airframe is the most important structure on any drone, holding mission-critical systems such as propulsion, navigation, and payload support. 3D printing has then switched the manufacturing of airframes from a long and expensive procedure to a very rapid and cheap one, making this field very central to scaling the drone production industry through the production of lightweight, strong, and aerodynamically pleasing designs. The demand is further driven by the ability to customize airframes for special jobs, ranging from surveillance to delivery, agriculture spraying, and infrastructure inspection. Frameworks developed through additive manufacturing are such as carbon fiber-reinforced polymers and high-strength thermoplastics, both of which greatly improve the structural integrity while not adding too much weight. Another aspect that 3D printed airframes have is modularity. Maintenance will also comprise faster iterations and field repairs that minimize downtime of the machines as well as the costs of operations. In ensuring that future airframe components are designed for adaptability, efficiency, and high-performance drone systems, the advances cover operational drones in the commercial, defense, and emergency response processes.

North America Dominated the Global 3D-Printed Drones Market

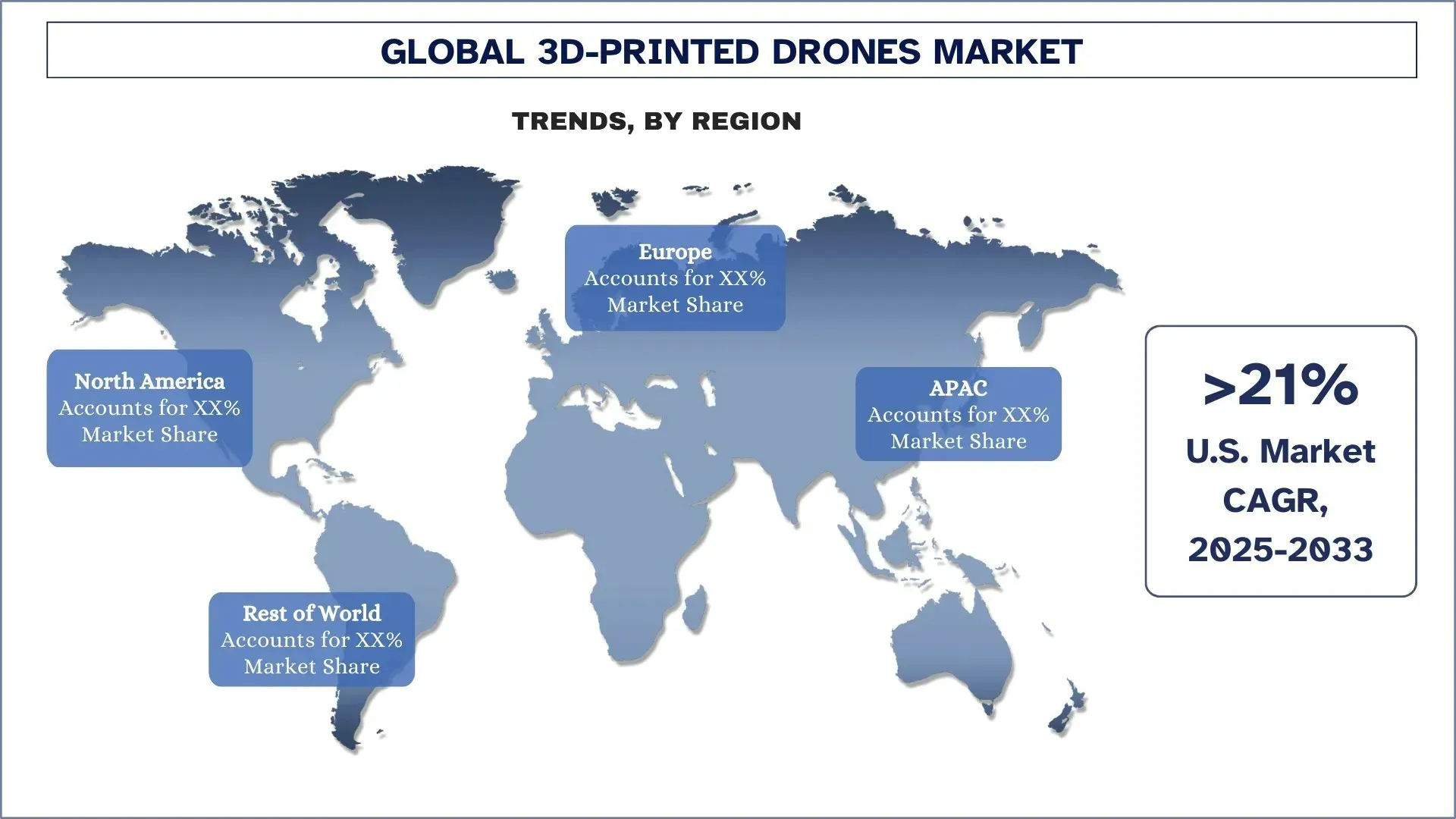

The North America 3D-printed drones market dominated the global 3D-printed drones market in 2024 and is forecasted to remain in this position in the forecast period. This is due to the early adoption of this technology in the aerospace and defense industry, and especially in designing drones, and the wide presence of manufacturers. Additionally, the United States and its agencies, such as the U.S. Department of Defense, have consistently invested in the latest technology, like 3D printing, through initiatives like the Defense Innovation Unit (DIU) and partnerships with startups and academic institutions. For instance, in January 2025, the U.S. Air Force assigned a 5-year contract to Firestorm Labs of a USD 100 million IDIQ contract for the development of 3D-printed unmanned aerial systems (UAS). The contract supports modular designs with advanced autonomy, the focus is Group 1-3 UAS for intelligence, surveillance, and tactical support. Firestorm Labs will perform work under the contract until December 16, 2031, using additive manufacturing for local production to avoid dependencies on the supply chain. On the other side, the agencies are employing other services and applications under the application of 3D-printed drones. Surveillance, disaster response, and tactical operations by the U.S. Customs and Border Protection, FEMA, and local law enforcement, with these other areas of applications, the technology finds increased acceptance in government sectors. North America has dominated the field of real-world testing and deployment of 3D-printed drone systems. Test programs in agriculture, logistics (last-mile delivery), and infrastructure monitoring give live data and case studies that push more investments and scaling.

U.S. held a dominant Share of the North America 3D-Printed Drones Market in 2024

The USA leads the 3D-printed drones market, supported by a developed defense setup, a strong additive manufacturing ecosystem, and heavy investments in aerospace R&D. U.S. military bodies give priority to rapid prototyping and deployment of drones for mission-oriented purposes, for which 3D printing fits perfectly as it is fast and can be produced locally. Establishments such as Lockheed Martin and Raytheon, alongside upcoming companies such as Firestorm Labs, are pushing further advancements in 3D printing within tactical drone systems. Further enhancing their advantage, U.S. governmental efforts like the Blue sUAS program champion secure, locally manufactured UAVs.

3D-Printed Drones Competitive Landscape

The global 3D-Printed Drones market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top 3D-Printed Drones Companies

Some of the major players in the market are AeroVironment, Inc., Parrot Drones SAS, AURORA FLIGHT SCIENCES (A Boeing Company), RapidFlight, Northrop Grumman, Firestorm Labs, Inc., Skydio, Inc., BAE Systems, DJI, and General Atomics.

Recent Developments in the 3D-Printed Drones Market

In February 2025, AeroVironment awarded its third delivery order for Switchblade loitering munition systems, valued at USD 288 million, under a multi-year USD 990 million contract with the US Army.

In January 2025, Kratos Defense & Security Solutions secured a USD 34.8 million contract expansion with the US Marine Corps to enhance the XQ-58A Valkyrie Unmanned Aerial System (UAS). The expansion supports mission system integration for the Marine Corps' Tactical Aircraft initiative.

In April 2024, Firestorm Labs, Inc. secured USD 12.5 million in seed funding. The investment round was led by Lockheed Martin Ventures and included notable defense investors. The investment is intended to advance Firestorm Labs’ drone manufacturing technologies to meet the demands of modern warfare and improve interoperability for defense applications.

In 2023, Boeing unveiled a new line of unmanned aerial vehicles (UAVs) that incorporate 3D-printed components, enhancing performance and reducing production costs.

Global 3D-Printed Drones Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 20.23% |

Market size 2024 | USD 724.90 Million |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | North America is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, South Korea, and India |

Companies profiled | AeroVironment, Inc., Parrot Drones SAS, AURORA FLIGHT SCIENCES (A Boeing Company), RapidFlight, Northrop Grumman, Firestorm Labs, Inc., Skydio, Inc., BAE Systems, DJI, and General Atomics |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Type, By Component, By Technology, By Application, By Region/Country |

Reasons to Buy the 3D-Printed Drones Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional-level analysis of the industry.

Customization Options:

The global 3D printed drones market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global 3D-Printed Drones Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global 3D printed drones market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the 3D printed drones value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global 3D printed drones market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including type, component, technology, application, and regions within the global 3D printed drones market.

The Main Objective of the Global 3D-Printed Drones Market Study

The study identifies current and future trends in the global 3D printed drones market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current market size and forecast the market size of the global 3D printed drones market and its segments in terms of value (USD).

3D-Printed Drones Market Segmentation: Segments in the study include areas of type, component, technology, application, and regions.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the 3D printed drones industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the 3D printed drones market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global 3D printed drones market current market size and its growth potential?

The global 3D printed drones market was valued at USD 724.90 million in 2024 and is expected to grow at a CAGR of 20.23% during the forecast period (2025-2033).

Q2: Which segment has the largest share of the global 3D printed drones market by Type?

The multi-rotor market dominated the market and is expected to maintain its leading position throughout the forecast period. The growth of multi-rotor unmanned aerial vehicles is attributable to their high versatility, stability, and ease of modification in design achieved through additive manufacturing.

Q3: What are the driving factors for the growth of the global 3D printed drones market?

• Demand for Rapid Prototyping & Customization: 3D printing enables faster design iterations and mission-specific drone configurations, reducing time-to-market and enabling mass customization.

• Increased Military and Defense Applications: Armed forces globally are adopting 3D-printed drones for surveillance, reconnaissance, and tactical missions due to their modularity and fast production capabilities.

• Growing Use in Commercial Sectors: Industries such as agriculture, logistics, mining, and infrastructure are deploying drones with 3D-printed components to reduce costs and enhance operational efficiency.

Q4: What are the emerging technologies and trends in the global 3D printed drones market?

• Integration of Lightweight Composite Materials: Growing use of carbon fiber-infused filaments and thermoplastics to enhance flight endurance and payload capacity.

• Localized and On-Demand Manufacturing: Military and industrial users are setting up mobile 3D printing labs to produce drones or parts near deployment zones.

• AI-Driven Drone Design Optimization: Use of AI and generative design in creating aerodynamically optimized structures that are 3D-printed with minimal material waste.

Q5: What are the key challenges in the global 3D printed drones market?

• High Initial Investment in Industrial-Grade 3D Printers: Although desktop 3D printers are affordable, high-performance systems suitable for drone manufacturing remain capital-intensive for small companies.

• Structural Limitations of Printed Materials: While improving, 3D-printed plastics and composites often lack the strength and durability of traditional aerospace-grade materials under extreme conditions.

• Lack of Standardization in Drone Parts and Printing Processes: The absence of industry-wide standards for 3D-printed UAV parts creates interoperability and quality assurance challenges.

Q6: Which region dominates the global 3D printed drones market?

The North America 3D-printed drones market dominated the global 3D-printed drones market in 2024 and is forecasted to remain in this position in the forecast period. This is due to the early adoption of this technology in the aerospace and defense industry, and especially in designing drones, and the wide presence of manufacturers. Additionally, the United States and its agencies, such as the U.S. Department of Defense, have consistently invested in the latest technology, like 3D printing, through initiatives like the Defense Innovation Unit (DIU) and partnerships with startups and academic institutions. For instance, in January 2025, the U.S. Air Force assigned a 5-year contract to Firestorm Labs of a USD 100 million IDIQ contract for the development of 3D-printed unmanned aerial systems (UAS). The contract supports modular designs with advanced autonomy, the focus is Group 1-3 UAS for intelligence, surveillance, and tactical support. Firestorm Labs will perform work under the contract until December 16, 2031, using additive manufacturing for local production to avoid dependencies on the supply chain.

Q7: Who are the key players in the global 3D printed drones market?

Some of the leading 3D Printed Drones Companies include:

• AeroVironment, Inc.

• Parrot Drones SAS

• AURORA FLIGHT SCIENCES ( A Boeing Company)

• RapidFlight

• Northrop Grumman

• Firestorm Labs, Inc

• Skydio, Inc.

• BAE Systems

• DJI

• General Atomics

Q8 How does the regulatory environment impact the commercialization and adoption of 3D-printed Drones across different regions?

• Certification Hurdles: Regulatory bodies like the FAA (U.S.) and EASA (Europe) impose strict airworthiness standards for 3D-printed drone components, slowing time-to-market. For instance, in 2023, the FAA’s delayed certification of 3D-printed structural parts temporarily hindered U.S.-based drone manufacturers.

• Regional Disparities: Countries with flexible regulations (e.g., UAE, Singapore) are becoming testbeds for rapid deployment, while stricter regions (e.g., EU) face slower adoption. DJI’s compliance with China’s relaxed drone laws enabled faster scaling of its 3D-printed Agras crop-spraying drone.

• Investor Implications: Companies navigating regulatory complexities successfully (e.g., through pre-certified material partnerships) gain investor trust, as seen with Relativity Space’s $1.2B valuation after securing military contracts with compliant designs.

Q9: What roles do strategic partnerships and collaborations play in accelerating innovation in the 3D-Printed Drones market?

• Technology Synergies: Collaborations between 3D printing firms (e.g., Stratasys) and drone manufacturers (e.g., Parrot) integrate advanced materials (like Antero 800NA) into UAV designs, enhancing durability. Airbus’ partnership with Materialise reduced drone production costs by 30% through optimized printing processes.

• Market Access: Joint ventures, like Boeing’s alliance with Safran for 3D-printed military drones, help penetrate defense sectors with established supply chains. Similarly, start-ups like Carbon3D partnered with Siemens to access industrial clients.

• Investor Confidence: Strategic alliances signal market validation and scalability. Investors favored Beta Technologies after its collaboration with Archer Aviation to develop 3D-printed air taxis, reflecting confidence in cross-industry innovation.

Related Reports

Customers who bought this item also bought

Aeroderivative Sensor Market: Current Analysis and Forecast (2025-2033)

Emphasis on Sensor Type (Temperature Sensors, Pressure Sensors, Vibration Sensors, Flame Sensors, and Others); Service Provider (OEMs and Aftermarket); End-User (Industrial, Marine, Aerospace & Defense, Power & Energy, and Oil & Gas); and Region/Country

Kamikaze Drone Market: Current Analysis and Forecast (2026-2034)

Emphasis on Type (Fixed-wing System and Rotary-wing System); Range (Short range(10-20km), Medium range(20-100km), and Long range(>100km)); Platform (Ground based, Airborne, and Naval); Autonomy (Man in the loop and Fully Autonomous); and Region/Country

Counter-Unmanned Aerial System Market: Current Analysis and Forecast (2025-2033)

Emphasis on Platform (Ground-Based Systems, Airborne Systems, and Naval / Maritime Systems); Technology (Radar, RF, EO/IR, Laser, Kinetic, and Others); End-Use (Defense & Military, Homeland Security & Law Enforcement, Critical Infrastructure, and Commercial & Industrial); and Region/Country

Middle East & Africa Turboprop Aircraft Market: Current Analysis and Forecast (2025-2033)

Emphasis By Aircraft Type (Light Turboprop Aircraft, Medium Turboprop Aircraft, and Heavy Turboprop Aircraft), by End-User (Government & Defense, Commercial Operators, and Private Operators), By Country (Saudi Arabia, UAE, Egypt, South Africa, Turkey, Israel, and the Rest of Middle East & Africa)