- Home

- About Us

- Industry

- Services

- Reading

- Contact Us

Ultra-Thin Glass Market: Current Analysis and Forecast (2025-2033)

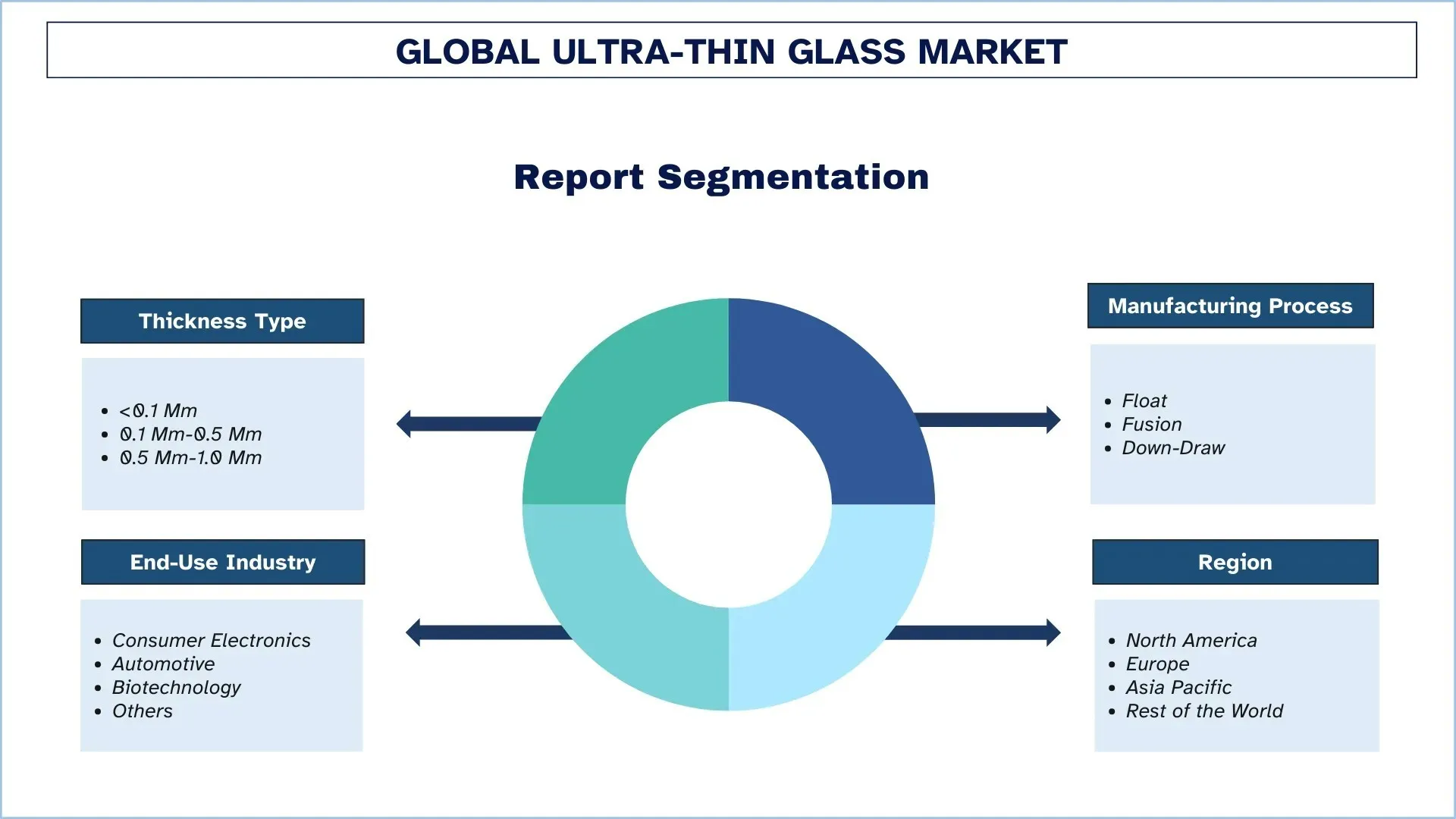

Emphasis on Thickness Type (<0.1 Mm, 0.1 Mm-0.5 Mm, and 0.5 Mm-1.0 Mm); Manufacturing Process (Float, Fusion, and Down-Draw); End-Use Industry (Consumer Electronics, Automotive, Biotechnology, and Others); and Region/Country

Global Ultra-Thin Glass Market Size & Forecast

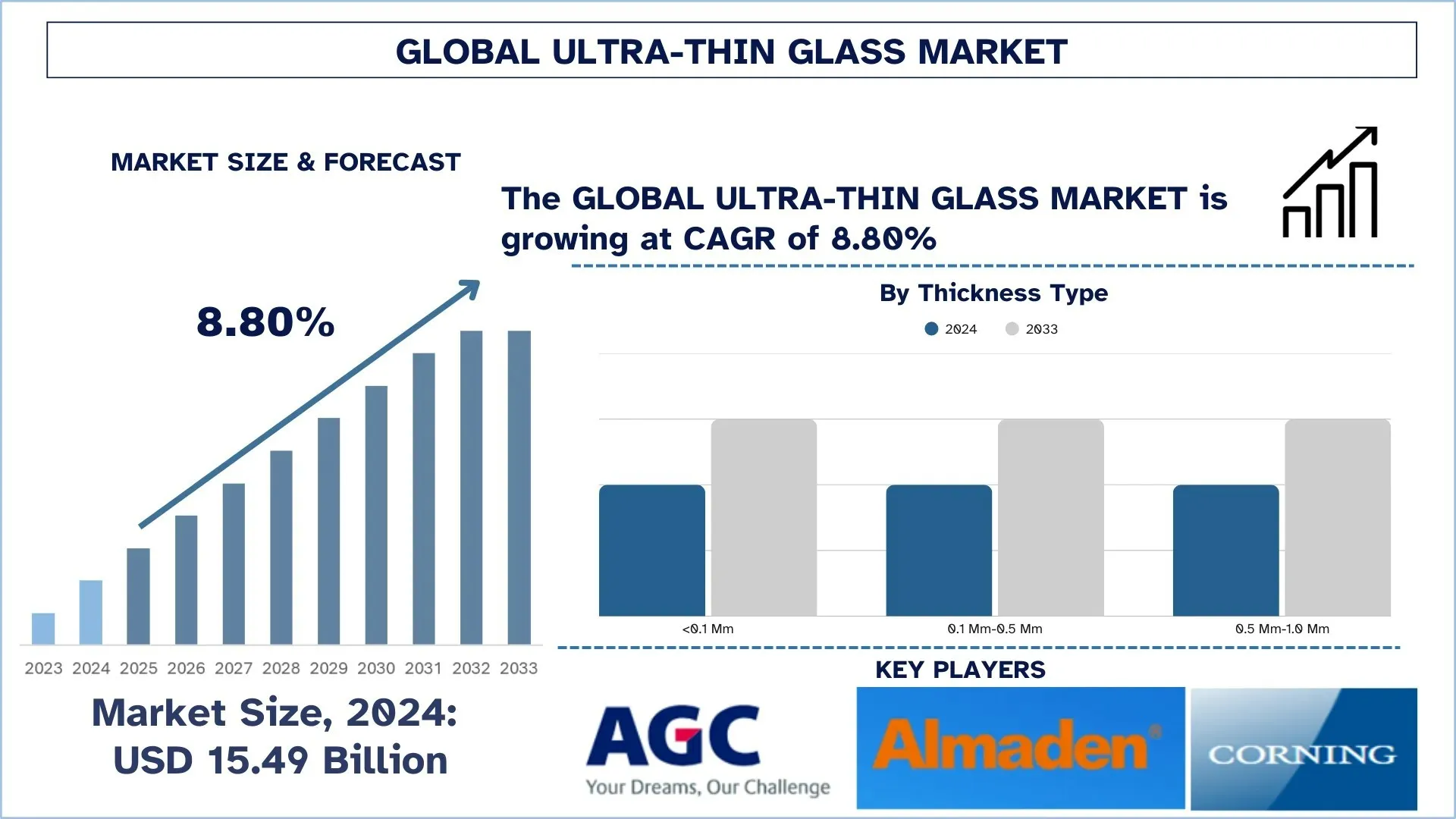

The Global Ultra-Thin Glass market was valued at USD 15.49 billion in 2024 and is expected to grow at a robust CAGR of around 8.80% during the forecast period (2025-2033F), due to the rising adoption in smartphones, tablets, and wearables fuels demand for ultra-thin, bendable glass. Additionally, Ultra-thin glass enhances signal transparency and durability in 5G-enabled electronics.

Ultra-Thin Glass Market Analysis

The major factors affecting the growth of the ultra-thin glass market are the demand for lightweight, durable, and flexible materials across various industries such as electronics, automobile, and solar energy. The adoption of ultra-thin glass in smartphones, tablets, and wearables due to its higher scratch resistance and optical clarity forms one of the major drivers in the market. Therefore, the ongoing trend of energy-efficient solutions has driven its use in solar panels, where ultra-thin glass aids in enhancing efficiency while remaining light-weight. Furthermore, one of the major industries that is growing globally is automotive, where the burgeoning adoption of electric vehicles and the development of autonomous vehicles has further created the demand. In the automotive sector, ultra-thin glasses are used in heads-up displays and touchscreen panels for better aesthetics and functionality. With the evolution in glass manufacturing technologies, such as chemically strengthened and bendable glass, new applications are being explored for it. Also, stringent regulations are encouraging the use of ultra-thin glass by promoting materials that are energy-efficient and environmentally friendly. At large, the market is expected to grow significantly considering the developments and demand for newer applications in various sectors.

Global Ultra-Thin Glass Market Trends

This section discusses the key market trends that are influencing the various segments of the global ultra-thin glass market, as found by our team of research experts.

Increased Investment in AR/VR and Micro displays

One more accelerating trend includes the use of ultra-thin glass in AR, VR, and XR systems. Spatial computing and wearable displays have entered critical positions in gaming, healthcare, training, and defense. Lightweight, high-resolution micro displays are therefore in demand. Ultra-thin glass, especially below 0.2 mm in thickness, is crucial for providing 3500+ resolution on OLED-on-silicon panels, as has recently been demonstrated by companies such as Samsung Display. These glasses give adequate thermal and optical results and maintain ultralight weight, paramount for comfort during prolonged wear and for an immersive experience.

Lead-Free and Eco-Friendly Glass Compositions

Environmental sustainability is becoming an increasing consideration in the area of ultra-thin glass. Resin manufacturers are veering away from old formulations with lead or otherwise containing harmful substances in favor of environmentally friendly, lead-free alternatives. Now the products contain oxides of barium, boron, and bismuth and certify RoHS and green building certifications without compromising on the actual performance. For example, manufacturers in Europe and Japan have taken the green road, developing an ultra-thin glass that is fully recyclable and equipped with anti-reflective and anti-fingerprint technologies for use in both consumer electronics and architectural applications. This trend has increasingly gone into development amidst ESG (Environmental, Social, and Governance) policies to promote clean, safer supply chains.

Global Ultra-Thin Glass Industry Segmentation

This section provides an analysis of the key trends in each segment of the global ultra-thin glass market report, along with forecasts at the global, regional, and country levels for 2024-2032.

The 0.1 Mm-0.5 Mm Segment Dominates the Ultra-Thin Glass Market

Based on thickness type, the ultra-thin glass market is segmented into <0.1 Mm, 0.1 Mm-0.5 Mm, and 0.5 Mm-1.0 Mm. In 2024, the 0.1 Mm-0.5 Mm segment dominated and is expected to maintain its leading position throughout the forecast period. This is due to the glass achieving an optimal balance between flexibility and durability, making it most suited for diverse applications, which include applications for smartphones, tablets, automotive displays, as well as solar panels. Ultra-thin glass thinner than 0.1 mm may be too frail to mass-produce, and that thicker than 0.5 mm could be too rigid. Hence, the 0.1 mm to 0.5 mm range offers just the right balance in strength, lightweight, and cost-effectiveness. The widening, folding, and curved displays demand in consumer electronics drives this segment. The automotive sector is also increasingly using ultra-thin glass for HUD and touchscreen panels where mechanical strength and optical clarity are of prime importance. Solar technology contributes towards the agent with this thickness range as it enhances photovoltaic efficiency while decreasing module weight. In addition to that, chemical strengthening and anti-reflective coatings have made possible an improvement in ultra-thin glass applications within this segment, growing abundance in its resistance to scratches and optical clarity. Increased investment in flexible electronics and smart devices will further aid the segment's growth of 0.1 mm–0.5 mm, thereby further cementing its dominance in the ultra-thin glass market.

The Fusion Segment Dominates the Ultra-Thin Glass Market.

Based on the manufacturing process, the ultra-thin glass market is segmented into Float, Fusion, and Down-Draw. The fusion segment held the largest market share in 2024 and is expected to behave in the same fashion in the forecast period. Fusion-drawn glass holds the appellation of leadership for the highest optical quality, surface smoothness, and thermal stability, making it the favored choice for the finest materials in flexible displays, OLED screens, and advanced touch panels. The marketing of foldable smartphones, wearable devices, and next-generation TV is booming in tremendous perspectives, bolstering the demand for fusion ultra-thin glass, which has no rival in thinness (less than 0.1 mm) without imparting a disadvantage in strength or clarity. On the other hand, the increasingly phenomenal automotive demand provides another big selling story, which places fusion glass in curved infotainment displays and augmented reality HUDs, where distortion is simply intolerable. Additionally, manufacturers are also looking for chemical strengthening to help toughen levels in fusion glass, making it usable in ruggedized electronics and medical equipment. With 5G technology and IoT-enabled devices gaining momentum, the demand for ultra-thin and high-performance glass substrates is hitting the next gear, thus further cementing the fusion segment's lead.

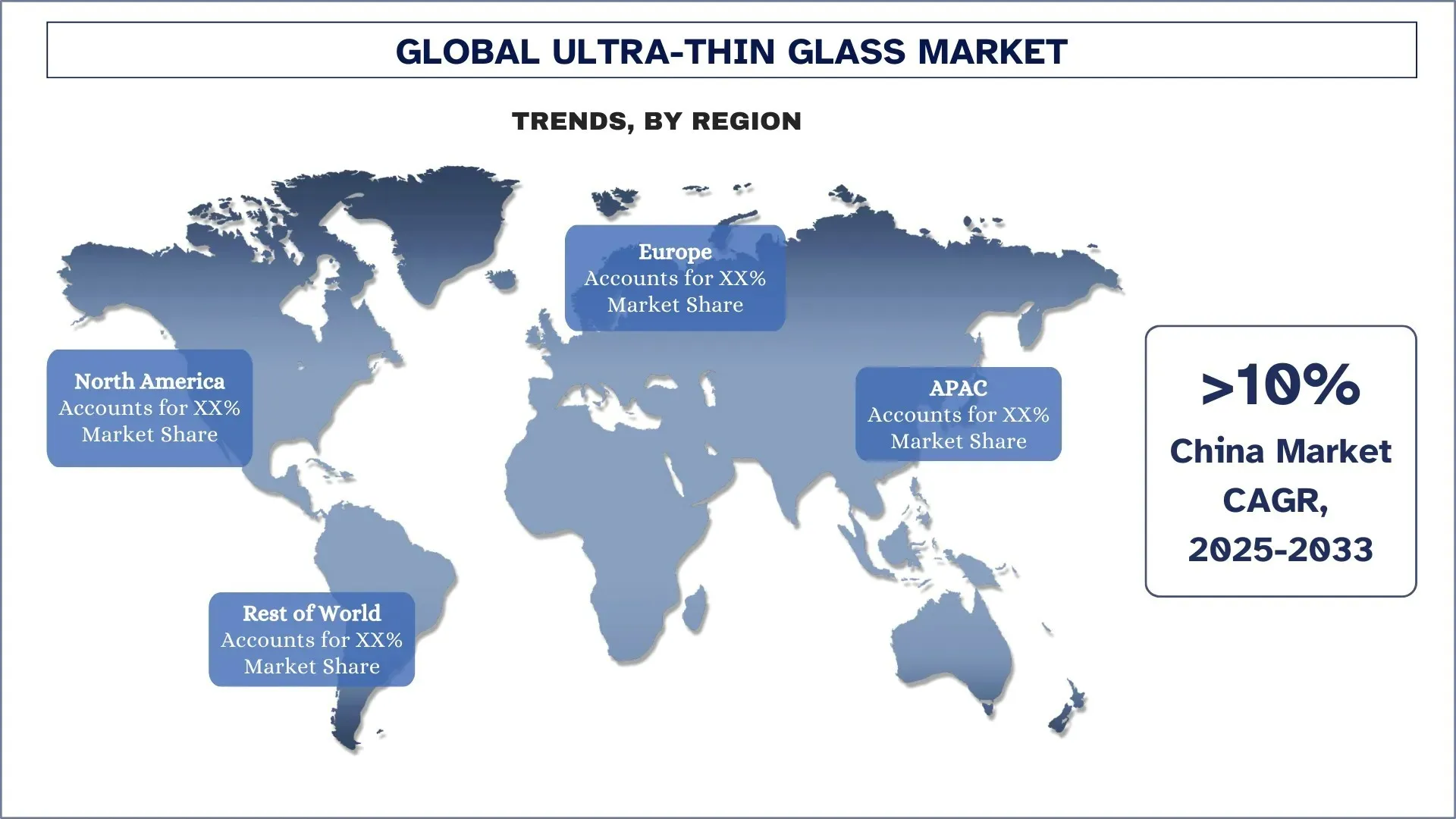

Asia Pacific Dominated the Global Ultra-Thin Glass Market

The Asia Pacific ultra-thin glass market dominated the global ultra-thin glass market in 2024 and is forecasted to remain in this position in the forecast period. The region is dominant because of a strong manufacturing ecosystem, high consumer electronics production, and fast urbanization. China, South Korea, and Japan are the global centers for the industries producing smartphones, display panels, and semiconductors, where ultra-thin glass is quite significant in one of its forms of optical clarity, flexibility, and durability. The ultra-thin glass demand has seen a significant boost with the ever-expanding China's ecosystem of electronics manufacturing and increased domestic consumption of top-of-the-line smart devices. The R&D and innovation for high-precision glass are still dominated by South Korea and Japan, using their technical advantages in supporting foldable and flexible display technologies. It enjoys the advantage of a skilled workforce and government-aided initiatives aiming at digital transformation and sustainable manufacturing. For example, Japan is making a bold move in the global renewable energy race by investing USD 1.5 billion in the commercialization of next-generation perovskite solar technology in February 2025. Unlike their silicon counterparts, perovskite solar cells are 20 times thinner, lighter, and flexible, enabling installation on a variety of urban surfaces ranging from stadiums and airports to office buildings.

China held a dominant Share of the Asia Pacific Ultra-Thin Glass Market in 2024

China led the ultra-thin glass industry in 2024, supported by a strong consumer electronics manufacturing ecosystem, cost-efficient production facilities, and strong domestic demand for advanced devices. Considered home to some of the most important smartphone and display panel manufacturers, enjoying the advantages of industry-wide economies of scale, vertical integration, and quick commercial acceptance of foldable and flexible displays, the country is well-placed in this sector. The country also benefits from government support for high-tech industries, thereby focusing on R&D and automation with large investments. With increasing domestic demands for medical diagnostics and solar technologies, the demand for ultra-thin glass is being further strengthened. Furthermore, the presence of important suppliers of raw materials and research facilities in China assures its leadership in the global landscape.

Ultra-Thin Glass Competitive Landscape

The global Ultra-Thin Glass market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top Ultra-Thin Glass Companies

Some of the major players in the market are AGC Inc., Changzhou Almaden Co., Ltd., Corning Incorporated, CSG Holding Limited, Emerge Glass India Pvt. Ltd., SCHOTT AG, Nippon Electric Glass Co., Ltd., TAIWAN GLASS IND. CORP., Xinyi Glass Holdings Limited, and Noval Glass.

Recent Developments in the Ultra-Thin Glass Market

In April 2024, Glass Acoustic Innovations Ltd. (GAIT) partnered with Nippon Electric Glass Co. (NEG) to bring to the audio world a thin glass diaphragm technology. The collaboration led to applications of glass diaphragms in Hi-fi speakers, headphones, and automotive audio systems to give them better strength, rigidity, and ways to deliver sound.

In February 2025, with the backend of a seller Lens Technology with China, Apple stepped onto launch the first foldable device. Lens Technology will procure 70% of the Ultra-Thin Glass (UTG) for Apple, with Corning as the raw material supplier. The ultra-thin glass will be placed at the center for enhanced flexibility around the device's hinge.

Global Ultra-Thin Glass Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 8.80% |

Market size 2024 | USD 15.49 Billion |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | Asia Pacific is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, South Korea, and India |

Companies profiled | AGC Inc., Changzhou Almaden Co., Ltd., Corning Incorporated, CSG Holding Limited, Emerge Glass India Pvt. Ltd., SCHOTT AG, Nippon Electric Glass Co., Ltd., TAIWAN GLASS IND. CORP., Xinyi Glass Holdings Limited, and Noval Glass |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Thickness Type, By Manufacturing Process, By End-Use Industry, By Region/Country |

Reasons to Buy the Ultra-Thin Glass Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional-level analysis of the industry.

Customization Options:

The global ultra-thin glass market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global Ultra-Thin Glass Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global ultra-thin glass market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the ultra-thin glass value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global ultra-thin glass market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including thickness type, manufacturing process, end-use industry, and regions within the global ultra-thin glass market.

The Main Objective of the Global Ultra-Thin Glass Market Study

The study identifies current and future trends in the global ultra-thin glass market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current market size and forecast the market size of the global ultra-thin glass market and its segments in terms of value (USD).

Ultra-Thin Glass Market Segmentation: Segments in the study include areas of thickness type, manufacturing process, end-use industry, and regions.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the ultra-thin glass industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the ultra-thin glass market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global ultra-thin glass market current market size and its growth potential?

The global ultra-thin glass market was valued at USD 15.49 billion in 2024 and is expected to grow at a CAGR of 8.80% during the forecast period (2025-2033).

Q2: Which segment has the largest share of the global ultra-thin glass market by Thickness Type?

The 0.1 Mm-0.5 Mm segment dominated and is expected to maintain its leading position throughout the forecast period. This is due to the glass achieving an optimal balance between flexibility and durability, making it most suited for diverse applications, which include applications for smartphone, tablets, automotive displays, as well as solar panels.

Q3: What are the driving factors for the growth of the global ultra-thin glass market?

• Growing Demand for Foldable & Flexible Displays: Rising adoption in smartphones, tablets, and wearables fuels demand for ultra-thin, bendable glass.

• Expansion of 5G & IoT Devices: Ultra-thin glass enhances signal transparency and durability in 5G-enabled electronics.

• Automotive Industry Shift to Smart Glass: Increasing use in HUDs, touchscreen dashboards, and sunroofs drives market growth.

Q4: What are the emerging technologies and trends in the global ultra-thin glass market?

• Lead-Free & Eco-Friendly Glass: Demand for sustainable, non-toxic shielding glass in medical and nuclear applications is on the rise.

• Increased Investment in AR/VR and Micro displays: As AR/VR adoption grows, demand for ultra-thin glass in high-PPI micro displays (used in headsets and goggles) is accelerating.

• Shift Toward Transparent and Flexible Electronics: Transparent displays, touch sensors, and flexible printed circuits are gaining traction, requiring ultra-thin glass with high optical clarity and bendability.

Q5: What are the key challenges in the global ultra-thin glass market?

• High Production Costs: Precision cutting, handling, and coating of ultra-thin glass can be complex and expensive, limiting access for smaller players.

• Fragility & Handling Difficulties: Despite being engineered for flexibility, ultra-thin glass remains fragile and prone to cracking under stress.

• Supply Chain Constraints: Shortages of high-purity raw materials and supply chain disruptions can affect production scalability and pricing.

Q6: Which region dominates the global ultra-thin glass market?

The Asia Pacific ultra-thin glass market dominated the global ultra-thin glass market in 2024 and is forecasted to remain in this position in the forecast period. The region is dominant because of a strong manufacturing ecosystem, high consumer electronics production, and fast urbanization. China, South Korea, and Japan are the global centers for the industries producing smartphones, display panels, and semiconductors, where ultra-thin glass is quite significant in one of its forms of optical clarity, flexibility, and durability. The ultra-thin glass demand has seen a significant boost with the ever-expanding China's ecosystem of electronics manufacturing and increased domestic consumption of top-of-the-line smart devices. The R&D and innovation for high-precision glass are still dominated by South Korea and Japan, using their technical advantages in supporting foldable and flexible display technologies. It enjoys the advantage of a skilled workforce and government-aided initiatives aiming at digital transformation and sustainable manufacturing.

Q7: Who are the key players in the global ultra-thin glass market?

Some of the Major ultra-thin glass companies include:

• AGC Inc.

• Changzhou Almaden Co., Ltd.

• Corning Incorporated

• CSG Holding Limited

• Emerge Glass India Pvt. Ltd.

• SCHOTT AG

• Nippon Electric Glass Co., Ltd.

• TAIWAN GLASS IND. CORP.

• Xinyi Glass Holdings Limited

• Noval Glass

Q8: How critical is vertical integration in the ultra-thin glass supply chain?

Cost Efficiency: Vertically integrated players streamline raw material sourcing, processing, and finishing, reducing production costs and lead times.

• Quality Control: End-to-end control ensures consistency in thickness, clarity, and mechanical critical in high-precision applications like foldable displays.

• Faster Customization: In-house R&D and fabrication capabilities accelerate prototyping and adaptation to OEM specifications, enhancing competitiveness.

Q9: How do regulatory and ESG frameworks shape strategic direction?

• Sustainability Alignment: ESG-conscious buyers prefer recyclable, lead-free glass, prompting a shift toward green-certified materials.

• Compliance-Driven Design: Regulations like REACH and RoHS mandate non-toxic compositions, directly influencing product formulations.

• Reputation & Access: Adherence to environmental and worker safety standards enhances brand image and facilitates access to international markets.

Related Reports

Customers who bought this item also bought