- Home

- About Us

- Industry

- Services

- Reading

- Contact Us

Indoor 5G Market: Current Analysis and Forecast (2025-2033)

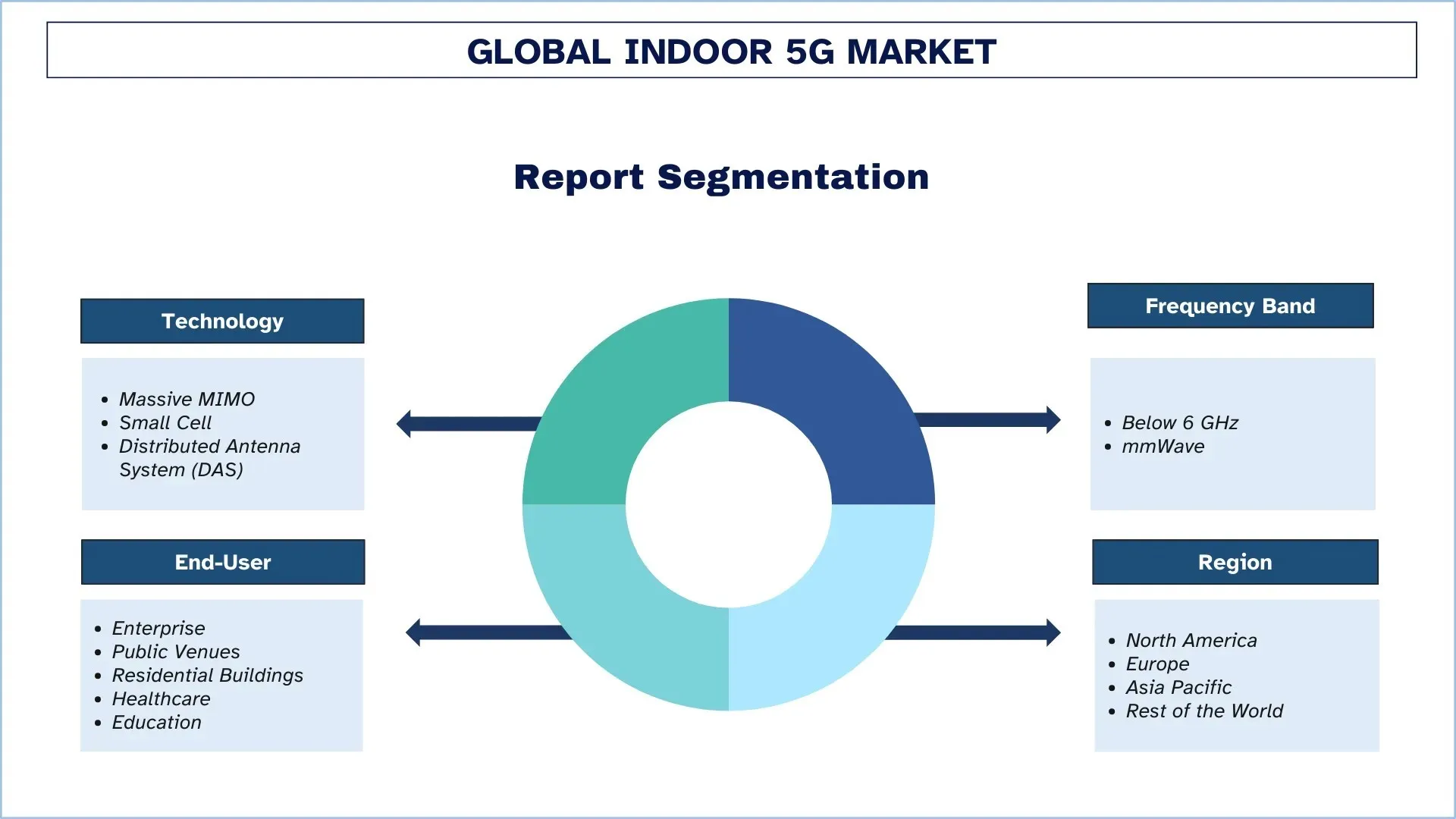

Emphasis on Technology (Massive MIMO, Small Cell, and Distributed Antenna System (DAS)); Frequency Band (Below 6 GHz and mmWave); End-User (Enterprise (Commercial Buildings, Manufacturing Units, etc)), Public Venues (Stadiums, Airports, etc.), Residential Buildings, Healthcare, and Education); and Region/Country

Global Indoor 5G Market Size & Forecast

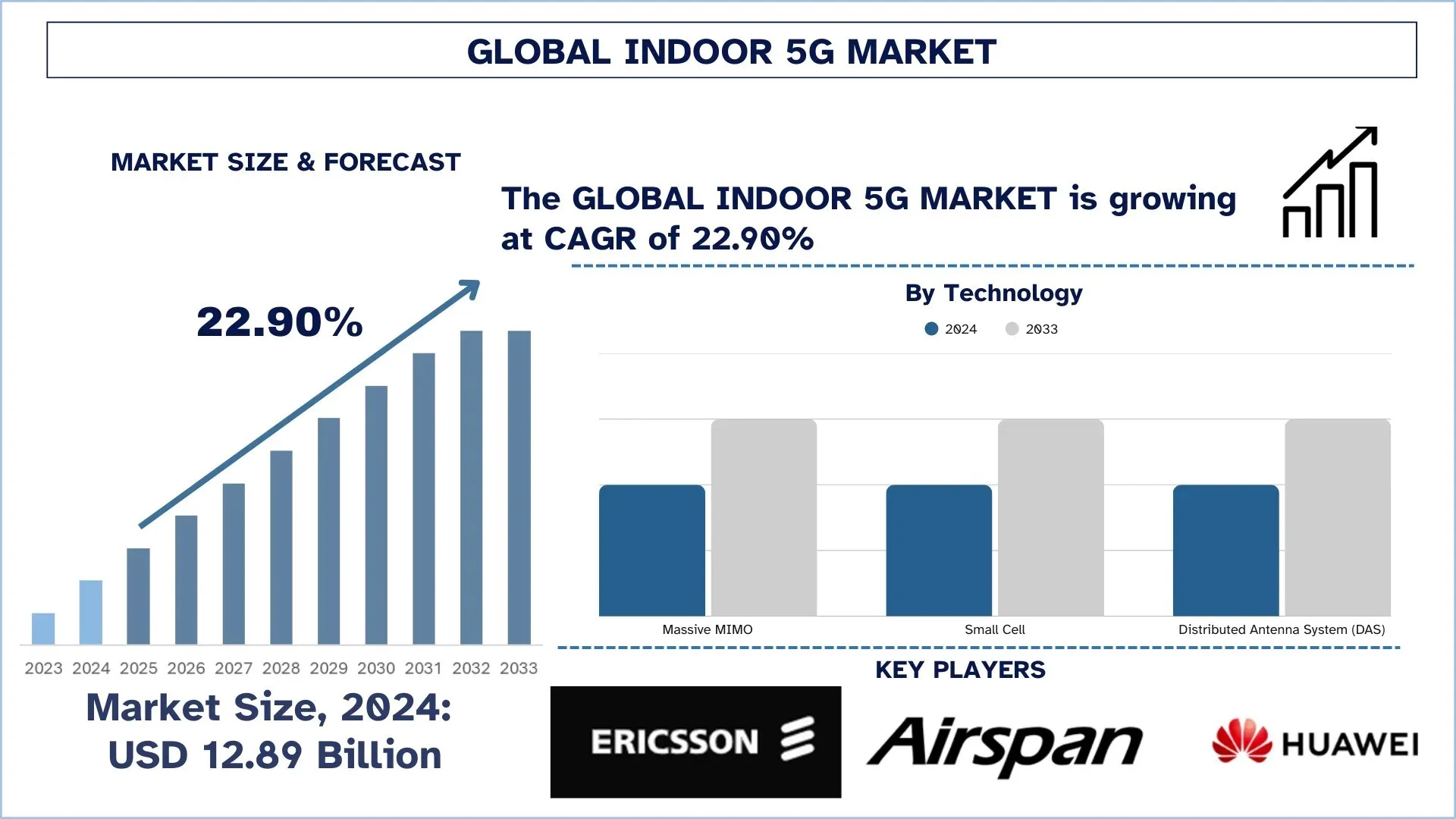

The Global Indoor 5G Market was valued at USD 12.89 billion in 2024 and is expected to grow at a robust CAGR of around 22.90% during the forecast period (2025-2033F), owing to the increasing demand for high-speed connectivity, the rise of smart buildings and IOT, and the growing enterprise digital transformation.

Indoor 5G Market Analysis

5G is a breakthrough in telecommunications, enabling the next wave of hyper-connectivity across sectors. Indoor 5G has evolved into being a critical cog in the wheels of becoming a digital world as it has ultra-low latency, high data throughput, and seamless connectivity capabilities, with an important role for enterprise IT, healthcare, education, retail, and manufacturing. With 5G, the real effects become most relevant indoors, where legacy systems and Wi-Fi cannot assist. Most of the features offer low latency and network slicing, plus high device density support for carrying load-critical, rare applications and advanced user applications.

5G has already transformed enterprise connections, smart buildings, and immersive digital experiences across corporate campuses, smart factories, airports, and stadiums. These environments require continuous, fast, and high-definition connectivity to support innovations, including software applications involving AR, robotics, remote operations, and real-time analytics. On the backdrop of uninterrupted streaming, safe communication, and infrastructure connectivity, the advent of 5G promises to unlock operational excellence and user satisfaction. The rapid demand has been even further fostered by the adoption of Industry 4.0 initiatives, the need for hybrid work support, and the evolution in the architecture of private networks.

Global Indoor 5G Market Trends

This section discusses the key market trends that are influencing the various segments of the global indoor 5G market, as found by our team of research experts.

Adoption of Private 5G Network Deployments

Among the major trends in the indoor 5G market, the deployment of private 5G networks is the most prominent one. Private 5G networks create new approaches for enterprise organizations to handle their indoor connectivity requirements. 5G networks managed by organizations enable complete control of network parameters, so businesses select them for secure environments like factories and logistics terminals, and hospitals. Nokia and Bosch announced in February 2023 that they created 5G-based precision positioning technology which serves new industrial use cases during Industry 4.0. Extensive testing as part of the proof-of-concept deployment at a Bosch production facility in Germany reached 50 cm accuracy in 90 percent of the factory area. The networks maintain specialized data allocation for vital operations while bypassing reliance on external telecommunications providers. The expanding spectrum options, including CBRS as an example of U.S. unlicensed resources, now permit medium-sized organizations to build economical private networks. The technology companies Ericsson and Nokia provide "5 G-as-a-Service" packages, incorporating infrastructure together with software and support services for indoor deployments. The trend demonstrates a fundamental transformation toward adaptable and secure, and personalized indoor network systems that redefine modern enterprise digital structure.

Indoor 5G Industry Segmentation

This section provides an analysis of the key trends in each segment of the global indoor 5G market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Small Cell Market Dominates the Indoor 5G Market

Based on technology, the indoor 5G market is segmented into Massive MIMO, Small Cell, and Distributed Antenna System (DAS). In 2024, the small cell market dominated the market and is expected to maintain its leading position throughout the forecast period. This is due to the gradual worldwide thrust toward attaining seamless, high-speed, and low-latency connectivity in confined or heavily populated indoor spaces, typically relying on conventional macro networks for reasonably consistent performance. Small cells have a good, aesthetically appealing form factor whereby they can be easily deployed across a variety of indoor spaces, ranging from offices, malls, hospitals, and industrial plants to other areas tailored toward improving indoor 5G coverage and capacity. The adoption of private networks and edge computing environments is further adding to the growth of small-cell technology, enabling enterprises to gain extra control, security, and network slicing capabilities for use cases such as autonomous robotics, smart surveillance, and remote diagnostics. They open mid-band and mmWave spectrums, supporting the deployment of small cells and reforming licensing frameworks to fast-track rollouts across regions.

The Below 6 GHz Segment Dominates the Indoor 5G Market.

Based on frequency band, the indoor 5G market is bifurcated into below 6 GHz and mmWave. The below 6 GHz segment held the largest market share in 2024. The unique propagation characteristics offered in this spectrum make it suitable and economical for integrating with existing infrastructure for mass indoor deployment. Below the 6 GHz band, notably in the sub-3.5 GHz band, represents a compromise in speed, coverage, and penetration of signals for them to travel through walls and other indoor obstacles, which is a significant requirement in environments such as office buildings, hospitals, malls, and educational institutions. As corporations increasingly demand reliable and widely covering indoor networks for mission-critical applications and hybrid work environments, IoT device ecosystems find that sub-6 GHz is the air band that offers the right balance of performance versus deployment feasibility. In contrast to mmWave, which gives terrific speed but poor coverage and penetration, below 6 GHz solutions keep connectivity over a larger land space by deploying a smaller number of small cells, thereby reducing capital and operational expenditure. More recent advancements, such as DSS and carrier aggregation, have enabled operators to deploy 5G services over existing LTE networks with minimal disruption, further enhancing the attractiveness of below 6 GHz frequency bands. With growing requirements for indoor 5G sub-6GHz systems, smart building projects, and digital transformation projects across developed and emerging markets, such approaches will increasingly become essential for indoor connectivity, delivering networks of high-performance, energy-efficient, and economically scalable solutions servicing a wide range of applications.

Asia Pacific Dominated the Global Indoor 5G Market

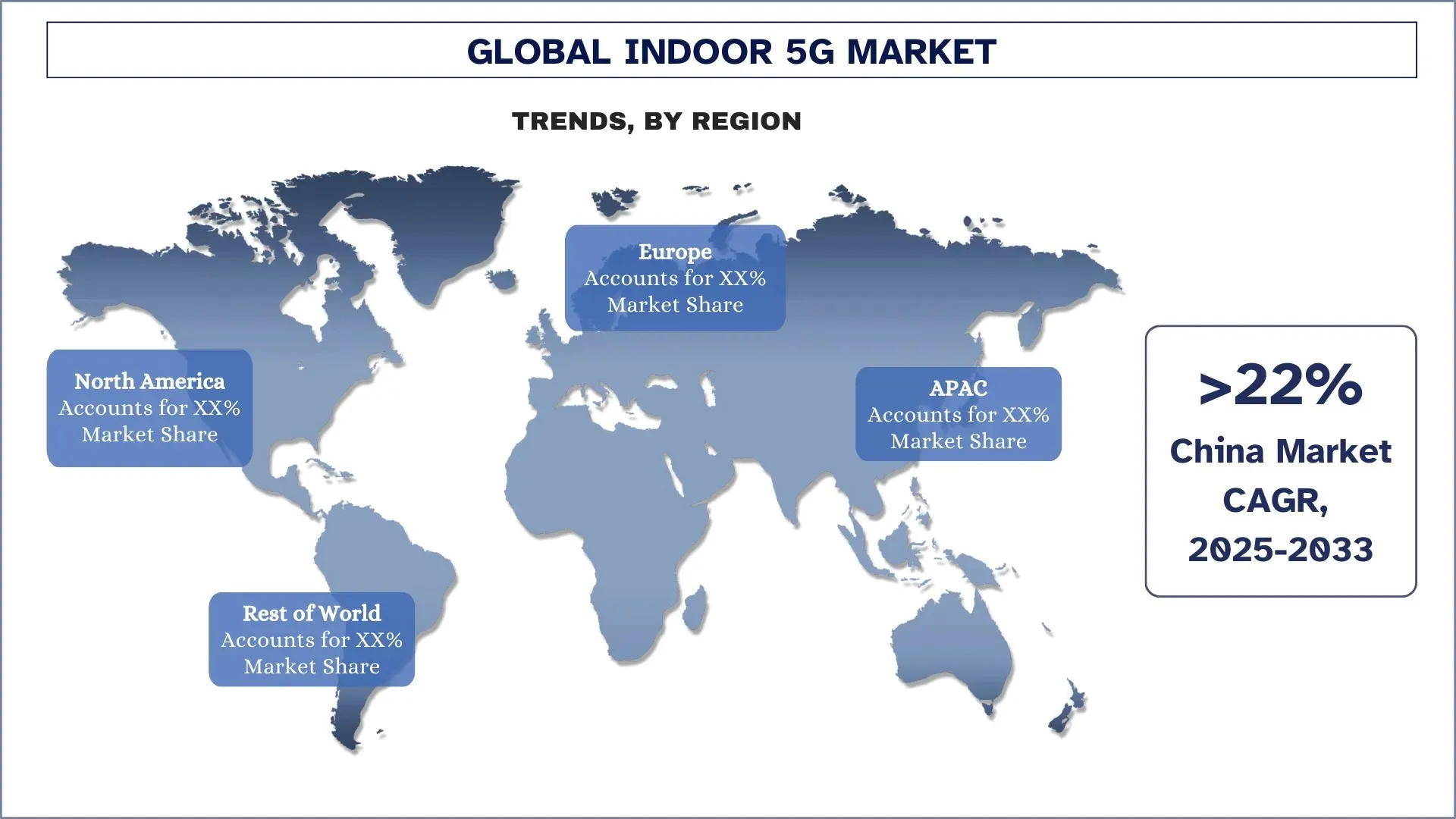

The Asia Pacific indoor 5G market dominated the global indoor 5G market in 2024 and is forecasted to remain in this position in the forecast period. The region's growth is fueled by the rapidly changing pace of urbanization, fast-growing digital development, and government initiatives pushing for next-generation connectivity. China, Japan, and South Korea are at the forefront of the indoor 5G research, deployment, and commercialization, mainly in applications such as enterprise, healthcare, and public venues. The presence of major telecoms and tech companies such as Huawei, ZTE, Samsung, and NTT Docomo, who have been actively investing in expanding and customizing indoor 5G networks for smart buildings, factories, and transportation hubs. Additionally, a strong imposition of smart city and digital transformation policies across the Asia-Pacific region thus became relevant in encouraging the setting up of private 5G networks in office complexes, manufacturing zones, educational campuses, and hospitals, contributing hugely towards Asia Pacific's prominence. For example, the 14th Five-Year Plan of China indicates massive investments into 5G infrastructure, highlighting indoor connectivity in urban innovation clusters as an important area. Conversely, South Korea is rapidly rolling out smart hospitals and automated logistics hubs powered by 5G under the government's Digital New Deal initiative. The region also boosted the fast-evolving digital economy and high mobile penetration to complement the need for high-speed, uninterrupted connectivity in private and public spaces.

China held a dominant Share of the Asia Pacific Indoor 5G Market in 2024

China's ambitious national digital infrastructure agenda and continuing vigorous urbanization, and a well-established manufacturing ecosystem were considerably impressive in 2024. The government was very quick to bring about the implementation of 5G to various smart buildings, industrial parks, hospitals, and transport hubs under its well-known "New Infrastructure" initiatives, among all other things. Telecom giants like China Mobile, Huawei, and China Telecom have invested heavily in the provision of indoor 5G solutions like small cells and private networks. From the telecommunications equipment and semiconductors to IoT devices, the vertically integrated supply chain in China permitted faster, cheaper rollouts. Besides, its emphasis on self-dependence on core technologies and huge R&D investments in 5G applications has, in fact, given China the edge in technology.

Indoor 5G Competitive Landscape

The global Indoor 5G market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top Indoor 5G Companies

Some of the major players in the market are Telefonaktiebolaget LM Ericsson, Airspan, Huawei Technologies Co., Ltd., Nokia, SOLiD, Samsung, Proptivity, LitePoint, A Teradyne Company, ALCAN Systems GmbH i.L., and ZTE.

Recent Developments in the Indoor 5G Market

In April 2024, Nokia and Bharti Airtel continue to expand their partnership to improve 4G and 5G capabilities of Airtel's network operations in India. Nokia installs its Packet Core and Fixed Wireless Access solutions to integrate 5G and 4G systems, which bring enhanced capacity for home broadband and enterprise services. The collaboration will enhance both network quality and operational cost savings through automation systems and Generative Artificial Intelligence while assisting Airtel to execute its 5G standalone architectural transition.

In September 2024, Huawei's partnership with du from The Emirates Integrated Telecommunications Company (EITC) launched the first successful Middle East deployment of Huawei’s 5G LampSite X ‘Digital Indoor Solution’ through Three Carrier Aggregation (3CC) Technology. The success helps du consolidate its 5G user experience market leadership with the ability to deliver 5.1 Gbps peak data rates.

In April 2025, Airspan Networks Holdings LLC completed its acquisition of Corning Incorporated’s wireless business. The deal gives Airspan full ownership of Corning’s 6000 and 6200 distributed antenna systems (DAS) and SpiderCloud 4G and 5G small cell RAN portfolio. The acquisition enables Airspan to advance its presence in indoor connectivity through an expanded collection of wireless solutions.

Global Indoor 5G Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 22.90% |

Market size 2024 | USD 12.89 Billion |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | Asia Pacific is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, South Korea, and India |

Companies profiled | Telefonaktiebolaget LM Ericsson, Airspan, Huawei Technologies Co., Ltd., Nokia, SOLiD, Samsung, Proptivity, LitePoint, A Teradyne Company, ALCAN Systems GmbH i.L., and ZTE |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Technology, By Frequency Band, By End-User, and By Region/Country |

Reasons to Buy the Indoor 5G Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional level analysis of the industry.

Customization Options:

The global indoor 5G market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global Indoor 5G Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global indoor 5G market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the indoor 5G value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global indoor 5G market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including technology, frequency band, end-user, and regions within the global indoor 5G market.

The Main Objective of the Global Indoor 5G Market Study

The study identifies current and future trends in the global indoor 5G market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current market size and forecast the market size of the global indoor 5G market and its segments in terms of value (USD).

Indoor 5G Market Segmentation: Segments in the study include areas of technology, frequency band, end-user, and regions.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the indoor 5G industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the indoor 5G market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global indoor 5G market current market size and its growth potential?

The global indoor 5G market was valued at USD 12.89 billion in 2024 and is expected to grow at a CAGR of 22.90% during the forecast period (2025-2033).

Q2: Which segment has the largest share of the global indoor 5G market by technology?

The small cell category dominated the market and is expected to maintain its leading position throughout the forecast period. This is due to the gradual worldwide thrust toward attaining seamless, high-speed, and low-latency connectivity in confined or heavily populated indoor spaces, typically relying on conventional macro networks for reasonably consistent performance.

Q3: What are the driving factors for the growth of the global indoor 5G market?

Increasing Demand for High-Speed Connectivity: Enterprises and consumers require ultra-low latency and high bandwidth for applications like AR/VR, cloud gaming, and 4K streaming.

Rise of Smart Buildings & IoT: Smart offices, factories, and homes rely on seamless indoor 5G for automation, asset tracking, and real-time monitoring.

Enterprise Digital Transformation: Industries like manufacturing, healthcare, and logistics are adopting private 5G networks for automation, remote monitoring, and AR/VR applications.

Q4: What are the emerging technologies and trends in the global indoor 5G market?

Private 5G Network Deployments: Businesses are increasingly deploying localized indoor 5G networks for secure and high-performance connectivity.

Neutral Host and Shared Infrastructure Models: Cost-sharing models are gaining traction to make deployments more economically viable.

AI-Driven Network Optimization: AI is being used for predictive maintenance, traffic optimization, and quality assurance in indoor 5G environments.

Q5: What are the key challenges in the global indoor 5G market?

High Deployment Costs: Indoor 5G requires small cells, DAS (Distributed Antenna Systems), and fiber backhaul, making it capital-intensive.

Complex Site Acquisition & Integration: Retrofitting 5G into existing buildings can be logistically difficult due to physical and regulatory constraints.

Lack of ROI for Smaller Venues: Smaller enterprises and venues may find it difficult to justify the cost without clear monetization models.

Q6: Which region dominates the global indoor 5G market?

The Asia Pacific indoor 5G market dominated the global indoor 5G market in 2024 and is forecasted to remain in this position in the forecast period. The region's growth is fueled by the rapidly changing pace of urbanization, fast-growing digital development, and government initiatives pushing for next-generation connectivity. China, Japan, and South Korea are at the forefront of the indoor 5G research, deployment, and commercialization, mainly in applications such as enterprise, healthcare, and public venues. The presence of major telecoms and tech companies such as Huawei, ZTE, Samsung, and NTT Docomo, who have been actively investing in expanding and customizing indoor 5G networks for smart buildings, factories, and transportation hubs. Additionally, a strong imposition of smart city and digital transformation policies across the Asia-Pacific region thus became relevant in encouraging the setting up of private 5G networks in office complexes, manufacturing zones, educational campuses, and hospitals, contributing hugely towards Asia Pacific's prominence. For example, the 14th Five-Year Plan of China indicates massive investments into 5G infrastructure, highlighting indoor connectivity in urban innovation clusters as an important area. Conversely, South Korea is rapidly rolling out smart hospitals and automated logistics hubs powered by 5G under the government's Digital New Deal initiative. The region also boosted the fast-evolving digital economy and high mobile penetration to complement the need for high-speed, uninterrupted connectivity in private and public spaces.

Q7: Who are the key players in the global indoor 5G market?

Top companies in the global indoor 5G market

• Telefonaktiebolaget LM Ericsson

• Airspan

• Huawei Technologies Co., Ltd.

• Nokia

• SOLiD

• Samsung

• Proptivity

• LitePoint, A Teradyne Company

• ALCAN Systems GmbH i.L.

• ZTE

Q8: How does the development of new technologies impact the competitive landscape in the Indoor 5G market?

• Technology Differentiation: Innovations such as beamforming, MIMO (Multiple Input, Multiple Output) antennas, and AI-driven network optimization allow companies to differentiate their products, offering superior performance and attracting customers.

• Cost Efficiency and Scalability: The adoption of more efficient technologies in 5G infrastructure can lower deployment costs, making it easier for companies to scale their services and reach broader markets.

• Investor Appeal: Companies investing in cutting-edge technologies demonstrate a forward-thinking approach, which boosts investor confidence. The potential for capturing emerging market segments with advanced tech solutions makes such companies attractive investment opportunities.

Q9: How does competition within the Indoor 5G market affect pricing and product offerings?

• Pricing Pressure: The presence of multiple competitors can lead to price reductions, pushing companies to innovate more to justify their pricing models. This can lead to more affordable solutions for customers, but also thinner profit margins for businesses.

• Product Diversification: To differentiate themselves, companies may offer a range of products, from basic 5G infrastructure to premium, high-performance systems, catering to different customer needs and budgets.

• Investor Perspective: Intense competition can lead to market fragmentation, where only the most resilient companies survive. Investors closely monitor this competition, as companies with sustainable competitive advantages will see long-term returns despite pricing pressures.

Related Reports

Customers who bought this item also bought

Indoor 5G Market: Current Analysis and Forecast (2025-2033)

Emphasis on Technology (Massive MIMO, Small Cell, and Distributed Antenna System (DAS)); Frequency Band (Below 6 GHz and mmWave); End-User (Enterprise (Commercial Buildings, Manufacturing Units, etc)), Public Venues (Stadiums, Airports, etc.), Residential Buildings, Healthcare, and Education); and Region/Country

May 19, 2025

Certificate Authority Market: Current Analysis and Forecast (2025-2033)

Emphasis on Component (Certificate Type, SSL Certificates, Code Signing Certificates, Secure Email Certificates, Authentication Certificates, Services); Certificate Validation Type (Domain Validation, Organization Validation, and Extended Validation); Enterprise Size (SMEs and Large Enterprises); Vertical (BFSI, Retail and E-commerce, Government and Defence, Healthcare, IT and Telecom, Travel and Hospitality, Education, and Others); and Region/Country

May 7, 2025

Digital Thread Market: Current Analysis and Forecast (2025-2033)

Emphasis on Technology (Application Lifecycle Management (ALM), Computer-Aided Design (CAD), Computer-Aided Manufacturing (CAM), Edge Computing, Enterprise Resource Planning (ERP), Industrial Communication, Industrial Sensor, SCADA, Service Lifecycle Management (SLM), and Others); Type of Module (Analytics & Visualization, Connectivity & Interoperability, Data Collection, and Data Management & Integration); Type of Deployment (Cloud Based and On-Premises); Application (Customer Support, Design & Engineering, Distribution, Maintenance & Services, and Others); End-Users (Aerospace, Automotive, Chemicals, Consumer Goods, Energy & Power, Food & Beverages, and Others); and Region/Country

May 6, 2025