- Home

- About Us

- Industry

- Services

- Reading

- Contact Us

Quantum Dots Market: Current Analysis and Forecast (2025-2033)

Emphasis on Material (Cadmium-based and Cadmium-free); Product Type (Display and Others (Lasers, Solar Cells, and others); End-User (Consumer, Healthcare, Defense, Media and Entertainment, and Others (Agriculture, Energy and Utilities, and others)); and Region/Country

Global Quantum Dots Market Size & Forecast

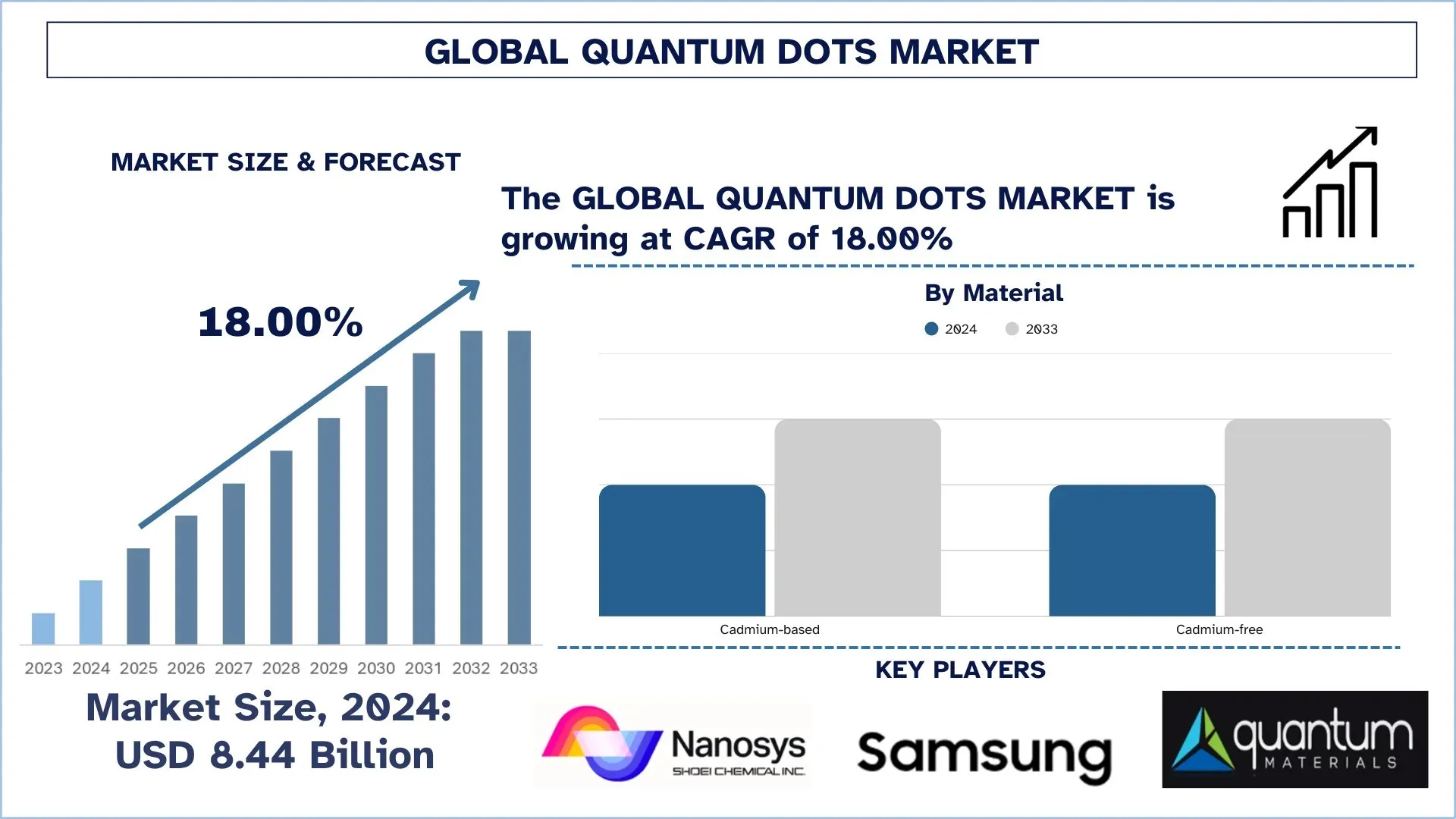

The Global Quantum Dots Market was valued at USD 8.44 billion in 2024 and is expected to grow at a robust CAGR of around 18.00% during the forecast period (2025-2033F), owing to the continuous progress in nanotechnology and material science, enhancing the performance and stability of quantum dots, expanding their application range. Additionally, the increasing consumer preference for high-resolution displays in televisions, smartphones, and monitors is propelling the adoption of quantum dot technology.

Quantum Dots Market Analysis

Quantum dots have grown up into path-breaking technology in the entire nanomaterials field, playing an enabling role for the new era of very high-performing electronics, imaging, and energy applications. These properties have become imperative for many lifelines of industries-such as consumer electronics, healthcare, energy, and automotive-which, inconsistent with their optical and electronic properties, allow size-tunable emission, high brightness, and incredible stability. Quantum dots have become a revolutionary technology for modern next-generation display systems (like the QLED TVs), which have proved to be much deeper in color saturation, brighter in luminosity, and more energy efficient than any older display technology. In the past couple of years, a lot of demand has been observed for quantum dots due to advances in the nanotechnology fields, amongst others, the growing consumer demand for bright visual experience, as well as their growing utilization in biomedical imaging and diagnostics. Private enterprises and governments have invested huge amounts in research and development to find innovative applications across photovoltaics, quantum computation, and targeted medication delivery. Environmental regulations are promoting the manufacturing of cadmium-free quantum dots and channelizing the manufacturers to devise cleaner and safer formulations.

While quantum dots will have become commonplace in solar cells, LEDs, and biosensors, they will have moved to defining market niches from those of exclusive scientific components to those defining core commercial material. The rapid adoption in emerging regions will also be complemented by technology-driven policies and growing awareness among local nations.

Global Quantum Dots Market Trends

This section discusses the key market trends that are influencing the various segments of the global quantum dots market, as found by our team of research experts.

Shift Toward Cadmium-Free Quantum Dots to Align with Safety and Sustainability Standards

Among the major trends in the whole market of quantum dots, the cadmium-free quantum dots are the prominent ones. Cadmium-based QDs in conventional form are effective in giving the crux of vibrant pure colors. However, cadmium, being a heavy metal, is toxic, and its release into the environment or utilization in consumer products can be hazardous. This toxic nature has prompted a lot of regulations against cadmium use, such as the Restriction of Hazardous Substances (RoHS) directive under the European Union and the REACH regulations. In these conditions, manufacturers and research institutions have incorporated a phased approach in developing non-poisonous alternatives. The cadmium-free QDs, largely made from indium phosphide (InP) or other less toxic materials, are now coming into play across many industries but are predominantly at the forefront in consumer electronics applications, where environmental branding and compliance with existing regulations quite a lot of focus on safety measures. Companies taking part in this market spend most of their investment in display technology and other applications. Such investments are the case for QustomDot, a leading innovator in cadmium-free quantum dot technology for display purposes, which announced the closure of a EUR 2.7 million financing round alongside an EIC accelerator grant for EUR 2.5 million in November 2024. CFQDs are also getting into applications such as biomedical imaging, LED lighting, and solar cells, where safety is never compromised.

Quantum Dots Industry Segmentation

This section provides an analysis of the key trends in each segment of the global quantum dots market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Cadmium-free Market Dominates the Quantum Dots Market

Based on material, the quantum dots market is bifurcated into Cadmium-based and Cadmium-free. In 2024, the cadmium-free market dominated the market and is expected to maintain its leading position throughout the forecast period. This is due to the increased international concerns about environmental safety and compliance with regulations, making the heavy metal used in conventional quantum dots, which include cadmium selenide (CdSe), extremely poisonous to human beings. The European Restriction of Hazardous Substances (RoHS) implemented strict regulations on the use of cadmium in composites and materials for consumer consumption, thus requiring companies to seek safer alternatives. Considering these, cadmium-free quantum dots, which have been demonstrated on InP or carbon and display similar optical performance without such hazards, were developed. Companies such as Samsung, Nanoco Technologies, and Nanosys have replaced the cadmium-based materials in their QLED TVs with InP quantum dots as part of their commitment to going green and reaching a wider market-open approach to environmentally who wanted to be conscious. Furthermore, cadmium-free QDs have gained interest in biomedical applications where the concern for toxicity is crucial in allowing safe in vivo imaging and diagnostics. Following the same sustainability awareness, when consumers started favoring environment-friendly products, cadmium-free quantum dots slipped into the profile of favored options, combining high performance with compliance and safety.

The Display Segment Dominates the Quantum Dots Market.

Based on product type, the quantum dots market is segmented into Display and Other (Lasers, Solar Cells, and others). The display segment held the largest market share in 2024. The high-quality and energy-efficient display solutions are the need of the hour in most consumer electronics, and this is causing this leadership to emerge. Quantum dots in displays are used to improve color accuracy, brightness, and energy efficiency in televisions, monitors, and smartphones. For example, QD technology has been integrated into display panels by Samsung and LG for higher levels of experience. The fact that new advances in production, such as photo-patternable quantum dot inks for new display applications, including virtual and augmented reality, by NanoPattern Technologies, have also brought to the attention of application-oriented industries the adoption of QDs in displays. For instance, in October 2024, Samsung Display announced the successful development of Quantum Dot ink recycling technology for enhanced cost competitiveness of its QD-OLED displays. In line with that, the company had been able to collect and recycle QD ink wasted during the manufacturing process of the QD-OLED and successfully recovered and reprocessed 80% of the ink that had been wasted in the production of the QD emissive layer. This is expected to yield annual cost savings of approximately USD 7.3 million.

Asia Pacific Dominated the Global Quantum Dots Market

The Asia Pacific quantum dots market dominated the global quantum dots market in 2024 and is forecasted to remain in this position on account of rapid industrialization, a booming consumer electronics industry, and active government assistance toward the evolution of advanced technologies. Countries such as China, South Korea, and Japan are emerging as very fundamental in quantum dot research, manufacturing, and integration, particularly in the display and healthcare sectors. Regional supremacy finds further strength from major electronics manufacturers, such as Samsung, LG, and BOE Technology, investing significantly in quantum dot-enabled displays, including QLED TVs and ultra-high-definition monitors. For example, in April 2024, Samsung Display, in collaboration with distinguished brands for broadcast monitors, SmallHD and Flanders Scientific Inc. (FSI), launched its new QD-OLED reference monitors used for film and broadcast productions to check the quality of footage or calibrate color tones and images to correspond to content concepts. Also, besides government funding, some of the companies in the Asia Pacific region are making some advances in the quantum dots arena. In a similar context, Taiwanese company Winbond Electronics launched in October 2023 a new range of quantum dot-enhanced devices aimed mainly at upgrading display technologies. In addition to the very fast-growing consumer electronics market of the region, a greater demand for high-definition screens is being witnessed. These supporting factors by legislation, along with innovative breakthroughs by major players of the Quantum Dots Market in Asia Pacific, indicate a bright future, further solidifying its place as a worldwide powerhouse for this new technology.

China held a dominant Share of the Asia Pacific Quantum Dots Market in 2024

The visionary developments in the realm of quantum dots (QD), which unfold in China, are spearheaded by its vertically integrated manufacturing capabilities, fast consumer electronics growth, and investments offered by the state for research in nanotechnology. In addition, the growing attention of the nation to self-reliance in semiconductors and display technology superiority, especially in OLED and QLED panels, has pushed it far ahead of most of the global markets regarding production and innovation. With companies like TCL and BOE Technology integrating these quantum dots into their televisions and displays, it has placed China as one of the largest consumer and producer bases in the world for products enabled by QDs. Further, the continuous state investments in research parks, smart factories, and next-generation materials have also opened the door for innovation into cadmium-free QDs so that they may also be able to meet international restrictions for export as well as domestic sustainability.

Quantum Dots Competitive Landscape

The global Quantum Dots market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top Quantum Dots Companies

Some of the major players in the market are Shoei Electronic Materials, Inc., SAMSUNG, Quantum Materials Corporation, UbiQD, Nanoco Group plc, NNCrystal US Corporation, Ocean NanoTech LLC, QDI Systems, Thermo Fisher Scientific Inc., and ams-OSRAM AG.

Recent Developments in the Quantum Dots Market

In August 2023, UbiQD, Inc. signed a joint development agreement with First Solar, Inc., to jointly explore the possibility of integrating fluorescent quantum dot technology into next-generation solar modules.

In January 2024, Quantum Solutions announced the release of QDot Perovskite CsPbBr3 Single Crystals for X-ray sensors. The product was released in collaboration with AY Sensors. This material is a significant alternative to CdTe and CdZnTe (CZT) crystals used in direct X-ray sensors. CsPbBr3 single crystals are regarded as the most favorable perovskite composition for X-ray sensors in terms of performance and long-term stability.

In May 2024, VueReal launched its QuantumVue Display technology, which combines its proprietary MicroSolid Printing platform with dynamic quantum dot (QD) patterning.

In February 2024, Diraq, specializing in the quantum computing market, secured over USD 15 million in a Series A-2 funding round. With this, the company expects to bolster its efforts in developing fault-tolerant quantum computing with silicon quantum dots.

Global Quantum Dots Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 18.00% |

Market size 2024 | USD 8.44 Billion |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | Asia Pacific is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, South Korea, and India |

Companies profiled | Shoei Electronic Materials, Inc., SAMSUNG, Quantum Materials Corporation, UbiQD, Nanoco Group plc, NNCrystal US Corporation, Ocean NanoTech LLC, QDI Systems, Thermo Fisher Scientific Inc., and ams-OSRAM AG |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Material, By Product Type, By End-User, and By Region/Country |

Reasons to Buy the Quantum Dots Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional level analysis of the industry.

Customization Options:

The global quantum dots market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global Quantum Dots Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global quantum dots market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the quantum dots value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global quantum dots market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including material, product type, end-user, and regions within the global quantum dots market.

The Main Objective of the Global Quantum Dots Market Study

The study identifies current and future trends in the global quantum dots market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current market size and forecast the market size of the global quantum dots market and its segments in terms of value (USD).

Quantum Dots Market Segmentation: Segments in the study include areas of material, product type, end-user, and regions.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the quantum dots industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the quantum dots market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global quantum dots market current market size and its growth potential?

The global quantum dots market was valued at USD 8.44 billion in 2024 and is expected to grow at a CAGR of 18.00% during the forecast period (2025-2033).

Q2: Which segment has the largest share of the global quantum dots market by material?

The cadmium-free market dominated the market and is expected to maintain its leading position throughout the forecast period. This is due to the increased international concerns about environmental safety and compliance with regulations, making the heavy metal used in conventional quantum dots, which include cadmium selenide (CdSe), extremely poisonous to human beings.

Q3: What are the driving factors for the growth of the global quantum dots market?

Advancements in Nanotechnology: Continuous progress in nanotechnology and material science is enhancing the performance and stability of quantum dots, expanding their application range.

Rising Demand for High-Resolution Displays: The increasing consumer preference for high-resolution displays in televisions, smartphones, and monitors is propelling the adoption of quantum dot technology.

Growing Investments in Research and Development: Significant investments by both private and public sectors are accelerating innovation and the commercialization of quantum dot applications.

Q4: What are the emerging technologies and trends in the global quantum dots market?

Shift Towards Cadmium-Free Quantum Dots: There's a growing preference for cadmium-free quantum dots, driven by environmental regulations and consumer demand for safer products.

Integration in Solar Energy Applications: Quantum dots are being explored to enhance the efficiency of solar cells, with research demonstrating improved energy conversion rates.

Advancements in Quantum Dot Printing Technologies: Developments in printing techniques are enabling cost-effective and scalable production of quantum dots, broadening their application scope.

Q5: What are the key challenges in the global quantum dots market?

High Production Costs: The complex manufacturing processes and the need for specialized equipment contribute to the high costs of quantum dot production.

Regulatory Hurdles: Certain quantum dots, especially those containing cadmium, raise environmental and health concerns, leading to regulatory challenges.

Competition from Alternative Technologies: Technologies like OLEDs and microLEDs offer similar benefits to quantum dots, posing competition in display and lighting applications.

Q6: Which region dominates the global quantum dots market?

The Asia Pacific quantum dots market dominated the global quantum dots market in 2024 and is forecasted to remain in this position on account of rapid industrialization, a booming consumer electronics industry, and active government assistance toward the evolution of advanced technologies. Countries such as China, South Korea, and Japan are emerging as very fundamental in quantum dot research, manufacturing, and integration, particularly in the display and healthcare sectors.

Q7: Who are the key players in the global quantum dots market?

Some of the leading companies in quantum dots includes:

• Shoei Electronic Materials, Inc.

• SAMSUNG

• Quantum Materials Corporation

• UbiQD

• Nanoco Group plc

• NNCrystal US Corporation

• Ocean NanoTech LLC

• QDI Systems

• Thermo Fisher Scientific Inc.

• ams-OSRAM AG

Q8: How does intellectual property (IP) and patent ownership influence competitive advantage and investor confidence in the Quantum Dots industry?

• Barrier to Entry for Competitors: Strong IP portfolios prevent new entrants from easily replicating technology, ensuring long-term market dominance for key players.

• Licensing Revenue Streams: Companies with patented Quantum Dot technologies can generate additional revenue by licensing their IP to other firms, boosting profitability.

• Investor Assurance: A robust patent portfolio signals innovation leadership and reduces litigation risks, making the company a safer investment.

Q9: What roles do government regulations and environmental policies play in shaping the growth and sustainability of Quantum Dot businesses?

• Compliance Costs vs. Market Access: Strict regulations (e.g., RoHS, REACH) may increase production costs but ensure market access in regions like the EU and North America.

• Demand for Eco-Friendly Solutions: Growing emphasis on non-toxic (cadmium-free) Quantum Dots creates opportunities for compliant companies to capture premium markets.

• Investor Risk Assessment: Regulatory alignment reduces long-term risks, making compliant firms more attractive to ESG-focused investors.

Related Reports

Customers who bought this item also bought

Ion Beam Etching System Market: Current Analysis and Forecast (2026-2034)

Emphasis on Type (Conventional Ion Beam Etching (IBE), Reactive Ion Beam Etching (RIBE), Focused Ion Beam (FIB) Systems, Automatic Ion Beam, and Others); Application (Semiconductor Manufacturing, Microelectronics & Data Storage, Photonics & Optoelectronics, MEMS (Micro-Electro-Mechanical Systems), Research & Metrology, and Others); End User (Semiconductor & Electronics, Aerospace & Defense, Healthcare & Medical Devices, Research Institutions, and Others); and Region/Country

April 30, 2026

Power over Ethernet (PoE) Chipset Market: Current Analysis and Forecast (2025-2033)

Emphasis on Type (PoE Power Sourcing Equipment (PSE) Chipset and PoE Powered Devices (PD) Chipset); Standard (IEEE 802.3at Standard, IEEE 802.3bt Standard, and IEEE 802.3af Standard); Device (IP/Network Cameras, VoIP Phone, Ethernet Switch & Injector, Wireless Radio Access Point, Proximity Sensor, LED Lighting, and Others); End-use (Commercial, Industrial, and Residential); and Region/Country

April 17, 2026