- Home

- About Us

- Industry

- Services

- Reading

- Contact Us

Glass Interposers Market: Current Analysis and Forecast (2025-2033)

Emphasis on Wafer Size (200 mm, 300 mm, and Above 300 mm); Packaging (2.5D Packaging, 3D Packaging, and Panel-Level Packaging); End-Use Industry (Consumer Electronics, Telecommunications, Automotive, Defense & Aerospace, and Others); and Region/Country

Global Glass Interposers Market Size & Forecast

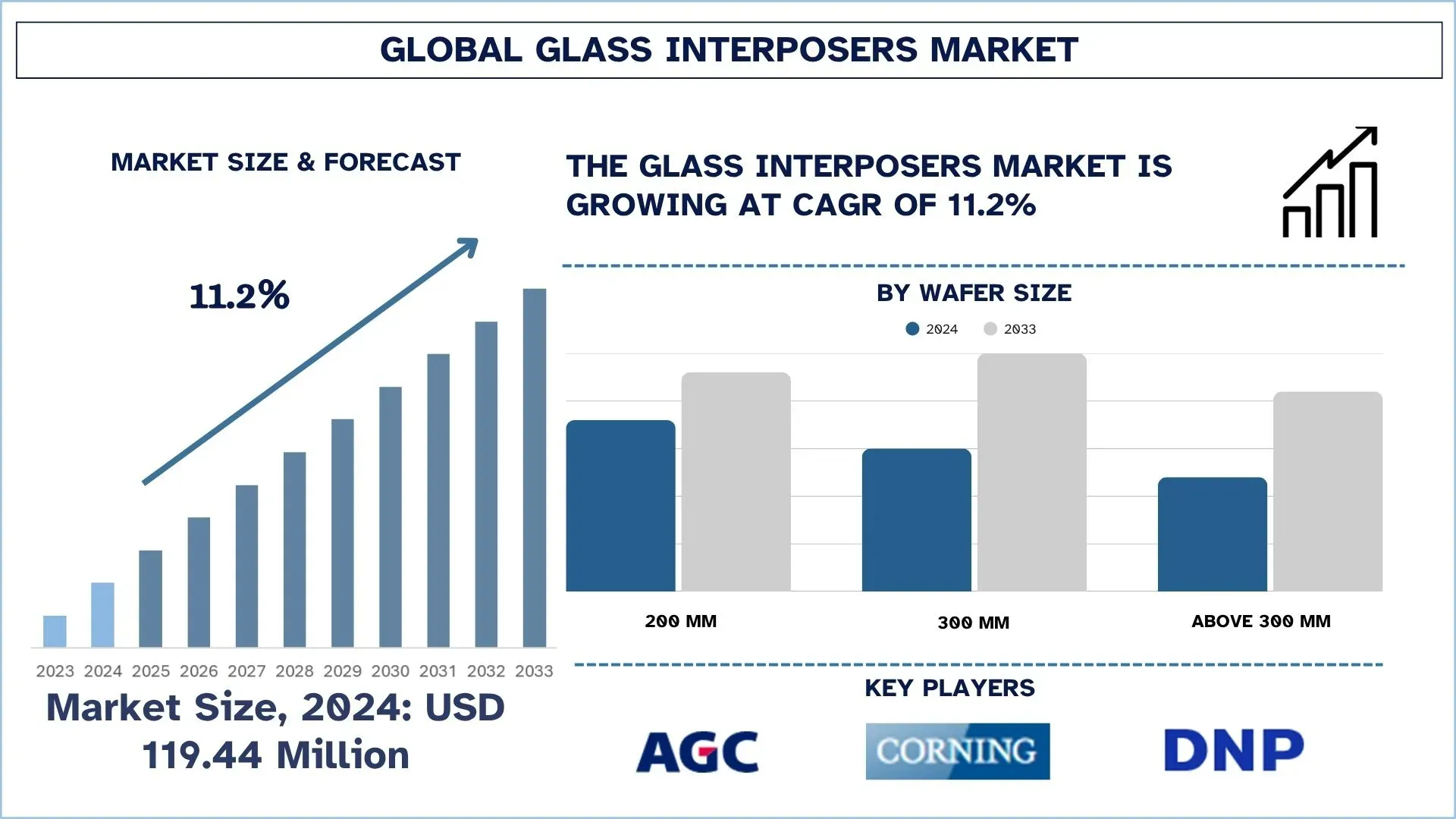

The Global Glass Interposers Market was valued at USD 119.44 million in 2024 and is expected to grow at a strong CAGR of around 11.2% during the forecast period (2025-2033F), driven by the rising demand for advanced semiconductor packaging to support high-performance computing, 5G, and AI applications.

Glass Interposers Market Analysis

A glass interposer is a vital component used in the microelectronics sector, serving as a bridging platform between the silicon chip and the substrate or printed circuit board (PCB) to which the chip is mounted. Glass interposer offers several features, such as higher performance due to their superior electrical properties and enhanced thermal management capabilities compared to traditional organic substrates.

The glass interposers market is experiencing significant growth due to the rising demand for high-performance, energy-efficient, and miniaturized semiconductor devices. High-performance computing (HPC), artificial intelligence (AI), and 5G communications, as well as other advanced applications, require high interconnect density, minimal signal loss, and excellent thermal management capabilities, which only glass interposers can provide compared to traditional organic substrates.

Global Glass Interposers Market Trends

This section discusses the key market trends that are influencing the various segments of the global glass interposers market, as found by our team of research experts.

Rising Adoption of 2.5D and 3D Packaging Technologies for Next-Generation Semiconductors

The adoption of 2.5D and 3D packaging technology in next-generation semiconductors is another major trend in the glass interposers market. With the growing need for high-performance computing, AI, 5G, and IoT devices, conventional packaging technologies are becoming limited in their ability to miniaturize, fast, and power efficient. Glass interposers, being more electrically insulated, less signal-loss, and more dimensionally stable, are being used more frequently to allow more advanced heterogeneous integration in 2.5D/3D architectures. This enables stacking or connecting various chips or other elements with improved performance, driving use in data centers, consumer electronics, and automotive applications.

Glass Interposers Industry Segmentation

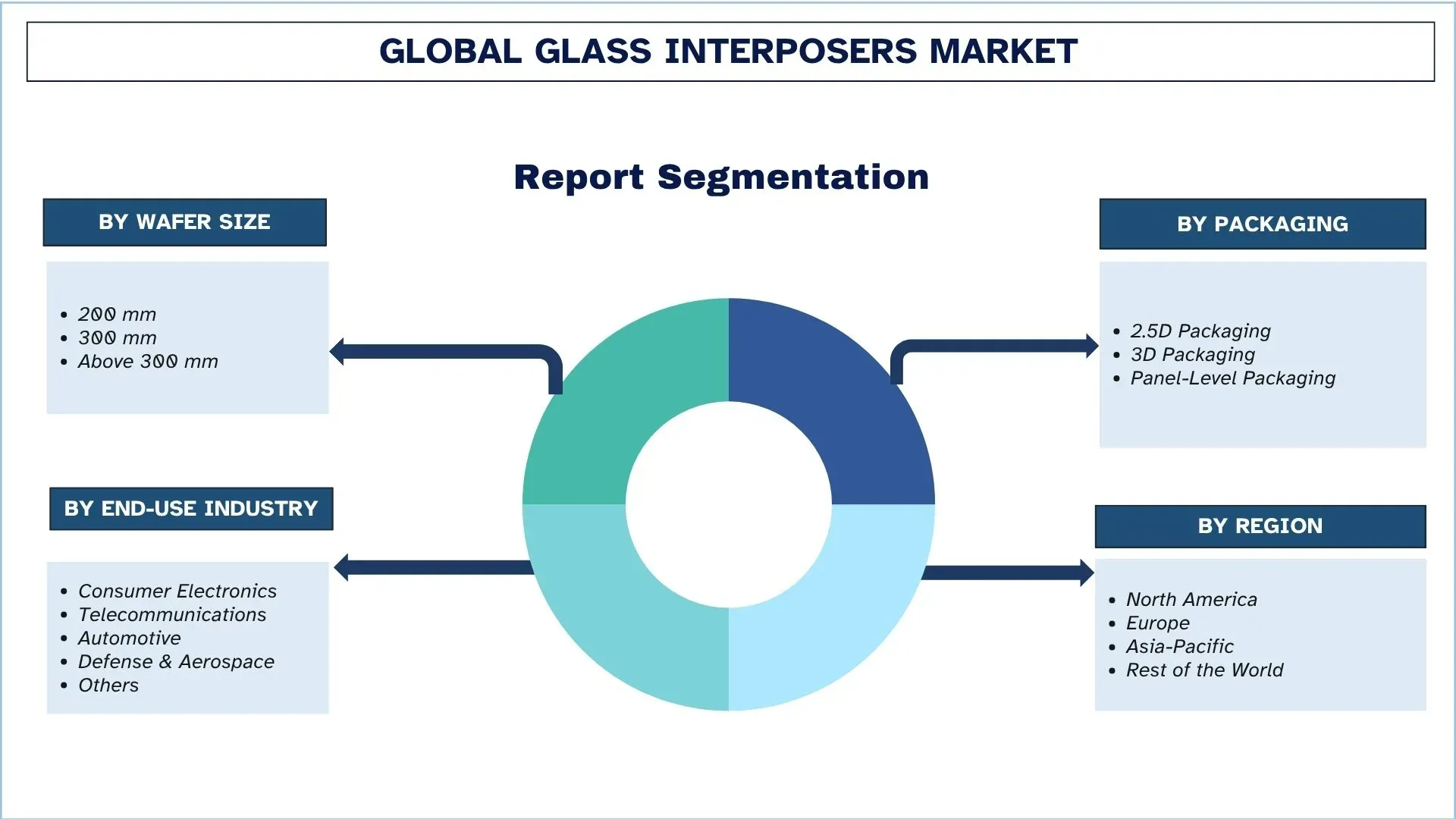

This section provides an analysis of the key trends in each segment of the global glass interposers market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The 300 mm wafer size Segment Dominates the Global Glass Interposers Market

Based on the wafer size category, the market is categorised into 200 mm, 300 mm, and above 300 mm. Among these, the 300 mm wafer segment holds the maximum market share since it provides better yield per wafer, cost-effectiveness, and is commonly used in semiconductor fabrication in various applications such as memory, logic, and advanced processors. However, the above 300 mm wafer segment is projected to experience robust growth in the future as the industry leaders focus on next-generation fabrication technology to satisfy the demand of AI, IoT, and 5G-enabled devices, which is likely to decrease the cost per chip and boost productivity.

The Consumer Electronics Segment Dominates the Global Glass Interposers Market.

Based on the end-use industry category, the market is segmented into consumer electronics, telecommunications, automotive, defense & aerospace, and others. Among these, consumer electronics currently hold the maximum market share due to the enormous demand for smartphones, laptops, wearables, and other smart devices that need sophisticated semiconductor solutions to process, store, and communicate. However, the automotive industry is predicted to be the most rapidly expanding field in the future due to the increase in the implementation of electric cars, the development of autonomous driving systems, and high-tech driver-assistance systems (ADAS). The rise in semiconductor per vehicle, and government pressure to adopt EVs, will drive automotive industry demand substantially.

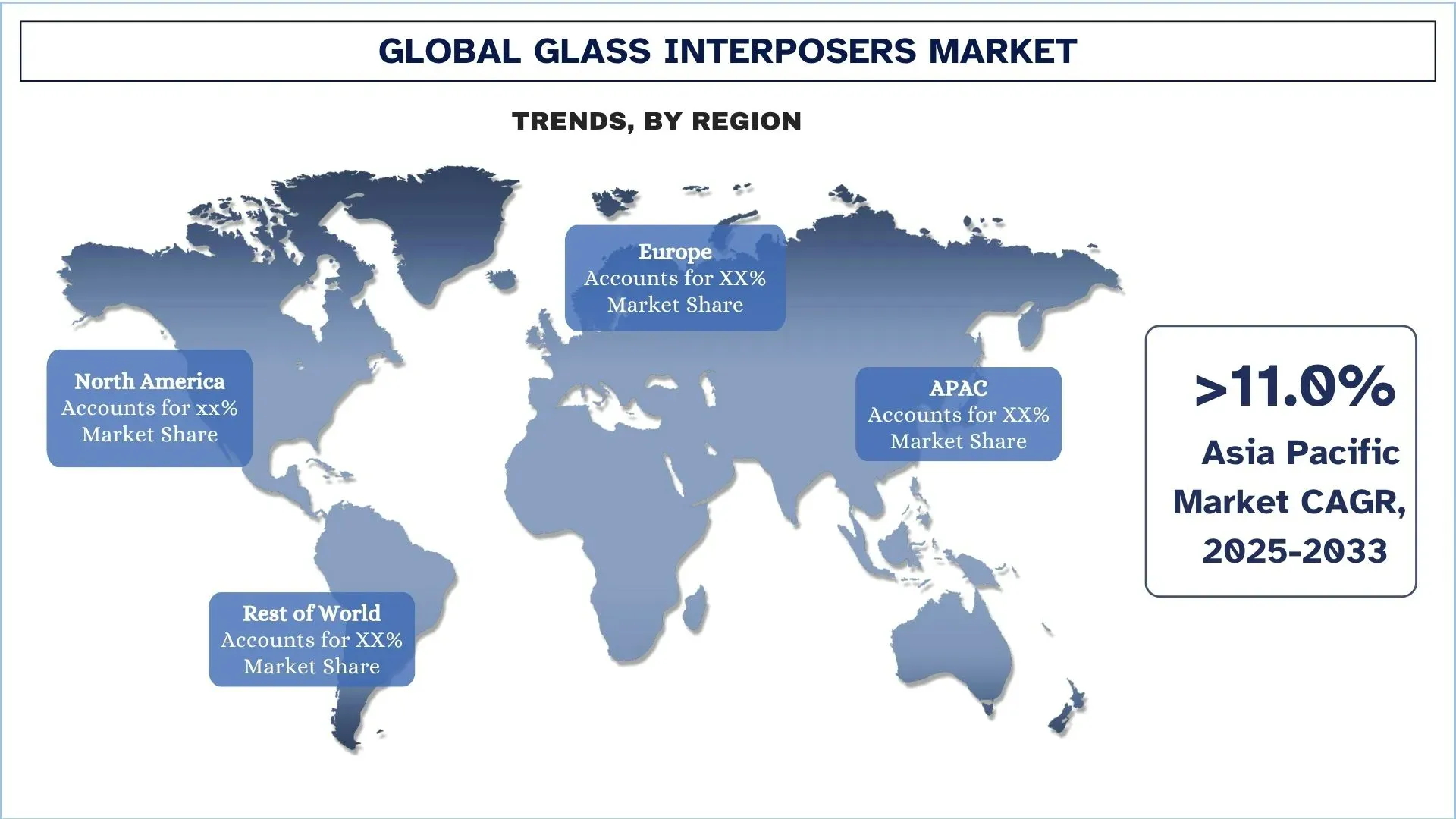

Asia-Pacific holds the largest market share in the global Glass Interposers market

The Asia-Pacific region holds a significant market share of the glass interposers market due to its well-established semiconductor manufacturing ecosystem, led by nations such as China, Taiwan, South Korea, and Japan. The availability of large foundries, OSAT suppliers, and glass substrate suppliers makes large-scale production possible and the adoption of sophisticated solutions in packaging. The high-performance, high-density, and thermally stable interposers are needed as the consumer electronics, data centers, AI applications, and 5G infrastructure grow rapidly. Additionally, the Asian-Pacific region is the most preferred region for glass interposers manufacturing, due to favourable government policies, investments in research and development, and cost-effective manufacturing, which can cater to both the local market and global exports.

China held a Dominant share of the Asia-Pacific Glass Interposers Market in 2024

China has the largest market share in the Asia-Pacific glass interposers market, which can be attributed to its high level of manufacturing of large-scale semiconductors and an extensive electronics ecosystem. The nation is a global consumer electronics, 5G technologies, and AI-based application hub that generates high demand in terms of sophisticated packaging technologies. Additionally, significant investments in semiconductor manufacturing within the country, combined with governmental support through programs such as Made in China 2025, enhance its leadership. Also, China has been able to partner with international foundries, OSAT vendors, and glass substrate suppliers to quickly support 2.5D/3D packaging and through-glass via (TGV) technologies, which has further established it as the biggest market in glass interposers.

Glass Interposers Industry Competitive Landscape

The global glass interposers market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, geographical expansions, and mergers and acquisitions.

Top Glass Interposers Market Companies

Some of the major players in the market are AGC Inc., Corning Incorporated, Dai Nippon Printing Co., Ltd., PLANOPTIK AG, Samtec, Inc., SCHOTT, 3DGS, NSG Group, TOPPAN Inc., and Nippon Electric Glass Co., Ltd.

Recent Developments in the Glass Interposers Market

In April 2023, 3D Glass Solutions (3DGS) closed a USD 30 million Series C funding round, led by Walden Catalyst Ventures along with Intel Capital, Lockheed Martin Ventures, and other investors. The funding was directed toward expanding its U.S. manufacturing capacity and advancing its glass-based integrated passive and substrate products. This milestone highlighted the growing investor confidence in glass interposer technology and 3D heterogeneous integration solutions.

In March 2023, Dai Nippon Printing Co. (DNP) developed a new Glass Core Substrate (GCS) employing high-density Through Glass Via (TGV) technology to replace conventional resin substrates in semiconductor packages. The substrate featured a high aspect ratio and fine-pitch wiring, aiming to enhance performance and scalability for next-gen semiconductor integration.

Global Glass Interposers Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 11.2% |

Market size 2024 | USD 119.4 million |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | The North America region is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, and India. |

Companies profiled | AGC Inc., Corning Incorporated, Dai Nippon Printing Co., Ltd., PLANOPTIK AG, Samtec, Inc., SCHOTT, 3DGS, NSG Group, TOPPAN Inc., and Nippon Electric Glass Co., Ltd. |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Wafer Size, By Packaging, By End-Use Industry, and By Region/Country |

Reasons to Buy the Glass Interposers Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional level analysis of the industry.

Customization Options:

The global glass interposers market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global Glass Interposers Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global glass interposers market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the glass interposers value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global glass interposers market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including wafer size, packaging, end-use industry, and regions within the global glass interposers market.

The Main Objective of the Global Glass Interposers Market Study

The study identifies current and future trends in the global glass interposers market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current and forecast market size of the global glass interposers market and its segments in terms of value (USD).

Glass Interposers Market Segmentation: Segments in the study include areas of wafer size, packaging, end-use industry, and region.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the glass interposers industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the glass interposers market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global glass interposers market’s current market size and growth potential?

As of 2024, the global glass interposers market size is USD 119.44 million. The market is projected to grow at a strong CAGR of 11.2% between 2025 and 2033, driven by rising demand across electronics, automotive, and data center applications.

Q2: Which segment has the largest share of the global glass interposers market by wafer size category?

The 300 mm wafer size segment accounts for the largest market share in the global glass interposers industry, owing to its wide adoption in high-performance computing and advanced semiconductor packaging.

Q3: What are the driving factors for the growth of the global glass interposers market?

Top growth drivers of the glass interposers market include:

• Increasing demand for high-performance computing, artificial intelligence (AI), and 5G technology

• Superior properties of glass, such as insulation, signal integrity, and thermal stability, compared to organic substrates

• Rapid integration of glass interposers in consumer electronics, automotive electronics, and data centers

Q4: What are the emerging technologies and trends in the global glass interposers market?

Emerging trends in the glass interposers market include:

• Rising adoption of 2.5D and 3D packaging technologies for next-generation semiconductors

• Growing demand for ultra-thin glass substrates to support miniaturization and improved performance

• Increasing focus on heterogeneous integration in chip design

Q5: What are the key challenges in the global glass interposers market?

Key challenges in the glass interposers market include:

• High manufacturing costs compared to silicon or organic interposers

• Immature supply chain and limited large-scale manufacturing capabilities

• Technical complexity in mass production and yield optimization

Q6: Which region dominates the global glass interposers market?

The Asia-Pacific region dominates the glass interposers market, primarily due to the presence of leading semiconductor manufacturers, strong electronics production hubs, and high adoption of advanced packaging technologies in countries like China, Japan, South Korea, and Taiwan.

Q7: Who are the key competitors in the global glass interposers market?

Top players in the glass interposers industry include:

• AGC Inc.

• Corning Incorporated

• Dai Nippon Printing Co., Ltd.

• PLANOPTIK AG

• Samtec, Inc.

• SCHOTT

• 3DGS

• NSG Group

• TOPPAN Inc.

• Nippon Electric Glass Co., Ltd.

Q8: What are the major investment opportunities in the global glass interposers market?

Investment opportunities lie in areas such as advanced wafer-level packaging, ultra-thin glass substrate development, and integration for AI, IoT, and 5G applications. The market also presents strong potential in automotive electronics and data center infrastructure, where demand for high-performance, miniaturized semiconductor solutions is rapidly rising.

Q9: How can businesses and semiconductor companies benefit from adopting glass interposer technology?

Businesses adopting glass interposers can achieve higher signal integrity, improved thermal performance, and better design flexibility compared to conventional interposers. For semiconductor companies, this translates into enhanced chip performance, cost optimization over time, and competitive advantage in next-generation computing, networking, and consumer electronics markets.

Related Reports

Customers who bought this item also bought

Workplace Safety Alarm Market: Current Analysis and Forecast (2025-2033)

Emphasis on Type (Traditional Alarm Systems, Smart Alarm Systems, and Others); Technology (Environmental Monitoring Systems, Real-Time Location, Wearable Safety Devices, and Others); Application (Construction, Healthcare, Factories & Industrial Plants, Transportation, Offices, Offices, Schools, and Others); and Region/Country

October 9, 2025

Field Programmable Gate Array (FPGA) Market: Current Analysis and Forecast (2025-2033)

Emphasis on Type (Low-end FPGA, Mid-end FPGA, and High-end FPGA); Node Size (<=16nm, 20-90nm, and >90nm); Technology (SRAM-based FPGA, Flash-based FPGA, EEPROM-based FPGA, and Others); Application (Telecommunication, Aerospace & Defense, Data Centre & Computing, Industrial, Healthcare, Consumer Electronics, and Others); and Region/Country

September 4, 2025