- Home

- About Us

- Industry

- Services

- Reading

- Contact Us

Porous Asphalt Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Open-Graded Friction Course, Permeable Asphalt Pavement, Porous Asphalt Concrete, and Others); Additive Type (Polymers, Recycled Materials, Fibers, and Others); Application (Roadways, Parking Lots, Sidewalks, Driveways, and Others); and Region/Country

Global Porous Asphalt Market Size & Forecast

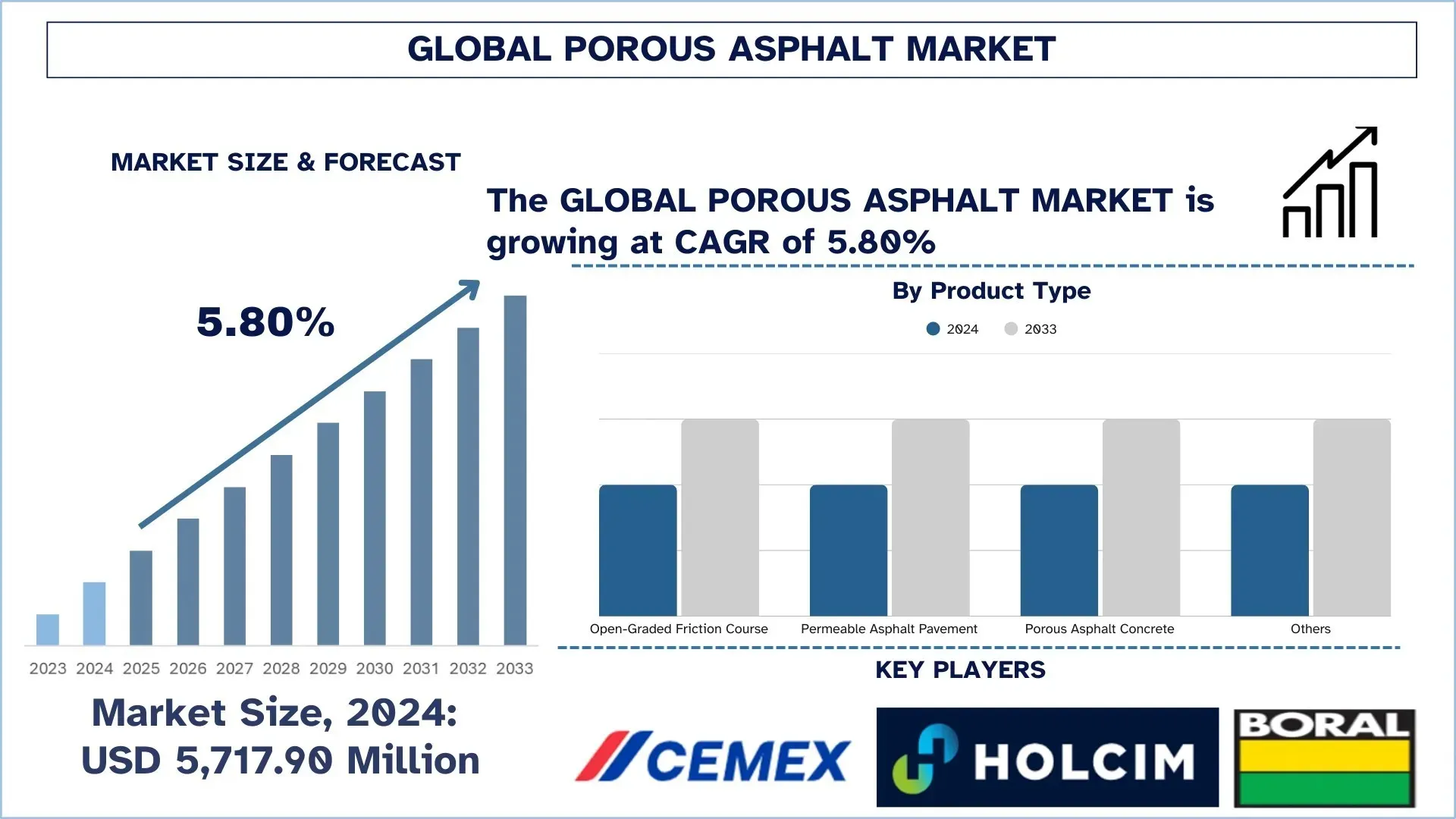

The Global Porous Asphalt Market was valued at USD 5,717.90 million in 2024 and is expected to grow at a CAGR of around 5.80% during the forecast period (2025–2033F), driven by tightening stormwater-management requirements, rising focus on wet-weather road safety, and the increasing adoption of permeable pavement solutions across transportation, commercial, and municipal infrastructure applications.

Porous Asphalt Market Analysis

The global porous asphalt market is expected to grow significantly over the forecast period, driven by the urgent need for long-term solutions to urban drainage challenges. This can be attributed to increasing regulatory pressure to manage stormwater runoff, reduce flood risk, and enhance groundwater recharge. As world cities grapple with climate change and stringent environmental regulations, porous asphalt is currently being employed to develop sustainable sponge city infrastructure. The high-permeability structure is primarily used on highways, parking areas, and municipal roads, where it is highly effective in filtering and draining rainwater, mitigating the effects of urban heat islands, and reducing the burden on the traditional sewer system. New material science, like polymer-modified binders and optimum aggregate mix, also contributes to the extension of market development, as it enhances durability and reduces clogging- an old nightmare of the technology. Through innovation and a focus on smart pavements and extended-service-life design, one can achieve the integration of porous asphalt as an essential component of present and climate-adaptive infrastructure at the global scale.

Global Porous Asphalt Market Trends

This section discusses the key market trends that are influencing the various segments of the global porous asphalt market, as found by our team of research experts.

Greater Use of Polymer-Modified Binders and Fiber

The use of polymer-modified binders and stabilizing fibers is one of the most noticeable trends in the global porous asphalt market, as owners and contractors are driving the adoption of porous/open-graded mixes to provide stable drainage and extended service in environments of increased traffic and more adverse weather. Since porous asphalt and OGFC/PFC layers contain large amounts of air voids and comparatively elevated binder contents, they are susceptible to binder drain down and durability losses (i.e., raveling/abrasion) when the binder is insufficiently rigid and not well stabilized. According to the latest best-practice guidance, modified asphalt binders are the norm in most State DOT OGFC mixtures, and the modifiers currently employed, including SBS and rubber, are used to enhance longevity and produce thicker, more robust binder coatings around the aggregate. Meanwhile, technical literature and agency reports are consistent in stating that the inclusion of fibers (often cellulose) reduces drain down, stabilizes the mix during handling and placement, and prevents moisture damage and rutting, without compromising the interlacing structure of voids required to allow passage of water. With an increasing number of projects specifying wet-weather safety, noise, and stormwater performance using a performance-based approach, polymer modification and fiber stabilization are no longer perceived as optional extensions of field performance and life, but rather as realistic means of achieving consistent field performance and extended service life for porous asphalt surfaces.

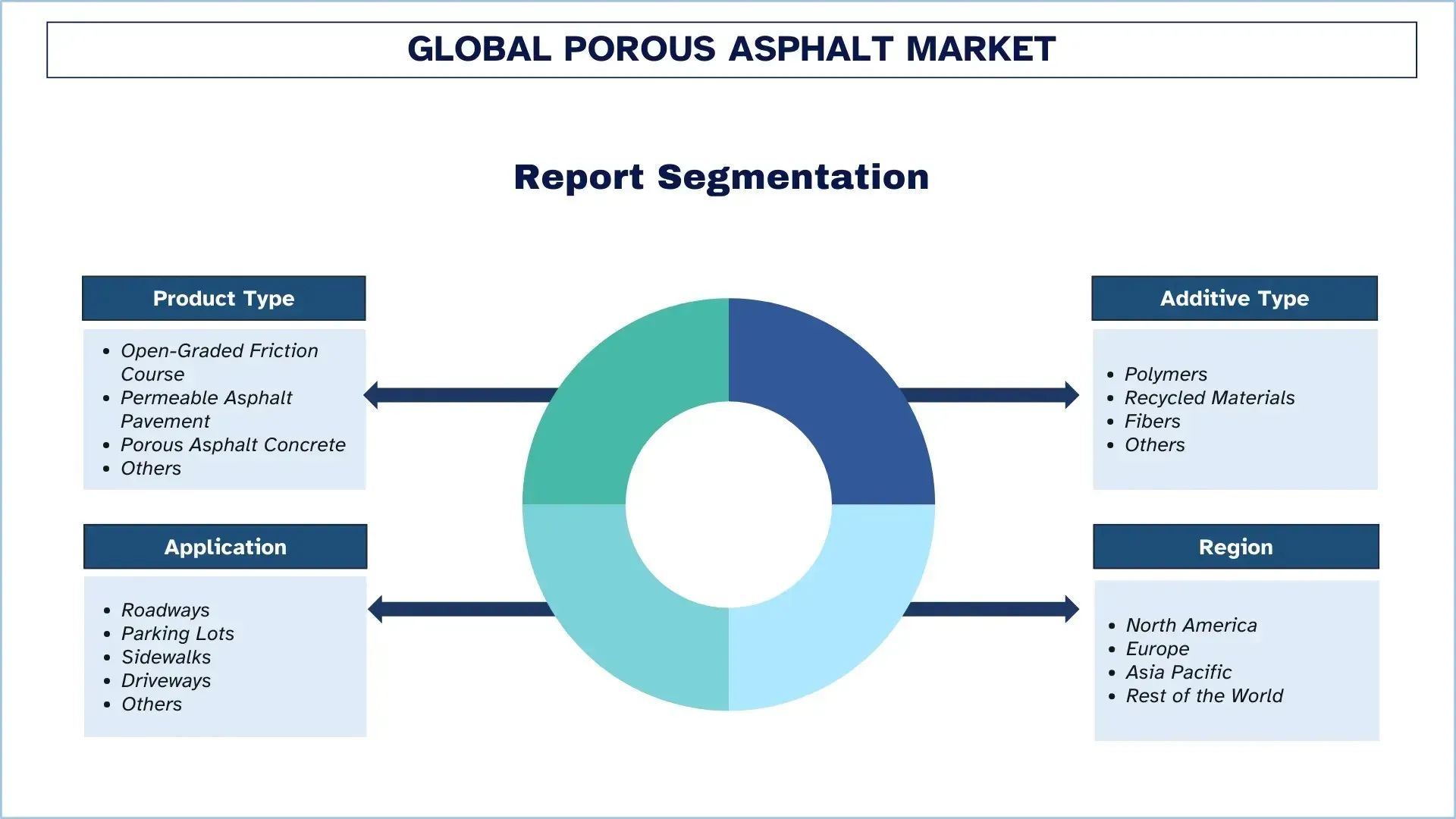

Porous Asphalt Industry Segmentation

This section provides an analysis of the key trends in each segment of the global porous asphalt market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Open-Graded Friction Course (OGFC) Segment held the Largest Market Share in the Porous Asphalt Market.

Based on product type, the global porous asphalt market is segmented into Open-Graded Friction Course (OGFC), Permeable Asphalt Pavement, Porous Asphalt Concrete, and Others. In 2024, the Open-Graded Friction Course (OGFC) segment is anticipated to hold the largest market share and continue its dominance throughout the forecast period. This is primarily because OGFC is commonly used as a wide-band, permeable surface layer in high-traffic roadways when agencies seek rapid surface drainage, improved wet-weather friction, and reduced splash-and-spray without necessarily reconstructing the entire road surface. The characteristics of OGFC that make it relatively easy to install as an overlay are also appreciated, as they allow owners to enhance the facility's safety performance without adding significant weight to the structure and causing minimal interference with existing assets. Moreover, to balance between permeability and durability (e.g., raveling resistance) through aggregate gradation control, binder adjustment, and stabilizing additives, OGFC mix designs can be tuned to support consistent operations across varying rainfall intensity and traffic loading. The Permeable Asphalt Pavement segment, however, is likely to expand with the fastest rate of increase as the stormwater compliance and urban-flood mitigation requirements continue to accelerate, particularly full-depth permeable systems with stone reservoirs deployed to contain the runoff at the source.

The Polymers Segment held the Largest Market Share in the Porous Asphalt Market.

Based on additive type, the global porous asphalt market is segmented into Polymers, Recycled Materials, Fibers, and Others. In 2024, the Polymers segment is anticipated to hold the largest market share and continue its dominance throughout the forecast period. This is primarily because a polymer-modified binder (e.g., SBS and other PMB systems) is widely being used to enhance the service life of open-graded/permeable asphalt to increase binder-aggregate bonding and increase resistance to ravelling, abrasion, cracking, moisture damage, and temperature-induced distress without compromising the interlacing void structure, providing the advantages of drainage and noise reduction. The recycled materials segment will, however, increase the most due to growing sustainability goals and a circular-economy supply chain for roadway and stormwater infrastructure. Agencies and contractors are investigating reclaimed asphalt pavement (RAP), industrial by-products (e.g., steel slag), and other recycled aggregates/fillers to reduce embodied impacts and material costs without compromising functional requirements (e.g., permeability and skid resistance).

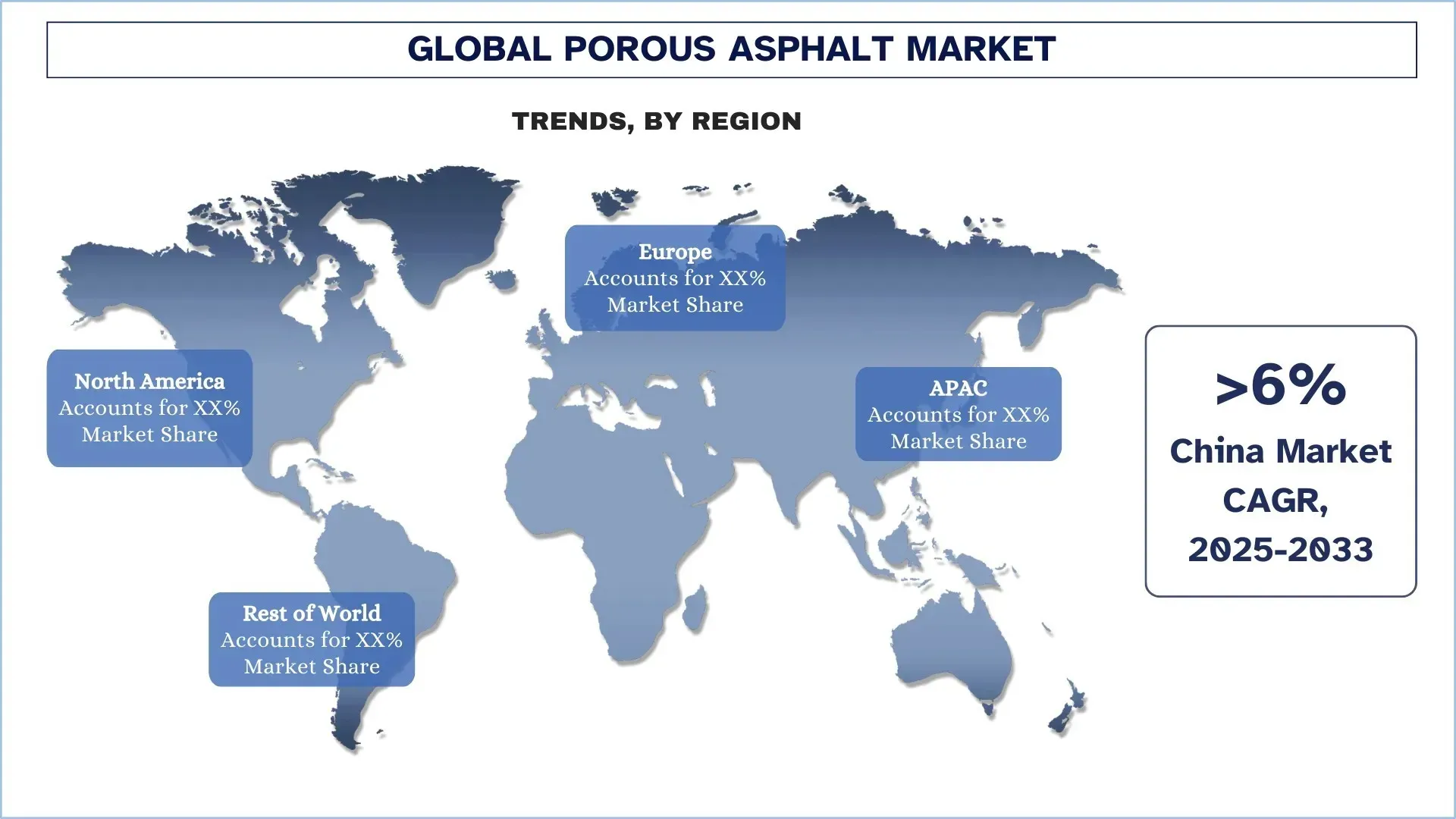

Asia Pacific Dominated the Global Porous Asphalt Market

The Asia-Pacific region dominates the global asphalt market and is expected to continue to do so over the forecast period. The rapid urbanization, massive expansion of transportation systems, and increasing investments in climate-resilient, flood-prevention infrastructure have given the Asia-Pacific region a competitive edge in the global porous asphalt market, particularly in China, Japan, and India. The intensity of rainfall in most sub-markets (monsoon-driven conditions), dense urbanization, and the increase in impervious surface area have increased demand for pavement solutions that enhance surface drainage and minimize runoff impacts. Moreover, the Asia-Pacific region has a broad network of road construction services, asphalt manufacturers, and municipal project pipelines, which enables the more rapid implementation of open-graded and permeable pavement technologies on highways, urban streets, parking lots, and civic amenities. As infrastructure modernization accelerates and wet-weather driving becomes more safety-oriented, performance advantages of adopting porous asphalt include reduced splash-and-spray, improved skid resistance, and a reduced risk of hydroplaning. The current transition to sustainable stormwater management, the desire for quieter urban corridors, and the pursuit of improved lifecycle performance through changes to binders and mix design further enhance market development in the region.

China held a dominant Share of the Asia Pacific Porous Asphalt Market in 2024

The success of China in the porous asphalt market has its roots in its vast infrastructure projects and the advanced nature of its manufacturing assets in high-end construction materials. The nation enjoys the advantage of an extensive, developed system of specialized manufacturing and downstream industries in the form of road engineering, urban works, and urban development. The basic factors leading to this growth are strict national policies, most of which are the Sponge City Initiative, which requires the management of stormwater to be sustainable to reduce urban flooding and recharge groundwater.

Porous Asphalt Industry Competitive Landscape

The global porous asphalt market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top Porous Asphalt Companies

Some of the major players in the market are Cemex S.A.B de C.V, Holcim, Boral, Tarmac, Colas, Skanska, CRH plc, Astec Industries, Inc., Graniterock, and Kilsaran.

Recent Developments in the Porous Asphalt Market

In August 2024, Eurovia announced the completion of a road resurfacing project on the RD1085 in Pas-de-Calais using its Up’Bio range of bio-based asphalt mixes. This initiative, which incorporated recycled materials and plant-based binders, successfully demonstrated a significant reduction in the carbon footprint of the infrastructure work.

In October 2025, Tarmac launched its CEVO Asphalts, a toolkit of engineered solutions designed to enable the UK's first truly Net Zero road construction. The system combines advanced bio binders, warm mix technology, and high levels of recycled material to cut asphalt emissions by up to 45%. When deployed with other measures like electric plants, it has already facilitated carbon reductions of up to 80% on major highway projects, demonstrating a practical path to zero-carbon roads without relying on offsets.

Global Porous Asphalt Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 5.80% |

Market size 2024 | USD 5,717.90 Million |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | Asia Pacific is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, and India |

Companies profiled | Cemex S.A.B de C.V, Holcim, Boral, Tarmac, Colas, Skanska, CRH plc, Astec Industries, Inc., Graniterock, and Kilsaran |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Product Type, By Additive Type, By Application, and By Region/Country |

Reasons to Buy the Porous Asphalt Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional-level analysis of the industry.

Customization Options:

The global Porous Asphalt Market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global Porous Asphalt Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global porous asphalt market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the porous asphalt value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global porous asphalt market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including product type, additive type, application, and regions within the global porous asphalt market.

The Main Objective of the Global Porous Asphalt Market Study

The study identifies current and future trends in the global porous asphalt market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current market size and forecast the market size of the global porous asphalt market and its segments in terms of value (USD).

Porous Asphalt Market Segmentation: Segments in the study include areas of product type, additive type, application, and regions.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the porous asphalt industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the porous asphalt market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global porous asphalt current market size and its growth potential?

The global porous asphalt market was valued at USD 5,717.90 million in 2024 and is expected to grow at a CAGR of 5.80% during the forecast period (2025-2033).

Q2: Which segment has the largest share of the global porous asphalt market by Product Type?

The Open-Graded Friction Course (OGFC) segment is anticipated to hold the largest market share primarily because OGFC is commonly used as a wide-band, permeable surface layer in high-traffic roadways when agencies seek rapid surface drainage, improved wet-weather friction, and reduced splash-and-spray without necessarily reconstructing the entire road surface.

Q3: What are the driving factors for the growth of the global porous asphalt market?

• Stricter Stormwater Management and Flood-Mitigation Needs

• Wet-Weather Road Safety Demand

• Sustainability and Green Building Mandates

Q4: What are the emerging technologies and trends in the global porous asphalt market?

• Greater Use of Polymer-Modified Binders and Fiber

• Integration with Smart City Infrastructure

Q5: What are the key challenges in the global porous asphalt market?

• Higher Initial Cost and Perceived Risk

• Clogging and Maintenance Requirements

Q6: Which region dominates the global porous asphalt market?

The Asia-Pacific region has dominated the porous asphalt market due to rapid urbanization, the massive expansion of transportation systems, and increasing investments in climate-resilient, flood-prevention infrastructure.

Q7: Who are the key players in the global porous asphalt market?

Some of the key companies include:

• Cemex S.A.B de C.V

• Holcim

• Boral

• Tarmac

• Colas

• Skanska

• CRH plc

• Astec Industries, Inc.

• Graniterock

• Kilsaran

Q8: How do stormwater-management rules and flood-mitigation mandates affect porous asphalt adoption in cities?

• Runoff-Reduction Targets: New drainage limits push permeable pavements to lower peak runoff.

• Compliance-Led Project Design: Municipal codes favor porous surfaces for detention and infiltration credits.

• More Retrofit Demand: Flood-prone streets, parking lots, and sidewalks get upgraded to meet norms.

Q9: How do performance standards and maintenance expectations influence purchasing decisions for porous asphalt?

• Clogging & Durability Concerns: Buyers prioritize mixes that resist raveling and maintain permeability.

• O&M Cost Visibility: Vacuuming/jetting needs shape lifecycle cost comparisons versus conventional asphalt.

• Specification-Driven Bidding: Standardized test methods and warranties increase confidence and tender wins.

Related Reports

Customers who bought this item also bought

Thin Bed Mortar Market: Current Analysis and Forecast (2025-2033)

Emphasis on Application (Tile & Stone Adhesive, Thin Joint Masonry (AAC/CLC Blocks), Insulation & Finishing Systems, Floor & Wall Layering, Repair, Renovation & Refurbishment, and Others); End-Use (Residential, Commercial, Industrial, and Others); Distribution Channel (Direct Sales, Retail Sales, Online, and Others); and Region/Country

January 6, 2026