Saudi Arabia Data Center Colocation Market: Current Analysis and Forecast (2025-2033)

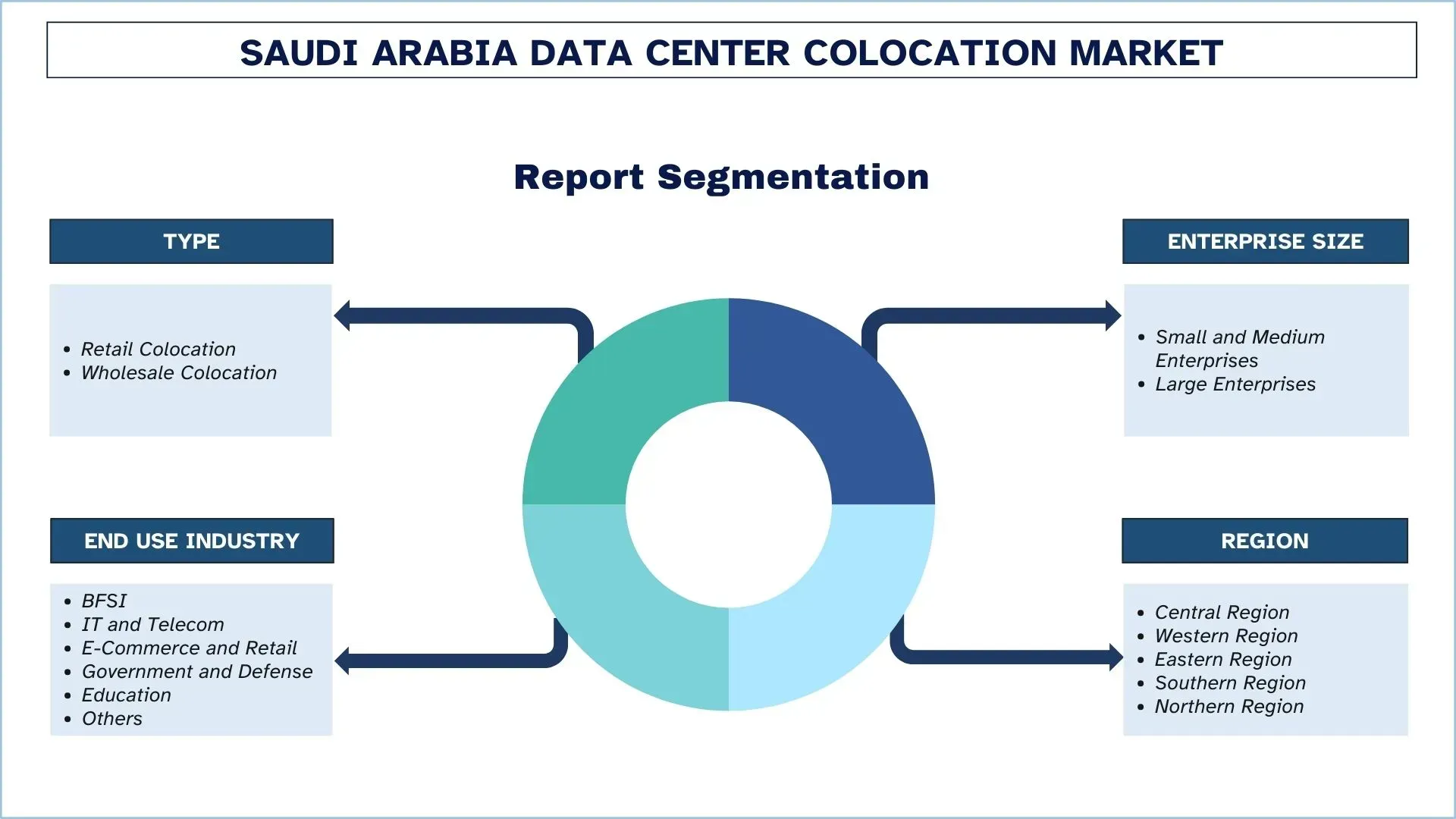

Emphasis on Type (Retail Colocation, Wholesale Colocation); Enterprise Size (Small and Medium Enterprises, Large Enterprises); End Use Industry (BFSI, IT and Telecom, E-Commerce and Retail, Government and Defense, Education, Others); and Region.

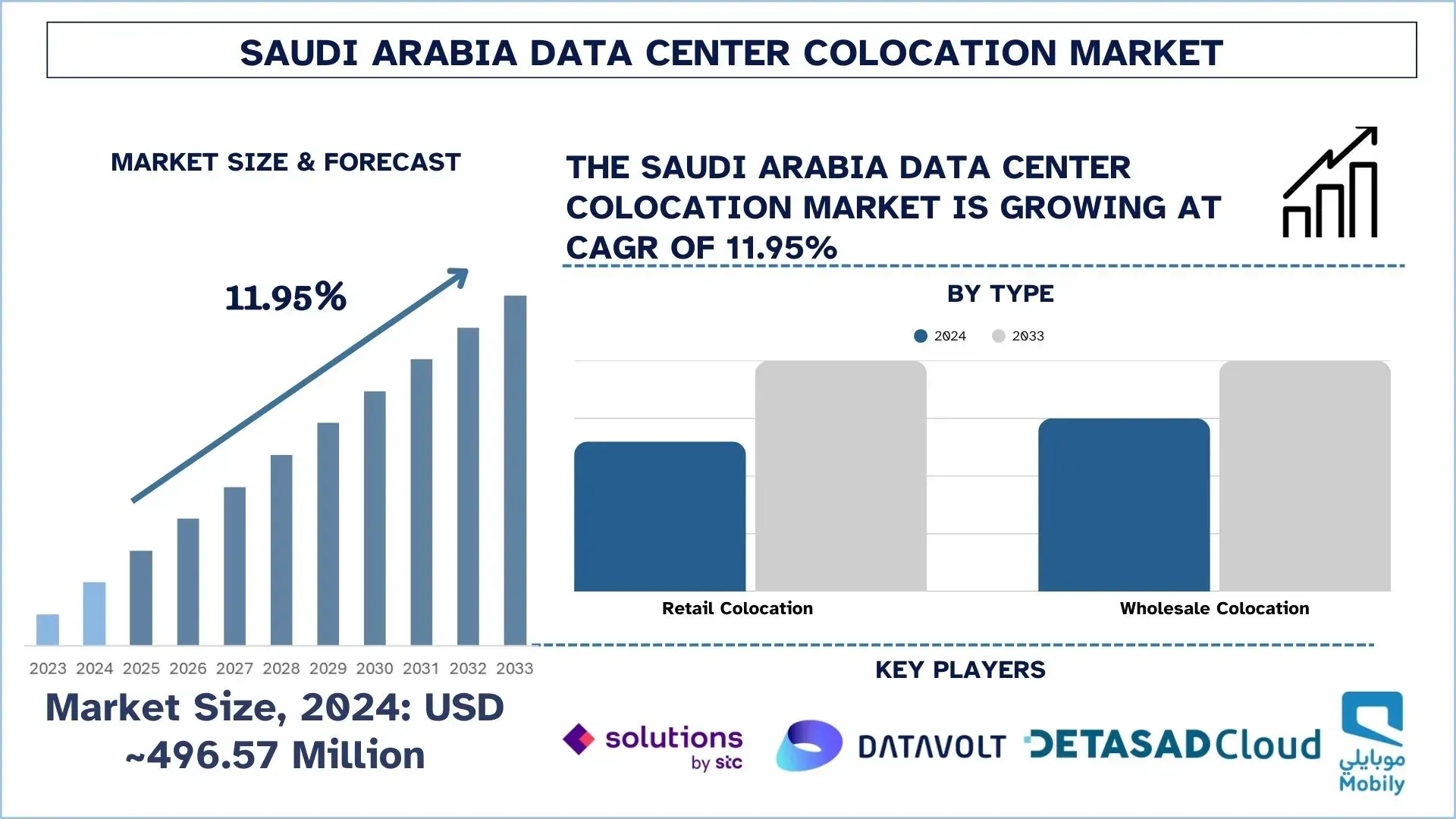

Saudi Arabia Data Center Colocation Market Size & Forecast

The Saudi Arabia Data Center Colocation Market was valued at USD 496.57 million in 2024 and is expected to grow at a strong CAGR of around 11.95% during the forecast period (2025-2033F), driven by growing cloud adoption and hybrid IT strategies across industries.

Saudi Arabia Data Center Colocation Market Analysis

Data colocation is the deployment of enterprise IT equipment in a professionally operated environment that has robust infrastructure. The facilities offer 24/7 availability, high bandwidth, and disaster recovery, ensuring that organizations achieve high reliability and compliance levels, as opposed to in-house setups.

The adoption of data center colocation is encouraged by the necessity to facilitate digital transformation, migration to the cloud, and alignment with the heavy data localization demands in Saudi Arabia. Additionally, companies are designing new facilities that hold Tier III and Tier IV certifications, featuring enhanced cooling systems, power redundancy, and high-speed connectivity to achieve enterprise-level performance. Simultaneously, investments in AI-ready infrastructure and regional growth are occurring in the market, making colocation a vital supporting infrastructure for the developing digital economy in the Kingdom.

For example, on July 9, 2025, XDS DATACENTRES signed a major agreement with ICS Arabia to deliver an initial state-of-the-art 10-megawatt immersion-cooled data centre in Riyadh & Jeddah. Under the terms of the agreement, ICS Arabia will design, construct, and hand over the facility to XDS by June 2026. The project will utilize Desert Dragon’s Tier III certified infrastructure and immersion cooling technology to support high-density workloads such as AI, machine learning, blockchain, and other GPU-intensive applications. The facility will set a new benchmark for energy-efficient, high-performance computing in the region.

Saudi Arabia Data Center Colocation Market Trends

This section discusses the key market trends that are influencing the various segments of the Saudi Arabia Data Center Colocation market, as found by our team of research experts.

Rapid Expansion of Cloud & AI-Ready Facilities

The rapid growth of cloud and AI-ready facilities is one of the key trends influencing the Saudi Arabia data center colocation market. Companies are now demanding infrastructure with the ability to support high-performance workloads, including AI, machine learning, and analytics of big data. As such, operators are investing in Tier III and IV certified centers that feature high power density and cooling, as well as hyperscale readiness. The given shift is not only a contributor to cloud migration but also makes Saudi Arabia a regional center of AI-driven digital ecosystems. For instance, on January 17, 2025, Gulf Data Hub and KKR announced that funds affiliated with KKR will acquire a stake in GDH. The investment, which is subject to customary regulatory approvals, is being made through KKR’s Global Infrastructure strategy. KKR and GDH are committing to support over USD 5 billion of total investment to build out data center capacity, supporting the significant rise in hyperscale demand, AI, and digital-focused national priorities across the Gulf countries.

Saudi Arabia Data Center Colocation Industry Segmentation

This section provides an analysis of the key trends in each segment of the Saudi Arabia Data Center Colocation market report, along with forecasts at the regional and provincial levels for 2025-2033.

The retail colocation market dominated the market share in 2024.

Based on type, the market is segmented into retail colocation and wholesale colocation. Among these, the retail colocation market held the largest share in 2024 because the enterprises are shifting towards smaller but scaled footprints that are managed by service providers rather than developing expensive in-house infrastructure. Additionally, scalability enables companies to increase capacity in response to digital transformation without requiring significant initial capital. The growing need for hybrid cloud and data security is establishing retail colocation as the preferred entry mode for many organizations.

The IT and telecom segments held a considerable market share in 2024.

Based on end-use industry, the market is segmented into BFSI, IT and telecom, e-commerce and retail, government & defense, education, and others. Among these, the IT and telecom segments held a considerable market share in 2024 due to the rising demand for infrastructure with large capacity and low latency to handle cloud services, as well as the rollout of 5G and digital platforms. The requirement for secure data storage and real-time connections drives continuous investment in sophisticated colocation facilities. For example, on February 7, 2025, Salam partnered with Netskope, a global leader in security and networking, to enhance data center services in the Kingdom. This collaboration will leverage Salam’s advanced data center infrastructure and Netskope’s expertise to provide secure and reliable colocation services for businesses.

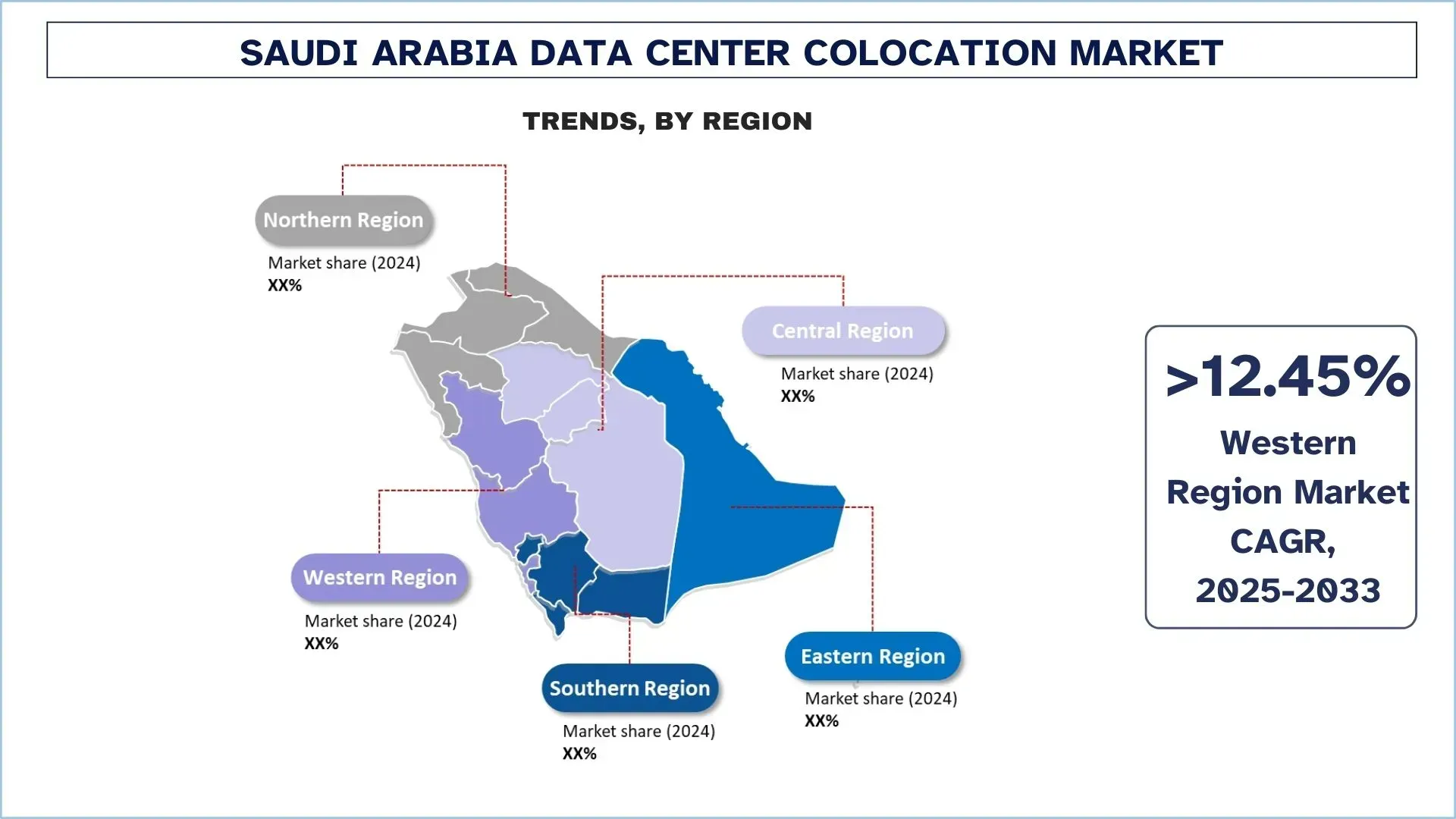

The Central Region led the market

The Central Region is home to numerous ministries of state, regulators, and corporate headquarters. Additionally, a significant number of data centre infrastructures are located in Riyadh, driven by the digital transformation of Vision 2030 and government projects. Moreover, the availability of BFSI, telecom, and multinational businesses ensures a secure, compliant, and high-capacity colocation workflow. Also, smart governance, cloud-first policies, and investments in AI adoption are compelling operators to increase their investments in Tier III and Tier IV data centers.

For example, on February 17, 2025, Etihad Etisalat Company (Mobily) announced that it would invest a substantial SAR 3.4 billion (approximately USD 905 million) in digital infrastructure in the Middle East. The announcement was made during the concluded LEAP 2025 technology conference in Riyadh. The amount would be invested in data centers, submarine cables, and fiber networks.

Saudi Arabia Data Center Colocation Industry Competitive Landscape

The Saudi Arabia Data Center Colocation market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top Saudi Arabia Data Center Colocation Companies

Some of the major players in the market are solutions by stc, DataVolt, WafaiCloud, DETASAD (Detecon Al Saudia Co. Ltd.), center3, Etihad Salam Telecom Company (Salam), Sahara Net, Zenlayer, Inc., EDGNEX Data Centres by DAMAC, Etihad Etisalat Company (Mobily).

Recent Developments in the Saudi Arabia Data Center Colocation Market

- On February 13, 2025, Ooredoo Group and Iron Mountain announced a landmark strategic partnership, which will see the global leader in information management services take a minority equity stake in Ooredoo’s carrier-neutral data centre company, MENA Digital Hub. Also, to meet the rising demand for colocation, AI, Cloud services, and hyperconnectivity in the region.

- On February 10, 2025, NEOM and DataVolt signed a landmark agreement, marking a significant step toward realizing the Kingdom’s vision for a sustainable, data-driven economy in Oxagon, Red Sea coast.

- An initial investment of USD 5 billion by DataVolt will fund the first phase of the factory’s development, expected to be operational by 2028.

- The agreement marks a significant milestone in the expansion of KSA's digital infrastructure, reinforcing its position as the region’s leading data hub.

- On October 6, 2023, stc group signed a strategic partnership with Red Sea Global (RSG), marking a significant milestone. This agreement aims to facilitate digital transformation and empower tourist destinations along the Red Sea coast by adopting state-of-the-art communication technologies and digital services, focusing on seamless and sustained connectivity services.

Saudi Arabia Data Center Colocation Market Report Coverage

Details | |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 11.95% |

Market size 2024 | USD 496.57 Million |

Regional analysis | Central Region, Western Region, Eastern Region, Southern Region, Northern Region |

Major contributing region | The Western Region is expected to grow at the highest CAGR during the forecasted period. |

Companies profiled | solutions by stc, DataVolt, WafaiCloud, DETASAD (Detecon Al Saudia Co. Ltd.), center3, Etihad Salam Telecom Company (Salam), Sahara Net, Zenlayer, Inc., EDGNEX Data Centres by DAMAC, Etihad Etisalat Company (Mobily) |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Type, By Enterprise Size, By End Use Industry, and By Region |

Reasons to Buy the Saudi Arabia Data Center Colocation Market Report:

- The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

- The report briefly reviews overall industry performance at a glance.

- The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

- Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

- The study comprehensively covers the market across different segments.

Customization Options:

The Saudi Arabia Data Center Colocation Market can further be customized as per requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Saudi Arabia Data Center Colocation Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the Saudi Arabian Data Center Colocation market to assess its application in major regions. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the Saudi Arabian Data Center Colocation value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the Saudi Arabia Data Center Colocation market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including type, enterprise size, end use industry, and region within the Saudi Arabian Data Center Colocation market.

The Main Objective of the Saudi Arabia Data Center Colocation Market Study

The study identifies current and future trends in the Saudi Arabia Data Center Colocation market, providing strategic insights for investors. It highlights market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current and forecast market size of the Saudi Arabia Data Center Colocation market and its segments in terms of value (USD).

Saudi Arabia Data Center Colocation Market Segmentation: Segments in the study include areas of type, enterprise size, end use industry, and region.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the Saudi Arabia Data Center Colocation industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as the Central Region, Western Region, Eastern Region, Southern Region, and Northern Region.

Company Profiles & Growth Strategies: Company profiles of the Saudi Arabia Data Center Colocation market and the growth strategies adopted by the market players to sustain in the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the Saudi Arabia Data Center Colocation market’s current market size and growth potential?

The Saudi Arabia Data Center Colocation market was valued at USD 496.57 million in 2024 and is projected to grow at a CAGR of 11.95% from 2025 to 2033. This growth is fueled by strong demand for cloud adoption, digital transformation, Vision 2030 initiatives, and increasing data localization requirements across various industries.

Q2: Which segment has the largest share of the Saudi Arabia Data Center Colocation market by type?

Retail colocation currently dominates the market, as it provides businesses with flexible, scalable, and cost-efficient solutions. This model is especially attractive for enterprises and SMEs looking to expand their digital capabilities without heavy upfront capital investment.

Q3: What are the driving factors for the growth of the Saudi Arabia Data Center Colocation market?

Key growth drivers include Vision 2030’s digital economy push, rising demand for cloud and hybrid IT solutions, data localization laws, rapid 5G rollout, and expansion in sectors such as BFSI, e-commerce, and government services. These factors are creating strong demand for advanced colocation facilities.

Q4: What are the emerging technologies and trends in the Saudi Arabia Data Center Colocation market?

The market is witnessing the rapid expansion of AI-ready facilities, modular data center designs, and wholesale colocation services for hyperscalers. Trends also include the use of green energy, advanced cooling technologies, and increasing adoption of Tier III and Tier IV certified facilities to ensure uptime and compliance.

Q5: What are the key challenges in the Saudi Arabia Data Center Colocation market?

The market faces challenges such as high capital investment for infrastructure development, shortage of skilled workforce, rising operational costs, and evolving cybersecurity threats. Additionally, increasing competition from international players adds pressure on local providers to innovate.

Q6: Which region dominates the Saudi Arabia Data Center Colocation market?

The Central Region (Riyadh) dominates the market as it hosts most government bodies, financial institutions, and corporate headquarters. Riyadh has the largest concentration of colocation facilities, making it the digital hub of the Kingdom, while the Western Region (Jeddah and Makkah) is emerging as a fast-growing secondary hub.

Q7: Who are the key players in the Saudi Arabia Data Center Colocation market?

Leading companies in the Saudi Arabia Data Center Colocation market include:

• solutions by stc

• DataVolt

• WafaiCloud

• DETASAD (Detecon Al Saudia Co. Ltd.)

• center3

• Etihad Salam Telecom Company (Salam)

• Sahara Net

• Zenlayer, Inc.

• EDGNEX Data Centres by DAMAC

• Etihad Etisalat Company (Mobily)

Q8: How does the Saudi Arabia Data Center Colocation market support businesses and investors?

The market enables businesses to reduce infrastructure costs, enhance scalability, and ensure compliance with local data regulations, while investors benefit from a rapidly growing sector aligned with Vision 2030’s digital economy goals. With high CAGR growth, it presents attractive opportunities for long-term investment and partnerships.

Q9: What future opportunities exist in the Saudi Arabia Data Center Colocation market?

Future opportunities lie in AI-driven colocation facilities, expansion into secondary cities like NEOM and Dammam, integration of renewable energy, and partnerships with global hyperscalers. As demand for secure, scalable digital infrastructure rises, colocation providers will play a central role in enabling Saudi Arabia’s digital leadership in the MENA region.

Related Reports

Customers who bought this item also bought

India IT and BPO Services Market: Current Analysis and Forecast (2026-2034)

Emphasis on Service Type (IT Services, BPO Services, Engineering & R&D Services); Outsourcing Type (Onshore, Offshore, Nearshore); Organization Size (Large Enterprises, SMEs); End-User Industry (BFSI, IT & Telecom, Healthcare, Retail & E-commerce, Manufacturing, Others); and Region/States

Gi-Fi Technology Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Display Devices and Network Infrastructure Devices); Technology (System on chip and Integrated Circuit Chip); Application (Consumer Electronics, Commercial, and Networking); and Region/Country

DNA Data Storage Market: Current Analysis and Forecast (2026-2034)

Emphasis on Type (Cloud and On-Premises); Technology (Sequence-based DNA Data Storage and Structure-based DNA Data Storage); End-User (Government, Healthcare & Biotechnology, Media & Telecommunication, and Others); and Region/Country

Cloud Service Brokerage Market: Current Analysis and Forecast (2026-2034)

Emphasis on Service Type (Integration and Support, Automation and Orchestration, Billing and Provisioning, Migration and Customization, Security and Compliance, and Others); Platform (Internal Brokerage Enablement and External Brokerage Enablement); Deployment (Private, Public, and Hybrid); Enterprise Size (Large Enterprises, and Small & Medium-Sized Enterprises); End-Use (IT & Telecom, BFSI, Government & Public Sector, Healthcare, Consumer Goods & Retail, Manufacturing, Energy & Utilities, and Others); and Region/Country