Neuromorphic Hardware Market: Current Analysis and Forecast (2025-2033)

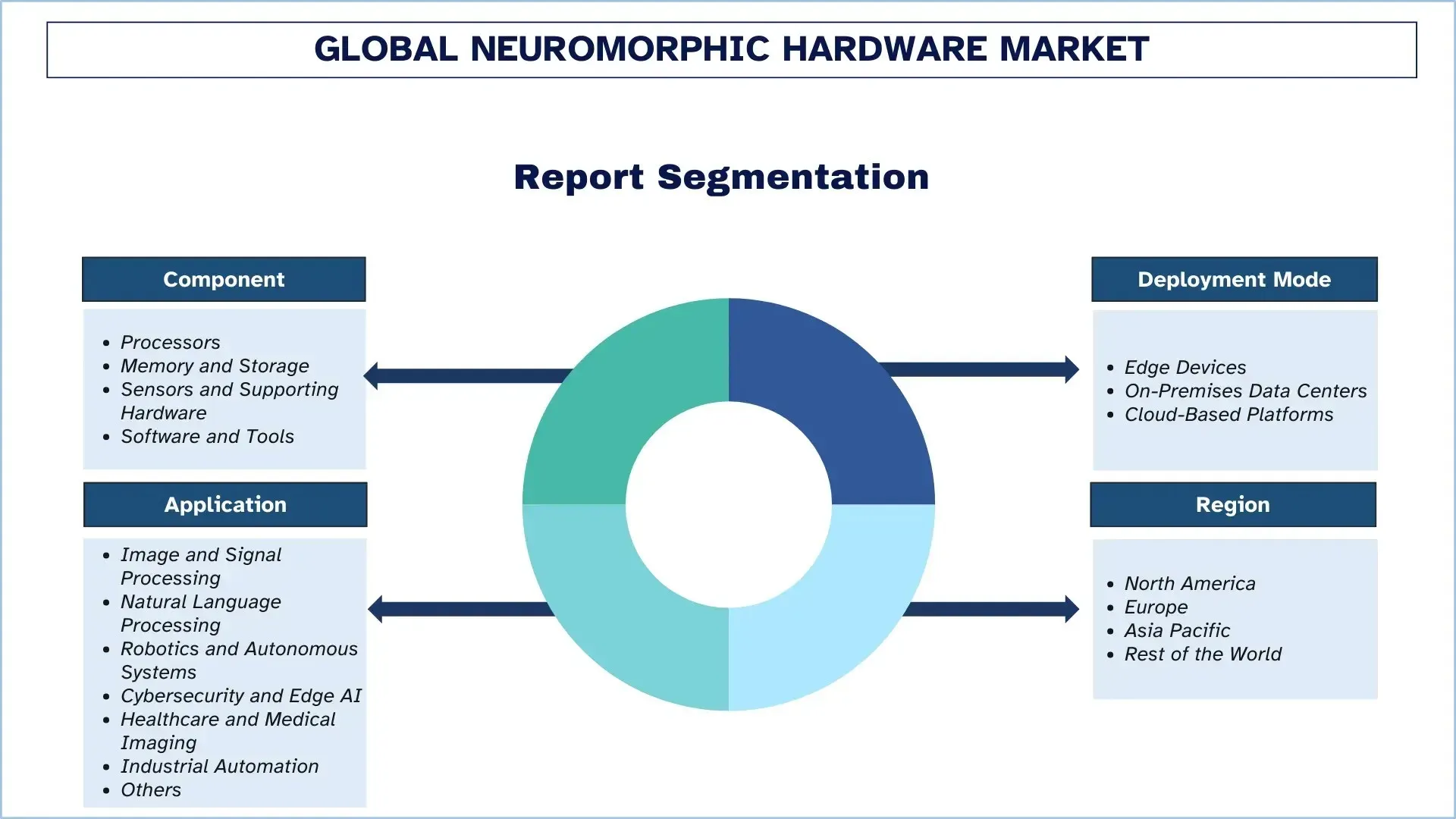

Emphasis on Component (Processors, Memory and Storage, Sensors and Supporting Hardware, and Software and Tools); Deployment Mode (Edge Devices, On-Premises Data Centers, and Cloud-Based Platforms); Application (Image and Signal Processing, Natural Language Processing, Robotics and Autonomous Systems, Cybersecurity and Edge AI, Healthcare and Medical Imaging, Industrial Automation, and Others); and Region/Country

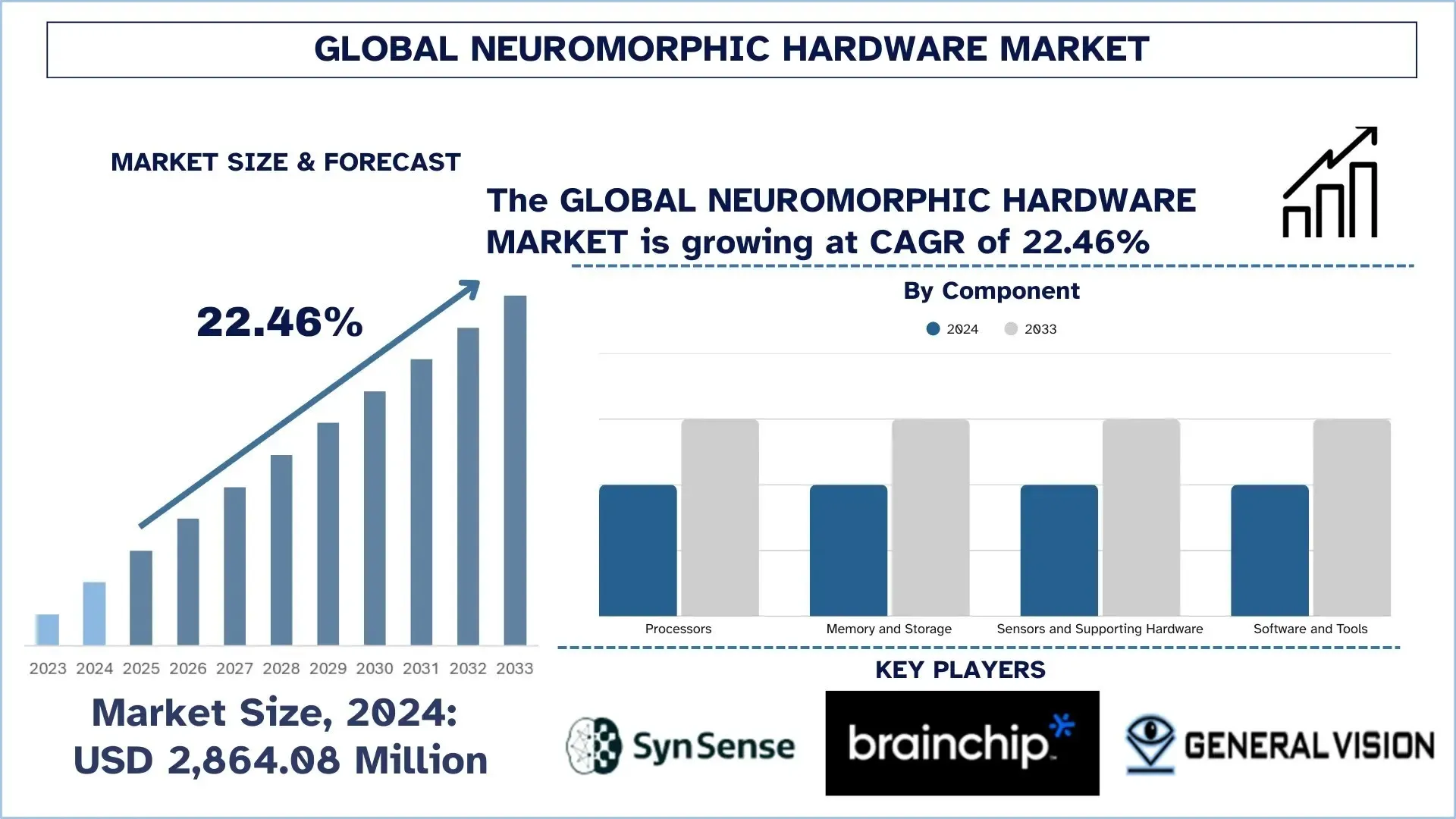

Global Neuromorphic Hardware Market Size & Forecast

The Global Neuromorphic Hardware Market was valued at USD 2,864.08 million in 2024 and is expected to grow at a CAGR of around 22.46% during the forecast period (2025–2033F), driven by rising demand for ultra-low-power, low-latency AI, increasing edge-computing adoption, and the need to reduce the energy and cost limits of conventional CPU/GPU-based inference across automotive, industrial, consumer, and defense applications.

Neuromorphic Hardware Market Analysis

The global neuromorphic hardware market is expected to grow robustly during the forecast period due to the dire necessity to have ultra-efficient, low-latency AI computing at the edge and in power-constrained settings. This expansion is enabled by the fact that there is a growing need for real-time perception and decision making in robotics, autonomous systems, industrial automation, and next-generation consumer devices, as well as mounting pressure to lower the energy and cost footprint of traditional GPU/CPU-based AI, with the drive to global industries to move towards always-on intelligence with tighter sustainability goals and higher data-privacy demands, neuromorphic architectures based on brain-like spiking neural networks-are receiving an ever-increasing interest to provide event-driven processing that consumes power orders of magnitude less. It finds applications most where asynchronous computation is useful (e.g., smart sensors, vision systems, adaptive control, and embedded inference), where responsiveness is important, bandwidth requirements are limited, and continuous learning (at the data source) is achievable. Further, long-term market development is driven by material science and device engineering-like memristive components, new non-volatile memories, and better on-chip interconnects, which are simpler to scale, are more reliable, and easier to manufacture, and address long-standing problems, such as the complexity of training and ecosystem fragmentation.

Global Neuromorphic Hardware Market Trends

This section discusses the key market trends that are influencing the various segments of the global neuromorphic hardware market, as found by our team of research experts.

Better SNN Software Tools, Compilers, and Standards

One of the trends in the world neuromorphic hardware market is the development of more powerful software tools and standards. Spiking neural networks (SNNs) are frequently adopted as neuromorphic systems, yet many groups cannot learn to use them because training, debugging, and deployment are often more complex than in standard AI frameworks. This is solved by better compilers, SDKs, libraries, and better benchmarking techniques that make models easier to build, performance easier to compare, and product transition easier. They also help minimize integration friction by enabling neuromorphic chips to operate in mixed systems (CPU/GPU + neuromorphic accelerators) and with event cameras. Thus, enhancing software and standards is an important tendency that favors the broader use of neuromorphic.

Neuromorphic Hardware Industry Segmentation

This section provides an analysis of the key trends in each segment of the global neuromorphic hardware market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Processor Segment held the Largest Market Share in the Neuromorphic Hardware Market.

Based on component type, the global neuromorphic hardware market is segmented into Processors, Memory and Storage, Sensors and Supporting Hardware, and Software and Tools. In 2024, the Processors segment is anticipated to hold the largest market share and maintain its dominance throughout the forecast period. This is largely because neuromorphic processors (such as event-driven inference chips or spiking neural network accelerators) are at the core of the compute layer that enables ultra-low-power, low-latency pattern recognition and adaptive decision-making across edge devices, robotics, and intelligent sensory platforms. Their ability to execute workloads very sparsely and asynchronously, frequently with less data movement and simpler signal-processing pipelines, makes them the investment choice for OEMs and system integrators to enhance performance per watt by addressing real-time performance requirements. In addition, processor-level innovation, including higher neuron/synapse density, on-chip interconnects, and closer integration with traditional CPUs/MCUs, enhances deployment flexibility and accelerates commercialization in both industrial and automotive-grade environments.

The Edge Devices Segment held the Largest Market Share in the Neuromorphic Hardware Market.

Based on deployment mode, the global neuromorphic hardware market is segmented into Edge Devices, On-Premises Data Centers, and Cloud-Based Platforms. In 2024, the Edge Devices segment is anticipated to hold the largest market share and sustain its dominance throughout the forecast period. This is mainly because neuromorphic systems are designed to execute event-driven, low-power, real-time inference, making them highly applicable on resource-constrained endpoints such as smart cameras, autonomous robots, drones, wearables, industrial controllers, and intelligent Internet of Things nodes. Local processing of sensory data using edge neuromorphic hardware accelerates latency. It minimizes bandwidth consumption, enabling privacy-centric architectures in which continuous streaming to centralized servers is infeasible or limited. Further, spiking processors can be combined with event-based sensors to create efficient perception pipelines that are responsive in dynamic environments, require less thermal load, and have prolonged battery life, which are important considerations in field-deployed systems. But the On-Premises Data Centers segment will experience the fastest growth as enterprises deploy neuromorphic accelerators to specialized workloads, including high-throughput signal analytics, adaptive control, and research-oriented simulation, where deterministic performance, security, or regulatory considerations favor local infrastructure.

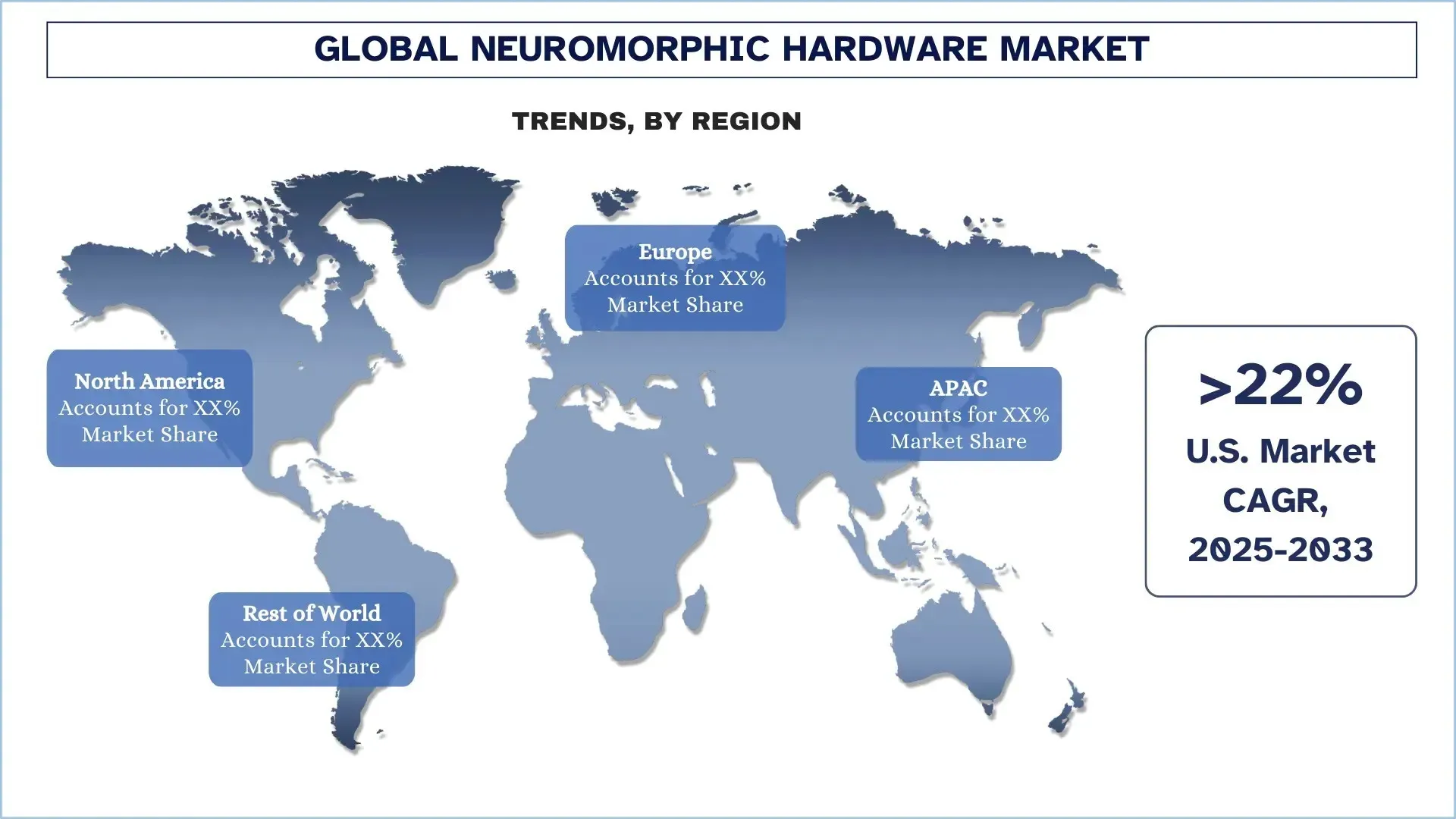

North America Dominated the Global Neuromorphic Hardware Market

The North America region dominates the global neuromorphic hardware market and is expected to maintain its lead over the forecast period. The primary driver of this leadership is the concentration of semiconductor innovation, AI research institutions, defense and aerospace programs, and deep-tech capital in the United States, particularly with Canadian support for advanced research and startups, which has accelerated the commercialization of neuromorphic processors and event-driven sensing platforms. One of the main factors that make the region a highly popular market for neuromorphic hardware in 2024 is the early adoption of energy-efficient neuromorphic computing across North America, particularly in edge computing, robotics, and mission-critical industrial and security workloads. Moreover, the ecosystem is well equipped with mature tools; pilot deployments are active; and there is strong collaboration among chip developers, cloud/edge platform vendors, system integrators, and end users, which supports faster validation cycles and facilitates the rapid scale-up of prototypes to actual deployments. With enterprises prioritizing low-latency on-device inference, privacy-aware processing, and power optimization, North America is well positioned to meet demand for next-generation autonomous, industrial, and national security applications.

U.S. held a dominant Share of the North America Neuromorphic Hardware Market in 2024

The US leads the global neuromorphic hardware market due to its optimal mix of advanced semiconductor design capabilities, AI research, and commercialization opportunities. The innovation cycle in U.S. chip and system creators has been shortened, with prototyping, taping-out, and iterating in minutes, and a diversity of universities and national labs gives a constant infusion of new architectures, algorithms, and talent into the system. The early need for ultra-low-power, low-latency computing with real-time capabilities is also evident in defense, aerospace, and security applications, to which neuromorphic applications are well-suited to address. Simultaneously, the U.S. has an established venture and startup system that invests in high-risk hardware innovation and facilitates collaboration with OEMs, cloud/edge platforms, and system integrators.

Neuromorphic Hardware Industry Competitive Landscape

The global neuromorphic hardware market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top Neuromorphic Hardware Companies

Some of the major players in the market are SynSense, BrainChip, Inc., General Vision Inc., Hewlett Packard Enterprise Development LP, IBM Corporation, Innatera Nanosystems BV, Intel Corporation, Knowm Inc., Blumind, and Numenta.

Recent Developments in the Neuromorphic Hardware Market

- In July 2025, Samsung announced an important breakthrough in the sphere of neuromorphic AI chips designed to work with edge computing. These brain-like chips mimic neural computation to make computing in devices like wearables and sensors incredibly efficient and with low power usage. The technology improves real-time, on-device data processing, reducing reliance on cloud resources and enhancing responsiveness and energy efficiency.

- In 2024, Fraunhofer will expose both analog and mixed-signal inference accelerators. That reduces data streams and offers very low latency to on-device signal processing. Furthermore, peer-reviewed articles indicate that femtojoule-equivalent energy per event on prototype pipelines targeted at embedded medical imaging and industrial inspection is likely to support segment growth.

- In 2024, Intel assembled Hala Point, a system that packages 1,152 Loihi-2 processors and supports over 1.15 billion neurons and 128 billion synapses. It operates at a peak power of approximately 2,600 W, and the experiment aims to provide system integrators with a method for scaling and benchmarking energy. Furthermore, this large-scale, replenished demonstration in 2024, when partnering across sectors, will ensure that North America is ahead of the pack in near-term demonstrations.

Global Neuromorphic Hardware Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 22.46% |

Market size 2024 | USD 2,864.08 Million |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | North America is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, and India |

Companies profiled | SynSense, BrainChip, Inc., General Vision Inc., Hewlett Packard Enterprise Development LP, IBM Corporation, Innatera Nanosystems BV, Intel Corporation, Knowm Inc., Blumind, and Numenta |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Component, By Deployment Mode, By Application, and By Region/Country |

Reasons to Buy the Neuromorphic Hardware Market Report:

- The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

- The report briefly reviews overall industry performance at a glance.

- The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

- Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

- The study comprehensively covers the market across different segments.

- Deep dive regional-level analysis of the industry.

Customization Options:

The Global Neuromorphic Hardware Market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global Neuromorphic Hardware Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global neuromorphic hardware market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the neuromorphic hardware value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global neuromorphic hardware market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including component, deployment mode, application, and regions within the global neuromorphic hardware market.

The Main Objective of the Global Neuromorphic Hardware Market Study

The study identifies current and future trends in the global neuromorphic hardware market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current market size and forecast the market size of the global neuromorphic hardware market and its segments in terms of value (USD).

Neuromorphic Hardware Market Segmentation: Segments in the study include areas of component, deployment mode, application, and regions.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the neuromorphic hardware industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the neuromorphic hardware market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global neuromorphic hardware current market size and its growth potential?

The global neuromorphic hardware market was valued at USD 2,864.08 million in 2024 and is expected to grow at a CAGR of 22.46% during the forecast period (2025-2033).

Q2: Which segment has the largest share of the global neuromorphic hardware market by Component?

The Processors segment is expected to hold the largest share throughout the forecast period because neuromorphic processors, such as event-driven inference chips and spiking neural network accelerators, form the core computational layer for ultra-low-power, low-latency pattern recognition and adaptive decision-making in edge devices, robotics, and intelligent sensing platforms.

Q3: What are the driving factors for the growth of the global neuromorphic hardware market?

• Demand for Low-Power and Low-Latency Edge AI

• Growth in Robotics and Autonomous Systems

• Data Privacy and Bandwidth Limits Pushing On-Device Inference over Cloud Processing

Q4: What are the emerging technologies and trends in the global neuromorphic hardware market?

• Better SNN Software Tools, Compilers, and Standards

• Integration with Event-Based Sensors and Hybrid AI Stacks

Q5: What are the key challenges in the global neuromorphic hardware market?

• Limited Ecosystem Maturity and Developer Adoption

• Scaling and ROI Uncertainty vs. Conventional AI Hardware

Q6: Which region dominates the global neuromorphic hardware market?

North America dominates the neuromorphic hardware market, led by U.S. chip innovation, AI R&D, defense demand, and deep-tech funding, with Canada reinforcing growth through research and startups.

Q7: Who are the key players in the global neuromorphic hardware market?

Some of the key companies include:

• SynSense

• BrainChip, Inc.

• General Vision Inc.

• Hewlett Packard Enterprise Development LP

• IBM Corporation

• Innatera Nanosystems BV

• Intel Corporation

• Knowm Inc.

• Blumind

• Numenta

Q8: How do data-privacy rules and AI governance policies affect neuromorphic hardware adoption in cities and public infrastructure?

• On-Device Inference Preference: Privacy requirements push sensitive video/audio analytics to run locally.

• Lower Data Transfer Exposure: Less cloud streaming reduces compliance and breach risk.

• Public-Sector Procurement Pull: Smart-city tenders favor secure, energy-efficient edge compute.

Q9: How do energy-efficiency targets and sustainability mandates influence purchasing decisions for neuromorphic hardware?

• Power-Budget Compliance: Buyers prioritize low-watt compute for always-on AI use cases.

• Lower Cooling And Opex: Reduced heat output cuts cooling needs in edge cabinets and facilities.

• ESG-Linked IT Roadmaps: Efficiency gains support carbon-reduction and green-IT goals.

Related Reports

Customers who bought this item also bought

Magnetoresistive RAM (MRAM) Market: Current Analysis and Forecast (2026-2034)

Emphasis on Type (Toggle MRAM and STT-MRAM); Application (Consumer Electronics, Automotive, Robotics, Aerospace & Defense, Enterprise Storage, and Others); and Region/Country

Ion Beam Etching System Market: Current Analysis and Forecast (2026-2034)

Emphasis on Type (Conventional Ion Beam Etching (IBE), Reactive Ion Beam Etching (RIBE), Focused Ion Beam (FIB) Systems, Automatic Ion Beam, and Others); Application (Semiconductor Manufacturing, Microelectronics & Data Storage, Photonics & Optoelectronics, MEMS (Micro-Electro-Mechanical Systems), Research & Metrology, and Others); End User (Semiconductor & Electronics, Aerospace & Defense, Healthcare & Medical Devices, Research Institutions, and Others); and Region/Country

25G Optical Module Market: Current Analysis and Forecast (2026-2034)

Emphasis on Product Type (SFP28, QSFP28, and CFP2); Application (Data Centers, Telecommunications, and Enterprise Networks); End-User (IT & Telecommunications, BFSI, Healthcare, Retail, and Others); and Region/Country

Power over Ethernet (PoE) Chipset Market: Current Analysis and Forecast (2025-2033)

Emphasis on Type (PoE Power Sourcing Equipment (PSE) Chipset and PoE Powered Devices (PD) Chipset); Standard (IEEE 802.3at Standard, IEEE 802.3bt Standard, and IEEE 802.3af Standard); Device (IP/Network Cameras, VoIP Phone, Ethernet Switch & Injector, Wireless Radio Access Point, Proximity Sensor, LED Lighting, and Others); End-use (Commercial, Industrial, and Residential); and Region/Country