- Home

- About Us

- Industry

- Services

- Reading

- Contact Us

25G Optical Module Market: Current Analysis and Forecast (2026-2034)

Emphasis on Product Type (SFP28, QSFP28, and CFP2); Application (Data Centers, Telecommunications, and Enterprise Networks); End-User (IT & Telecommunications, BFSI, Healthcare, Retail, and Others); and Region/Country

Global 25G Optical Module Market Size & Forecast

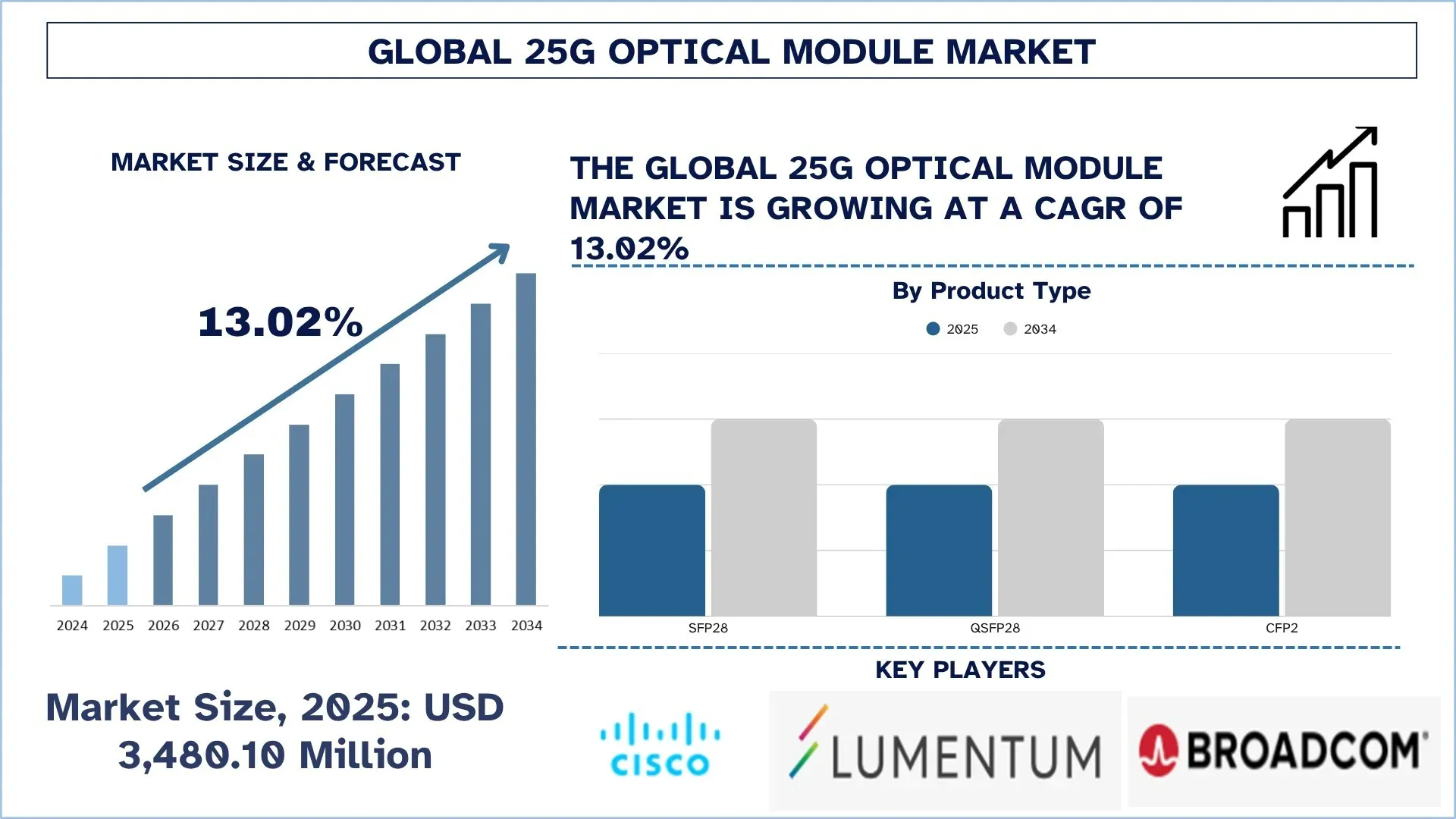

The Global 25G Optical Module Market was valued at USD 3,480.10 million in 2025 and is expected to grow at a strong CAGR of around 13.02% during the forecast period (2026-2034F), driven by the rapid expansion of 5G Network infrastructure, rising deployment of hyperscale data centers, and transition toward cost-efficient 25G Ethernet solutions.

25G Optical Module Market Analysis

25G optical modules are high-speed transceivers that allow data to be transmitted within networking environments like data centers, telecom infrastructure, and enterprise systems. Such modules provide a major performance advantage over standard 10G solutions in terms of bandwidth, reduced energy consumption, and reduced cost per bit, and are thus a popular choice in next-generation networking architectures. With the ever-growing exponential data traffic in organizations due to cloud computing, artificial intelligence, video streaming, and IoT applications, 25G optical modules are being adopted at an accelerating pace.

The market expansion is largely led by the fastest-growing nature of the 5G network infrastructure, the widespread use of hyperscale data centers, and the continued migration to the cost-effective 25G Ethernet solutions. Telecom operators are also spending a lot of money on updating their network infrastructure to incorporate 5G fronthaul and backhaul with 25G modules being very important in facilitating high-speed and low-latency communication. Meanwhile, hyperscale cloud providers and enterprises are moving to 25G and 10G solutions because they deliver superior performance without increasing overall costs, making the network more efficient as a whole. Additionally, the growing demand for high-speed connectivity in AI-driven workloads, edge computing, and digital transformation initiatives is further accelerating the adoption of 25G optical modules.

Global 25G Optical Module Market Trends

This section discusses the key market trends that are influencing the various segments of the global 25G Optical Module market, as found by our team of research experts.

Growing Integration in Cloud and AI Data Center Architectures

The increased integration of optical connectivity into cloud and AI data center architectures is one of the prominent trends in the global 25G Optical Module market. The design of data centers is increasingly informed by the requirements of AI training, inference, distributed computing, high-density switching, and scale-out clusters, creating demands for bandwidth density, latency control, and power efficiency. Optical modules are no longer considered as being separate connectivity elements; they are transitioning into a wider architecture of connecting servers, switches, accelerators, storage platforms, and inter-rack fabrics in a well-coordinated approach. This trend is important to the 25G market in that it solidifies the need to have reliable and energy-conscious optical links in the layers of infrastructure where cost-per-bit, compatibility, and operational flexibility still hold paramount value. In September 2025, the discussion of next-generation AI data center infrastructure by Lumentum provides a strong example with its focus on energy-efficient indium-phosphide photonics, pluggable transceivers, optical circuit switching, and future co-packaged optics as architectural components to support larger, more energy-efficient AI data centers. Lumentum also observed that its R300 optical circuit switch would scale to 100,000 and above Gordon Processor clusters and would consume as much as 65% less power than traditional switching fabrics, a factor that demonstrates how software demands by both clouds and AI architecture are having a direct impact on optical technology roadmaps.

25G Optical Module Industry Segmentation

This section provides an analysis of the key trends in each segment of the global 25G Optical Module market report, along with forecasts at the global, regional, and country levels for 2026-2034.

The SFP28 segment held a significant share during the forecast period (2026-2034).

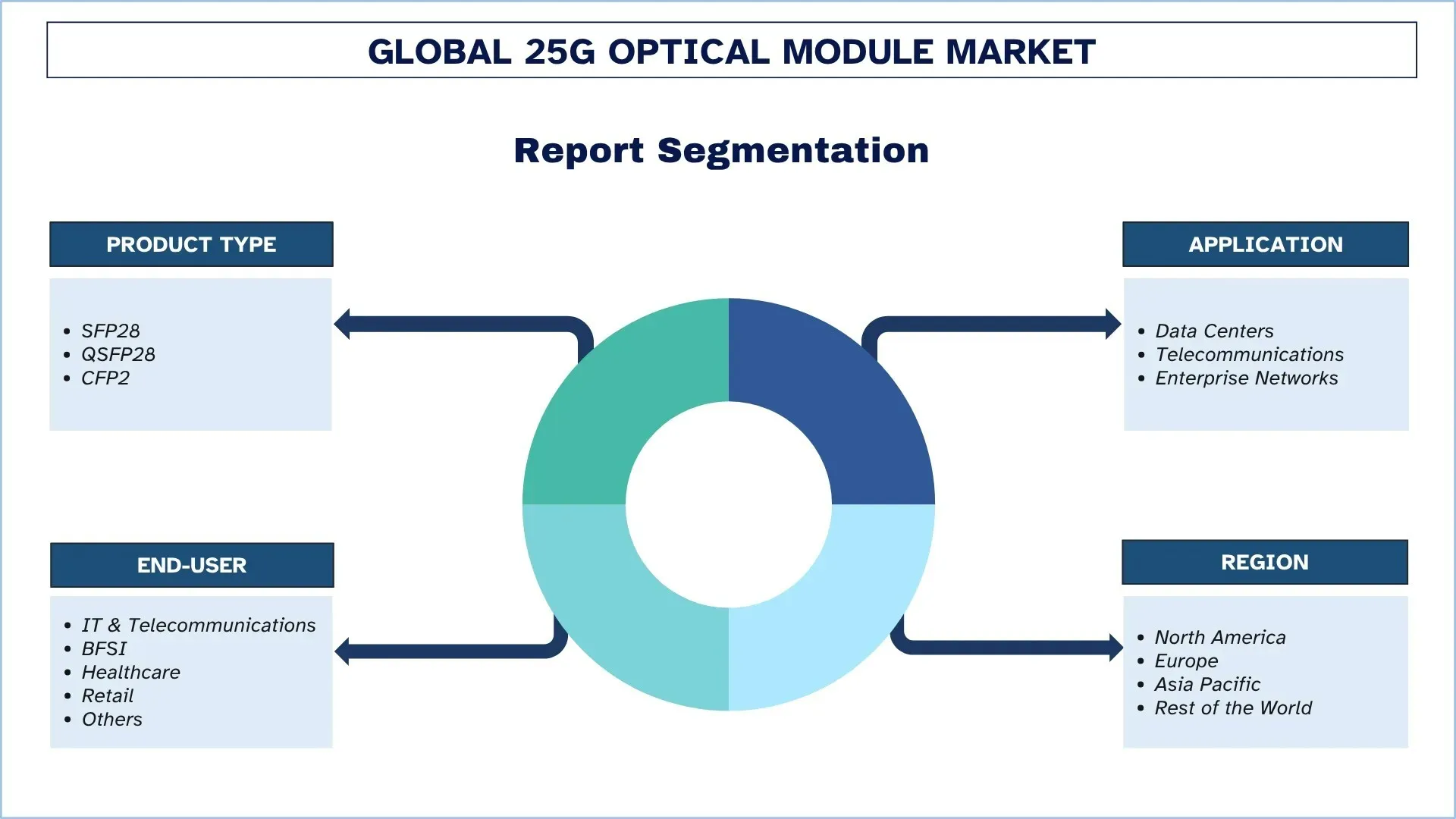

Based on product type, the Global 25G Optical Module market is segmented into SFP28, QSFP28, and CFP2. Among these, the SFP28 segment held the dominant market share in 2025 and is expected to maintain its position throughout the forecast period. SFP28 modules have become popular because of their small form factor, low power consumption, and cost efficiency, and they are suitable for high-density data center deployments. The modules enable organizations to transform their 10G networks to 25G without necessarily changing the infrastructure, which is a significant benefit to an enterprise that seeks to optimize costs and enhance performance.

The Data Centers Segment Dominates the Global 25G Optical Module Market.

Based on application, the Global 25G Optical Module market is segmented into Data Centers, Telecommunications, and Enterprise Networks. In 2025, the Data Centers segment held a significant share of the market. The growth contributes to several factors, such as the widespread adoption of 25G optical modules in contemporary data centers to facilitate high-speed data communications, increased bandwidth utilization, and low-cost migration of existing 10G infrastructure. Their increased utilization is also driven by accelerating adoption of cloud computing, hyperscale environments, AI-based workloads, and rising east-west traffic in data centers, all of which demand high-quality, scalable interconnect solutions. Moreover, 25G modules are becoming more popular with data center operators owing to the fact that such modules offer the right combination of performance, density, and power efficiency, and thus they are very suitable in large-scale server and switch connectivity.

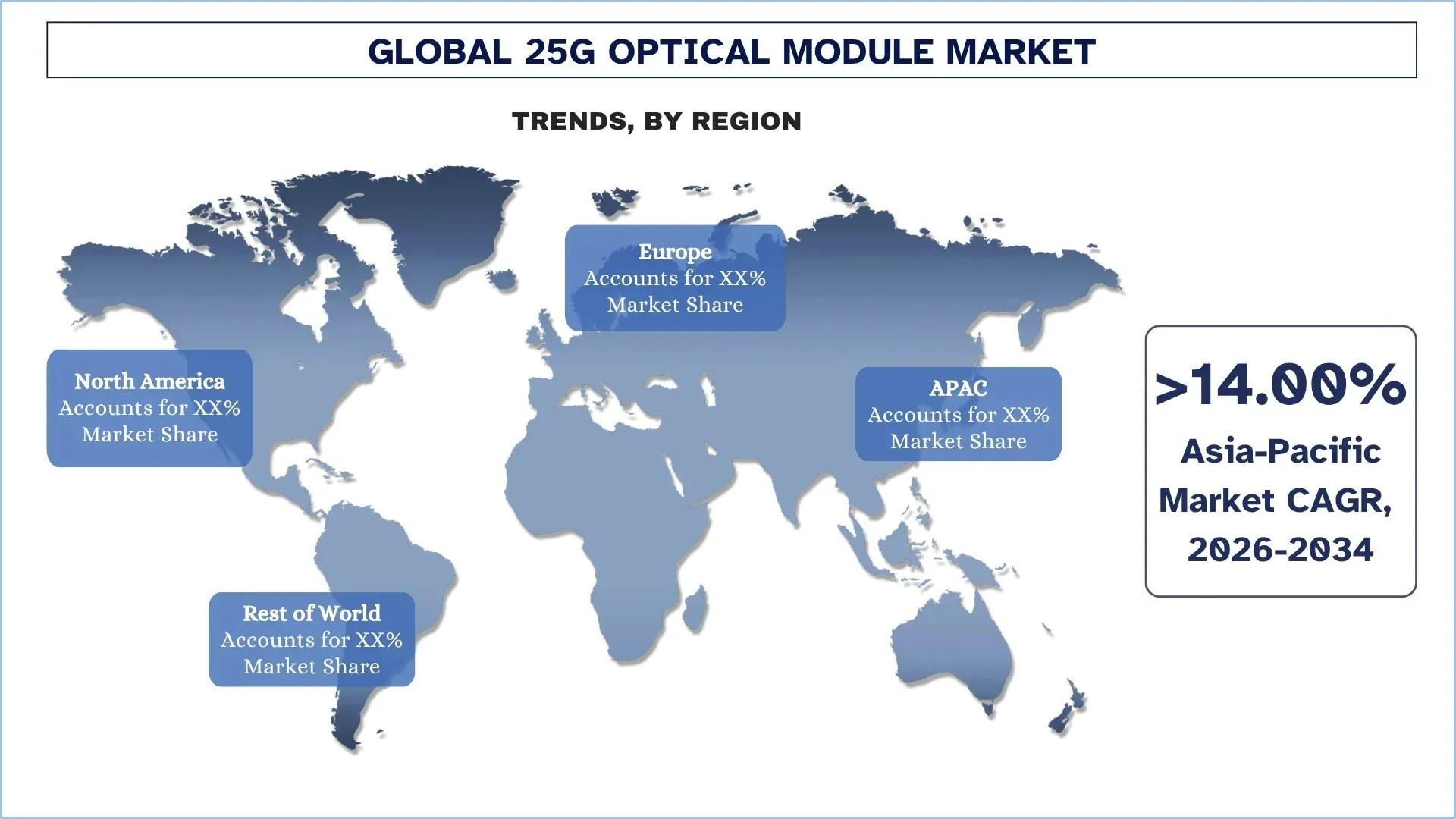

North America holds the largest market share in the global 25G Optical Module market

North America dominated the global 25G Optical Module market because of the high hyperscale data center base, developed cloud and AI infrastructure ecosystem, early adoption of high-speed optical networking technologies, and major telecom, semiconductor, and network equipment companies were located on the continent. The regional market is growing due to the increased need for high-bandwidth, low-latency, and energy-efficient connectivity of data centers, telecom transport networks, and enterprise digital infrastructures. Besides, there is constant investment in AI workloads, cloud migration, fiber rollout, and 5G network redesigning, which also promotes the use of 25G optical modules in North America. The region is also enjoying high advancement on optical interconnection technologies, a high rate of implementation of the advanced transceivers in the hyperscale facilities, and growing demands on scalable networking systems that can effortlessly handle the growing east-west traffic and AI-driven data loads. These aspects have still made North America an important revenue-generating region within the international market.

The United States held a dominant share of the North American 25G Optical Module Market in 2025

The U.S market led in the global and even in the North America 25G Optical Module market because of the highly established infrastructure of the hyperscale data centers, AI and cloud technology investment, the advanced modernization of telecom activity, and the availability of a large domestic networking, semiconductor, and optical technology industry. The country market is expanding due to increasing demand for high-bandwidth, low-latency, and energy-efficient optical connectivity in data centers, transport networks in telecom, in enterprise digital infrastructure, and in AI computing environments. In addition, the growing interest in AI infrastructure scale-out, national production of optical components, and development of next-generation interconnects are also contributing to the uptake within the U.S.

25G Optical Module Industry Competitive Landscape

The global 25G Optical Module market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, geographical expansions, and mergers and acquisitions.

Top 25G Optical Module Market Companies

Some of the major players in the market are Cisco Systems, Inc., Lumentum Operations LLC, Broadcom, FS.COM INC., Sumitomo Electric Industries, Ltd., Fujitsu, Applied Optoelectronics, Inc., Accelink Technology Co., Ltd., INNOLIGHT, and Huawei Technologies Co., Ltd.

Recent Developments in the 25G Optical Module Market

In March 2026, Lumentum Operations LLC declared a new manufacturing facility in Greensboro, North Carolina, in the United States to manufacture advanced indium phosphide optical devices to serve the largest AI data centers worldwide, enhancing U.S. capability to produce high-performance optical components in next-generation cloud and AI networking.

In April 2026, Applied Optoelectronics, Inc. released an order of 800G single-mode data center transceivers in bulk (USD 71 million), by a top hyperscale user, indicating the increasing optical interconnect usage by big optical infrastructure deployments.

In March 2025, Fujitsu launched its 1FINITY 800G ZR/ZR+ coherent pluggable transceivers, which are meant to reduce the power per bit by approximately 30 percent compared to earlier pluggable generations and metro, regional, and long-haul networks' AI-driven traffic growth.

In May 2025, Cisco Systems, Inc. declared that it would cooperate with the AI Infrastructure Partnership with BlackRock, Microsoft, NVIDIA, xAI, and others to aid with the rapid investment in AI data centers and enabling infrastructure, to bolster broader market momentum of high-speed optical networking ecosystems.

Global 25G Optical Module Market Report Coverage

Report Attribute | Details |

Base year | 2025 |

Forecast period | 2026-2034 |

Growth momentum | Accelerate at a CAGR of 13.02% |

Market size 2025 | USD 3,480.10 million |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | The North America region is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, and India. |

Companies profiled | Cisco Systems, Inc., Lumentum Operations LLC, Broadcom, FS.COM INC., Sumitomo Electric Industries, Ltd., Fujitsu, Applied Optoelectronics, Inc., Accelink Technology Co., Ltd., INNOLIGHT, and Huawei Technologies Co., Ltd. |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Product Type, By Application, By End-User, and By Region/Country |

Reasons to Buy the 25G Optical Module Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional level analysis of the industry.

Customization Options:

The global 25G Optical Module market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global 25G Optical Module Market Analysis (2024-2034)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global 25G Optical Module market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the 25G Optical Module value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global 25G Optical Module market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including product type, application, end-user, and regions within the global 25G Optical Module market.

The Main Objective of the Global 25G Optical Module Market Study

The study identifies current and future trends in the global 25G Optical Module market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current and forecast market size of the global 25G Optical Module market and its segments in terms of value (USD).

25G Optical Module Market Segmentation: Segments in the study include areas of product type, application, end-user, and region.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the 25G Optical Module industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the 25G Optical Module market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the current market size and growth potential of the global 25G Optical Module market?

The global 25G Optical Module market is valued at USD 3,480.10 million in 2025, driven by the rapid expansion of 5G Network infrastructure, rising deployment of hyperscale data centers, and transition toward cost-efficient 25G Ethernet solutions.

Q2: Which segment has the largest share of the global 25G Optical Module market by Product Type?

The SFP28 segment currently represents the most prominent product category in the market, supported by its compact design, lower power consumption, and cost-effective migration path from legacy 10G systems.

Q3: What are the driving factors for the growth of the global 25G Optical Module market?

Key growth drivers include the expansion of 5G network infrastructure, the rising deployment of hyperscale data centers, and the transition toward cost-efficient 25G Ethernet solutions that offer improved bandwidth, scalability, and lower cost per bit.

Q4: What are the emerging technologies and trends in the global 25G Optical Module market?

Key market trends include the growing integration of 25G optical modules in cloud and AI data center architectures, the shift toward energy-efficient and standards-compliant modules, and the increasing adoption of SFP28 and QSFP28 form factors across modern networking applications.

Q5: What are the key challenges in the global 25G Optical Module market?

Major challenges include high initial deployment and network upgrade costs, interoperability and compatibility issues across vendors and systems, and thermal management and power consumption constraints in high-density networking environments.

Q6: Which region dominates the global 25G Optical Module market?

North America dominates the market due to its strong presence of hyperscale data centers, advanced cloud and AI infrastructure, early adoption of high-speed optical networking technologies, and continuous investment in telecom modernization and enterprise digital infrastructure.

Q7: Who are the key competitors in the global 25G Optical Module market?

Top players in the 25G Optical Module industry include:

• Cisco Systems, Inc.

• Lumentum Operations LLC

• Broadcom

• FS.COM INC.

• Sumitomo Electric Industries, Ltd.

• Fujitsu

• Applied Optoelectronics, Inc.

• Accelink Technology Co. Ltd

• INNOLIGHT

• Huawei Technologies Co., Ltd.

Q8: What opportunities are emerging for new entrants and technology providers in this market?

Major opportunities include expanding use of 25G optical modules across BFSI, healthcare, and retail sectors, strong growth potential in emerging Asia-Pacific telecom markets, and rising demand for long-reach and low-power optical modules in advanced communication networks.

Q9: How is the expansion of hyperscale data centers influencing the 25G Optical Module market?

The rapid expansion of hyperscale data centers is significantly increasing demand for high-speed optical interconnect solutions. As cloud service providers and large enterprises scale their infrastructure to support AI, big data, and high-performance computing workloads, there is a growing need for reliable, low-latency, and cost-efficient connectivity between servers and switches.

Related Reports

Customers who bought this item also bought

Ion Beam Etching System Market: Current Analysis and Forecast (2026-2034)

Emphasis on Type (Conventional Ion Beam Etching (IBE), Reactive Ion Beam Etching (RIBE), Focused Ion Beam (FIB) Systems, Automatic Ion Beam, and Others); Application (Semiconductor Manufacturing, Microelectronics & Data Storage, Photonics & Optoelectronics, MEMS (Micro-Electro-Mechanical Systems), Research & Metrology, and Others); End User (Semiconductor & Electronics, Aerospace & Defense, Healthcare & Medical Devices, Research Institutions, and Others); and Region/Country

April 30, 2026

Power over Ethernet (PoE) Chipset Market: Current Analysis and Forecast (2025-2033)

Emphasis on Type (PoE Power Sourcing Equipment (PSE) Chipset and PoE Powered Devices (PD) Chipset); Standard (IEEE 802.3at Standard, IEEE 802.3bt Standard, and IEEE 802.3af Standard); Device (IP/Network Cameras, VoIP Phone, Ethernet Switch & Injector, Wireless Radio Access Point, Proximity Sensor, LED Lighting, and Others); End-use (Commercial, Industrial, and Residential); and Region/Country

April 17, 2026