MENA Heat Exchanger Market: Current Analysis and Forecast (2024-2032)

Emphasis on Type (Shell & Tube, Plate and Frame, Air-Cooled, And Others); Material (Plastics, Stainless Steel, and Aluminum Alloy); End-User (Chemical & Petrochemical, Oil & Gas, HVAC and Refrigeration, Food & Beverage, Power Generation, Paper & Pulp, And Others); and Country

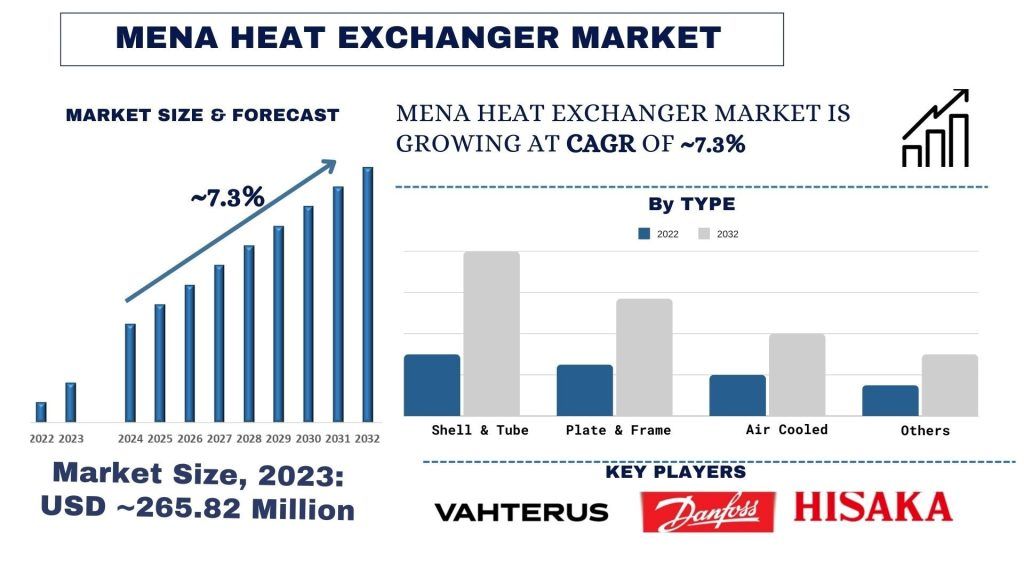

MENA Heat Exchanger Market Size & Forecast

MENA Heat Exchanger Market Size & Forecast

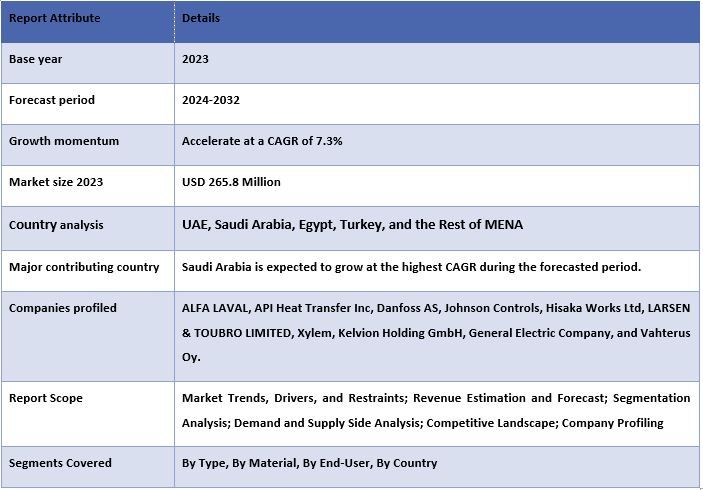

The MENA Heat Exchanger market was valued at approximately USD 265.8 Million in 2023 and is expected to grow at a robust CAGR of around 7.3% during the forecast period (2024-2032) owing to the increasing urbanization.

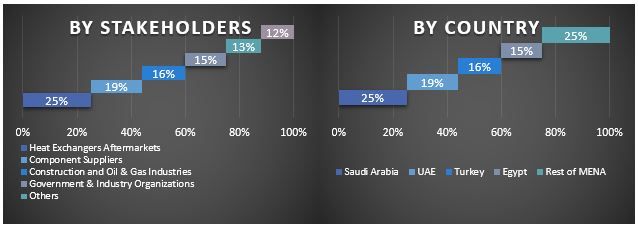

MENA Heat Exchanger Market Analysis

The heat exchanger market is growing steadily worldwide, and it is stimulated by people’s desire for higher efficiency and the ongoing expansion of industrial sectors. The heat exchanger is a device that is utilized in a way that enables the transfer of heat from one fluid medium to another through which the first fluid flows, and these fluids can be in the form of liquid or gases or may comprise a mixture of both liquids and gases. Some of its applications can be observed in chemical and petrochemical industries, oil and natural gas, electricity and power generation, refrigeration, and HVAC applications (heating, ventilation, and air conditioning). Hot gases and liquids flow through each type due to varied mechanisms, which enhance heat flow. For example, shell and tube heat exchangers have deep tubes through which heat exchange between hot and cold fluids occurs by contacting the walls of the tubes. Here, thin metal plates of one of the various types of patterns are arranged in series, and the fluids flow between these plates, in turn, to give up or absorb heat through the plates.

Companies in the Heat Exchanger market are actively pursuing various strategies to stimulate growth and meet the evolving demands of consumers. The MENA region is experiencing a growing adoption of heat exchangers, driven by the region’s focus on sustainability and energy efficiency. One instance of this trend is in the industrial sector, where heat exchangers are increasingly used to recover waste heat from various processes. For example, heat exchangers are employed in the oil and gas industry to capture and utilize the heat generated during refining. For instance, Saudi Aramco, the kingdom’s state-owned oil company, announced a significant investment in a project to develop a new refinery and petrochemical complex in Jazan. This project likely includes the use of various heat exchangers for refining processes. This reduces energy consumption and lowers operating costs for companies in the sector. Additionally, the region’s expanding district cooling systems rely heavily on heat exchangers to efficiently transfer heat, further boosting the demand for these devices. As the MENA region continues to prioritize sustainable development, adopting heat exchangers is expected to grow, driven by their crucial role in improving energy efficiency and reducing environmental impact.

MENA Heat Exchanger Market Trends

This section discusses the key market trends influencing the MENA heat exchanger market segments as identified by our research experts.

Type Transforming Industry

Based on the type, the market has been divided into shell & tube, plate and frame, air-cooled, and Others. The Shell and tube segment holds a significant market share and is expected to grow during the forecast period (2024-2032). These heat exchangers are preferred for their ability to handle high-pressure and high-temperature applications, making them ideal for industries such as oil and gas, petrochemicals, and power generation. The robust construction of shell and tube heat exchangers ensures their durability in harsh operating conditions, making them a reliable choice for regional industrial processes. Additionally, their design allows easy maintenance and cleaning, reducing downtime and improving overall efficiency.

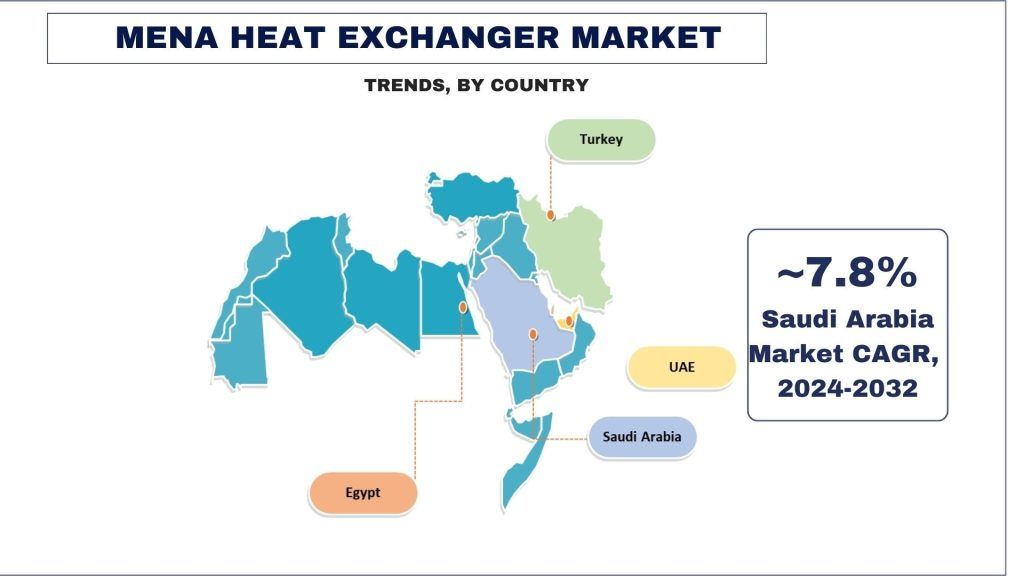

Saudi Arabia is Expected to Grow with Significant CAGR During Forecast Period

The growth of the heat exchanger market in Saudi Arabia is primarily driven by factors such as increasing disposable income levels and urbanization. Saudi Arabia is increasingly adopting heat exchangers, driven by its Vision 2030 plan to diversify its economy and reduce its reliance on oil. The development of mega-projects like NEOM and the focus on renewable energy projects create a significant demand for heat exchangers in solar and wind power applications. The country’s large industrial sector also contributes to the growing adoption of heat exchangers for various processes. For instance, Saudi Aramco, the kingdom’s state-owned oil company, announced a significant investment in a project to develop a new refinery and petrochemical complex in Jazan. This project likely includes the use of various heat exchangers for refining processes.

MENA Heat Exchanger Industry Overview

The MENA heat exchanger market is competitive, with several international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions. Some of the major players operating in the market are ALFA LAVAL, API Heat Transfer Inc, Danfoss AS, Johnson Controls, Hisaka Works Ltd, LARSEN & TOUBRO LIMITED, Xylem, Kelvion Holding GmbH, General Electric Company, and Vahterus Oy.

MENA Heat Exchanger Market News

For instance, Egypt’s Abu Qir Thermal Power Plant underwent a modernization project to improve efficiency and reduce emissions. Heat exchangers were likely used to enhance thermal management during the plant’s upgrade.

The Oman Power and Water Procurement Company (OPWP) announced plans to develop a new independent water project (IWP) in the country. Heat exchangers are likely to be used in the project’s desalination process to transfer heat and produce fresh water.

MENA Heat Exchanger Market Report Coverage

Reasons to buy this report:

- The study includes market sizing and forecasting analysis validated by authenticated key industry experts.

- The report briefly reviews overall industry performance at one glance.

- The report covers an in-depth analysis of prominent industry peers with a primary focus on key business financials, product portfolios, expansion strategies, and recent developments.

- Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

- The study comprehensively covers the market across different segments.

- Deep dive regional level analysis of the industry.

Customization Options:

The MENA heat exchanger market can further be customized as per the requirement or any other market segment. Besides this, UMI understands that you may have your own business needs; hence, feel free to connect with us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the MENA Heat Exchanger Market Analysis (2024-2032)

Analyzing the historical market, estimating the current market, and forecasting the future market of the MENA Heat Exchanger market were the three significant steps undertaken to create and analyze the adoption of MENA Heat Exchanger in major countries. Exhaustive secondary research was conducted to collect the historical market numbers and estimate the current market size. Secondly, numerous findings and assumptions were taken into consideration to validate these insights. Moreover, exhaustive primary interviews were also conducted, with industry experts across the value chain of the MENA Heat Exchanger market. Post assumption and validation of market numbers through primary interviews, we employed a top-down/bottom-up approach to forecasting the complete market size. Thereafter, market breakdown and data triangulation methods were adopted to estimate and analyze the market size of segments and sub-segments of the industry. Detailed methodology is explained below:

Analysis of Historical Market Size

Step 1: In-Depth Study of Secondary Sources:

A detailed secondary study was conducted to obtain the historical market size of the MENA Heat Exchanger market through company internal sources such as annual reports & financial statements, performance presentations, press releases, etc., and external sources including journals, news & articles, government publications, competitor publications, sector reports, third-party database, and other credible publications.

Step 2: Market Segmentation:

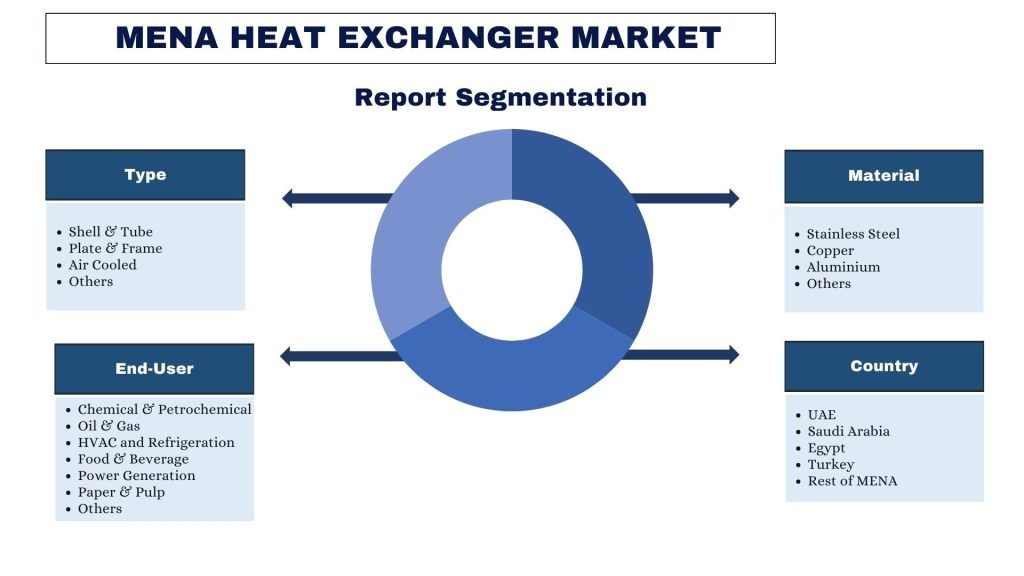

After obtaining the historical market size of the MENA Heat Exchanger market, we conducted a detailed secondary analysis to gather historical market insights and share for different segments & sub-segments for major countries. Major segments are included in the report as type, material, end-user, and countries. Further country-level analyses were conducted to evaluate the overall adoption of testing models in that region.

Step 3: Factor Analysis:

After acquiring the historical market size of different segments and sub-segments, we conducted a detailed factor analysis to estimate the current market size of the MENA Heat Exchanger market. Further, we conducted factor analysis using dependent and independent variables such as type, material, end-user, and MENA heat exchanger market countries. A thorough analysis was conducted for demand and supply-side scenarios considering top partnerships, mergers and acquisitions, business expansion, and product launches in the MENA Heat Exchanger market sector.

Current Market Size Estimate & Forecast

Current Market Sizing: Based on actionable insights from the above three steps, we arrived at the current market size, key players in the MENA heat exchanger market, and market shares of the segments. All the required percentage shares split, and market breakdowns were determined using the above-mentioned secondary approach and were verified through primary interviews.

Estimation & Forecasting: For market estimation and forecast, weights were assigned to different factors including drivers & trends, restraints, and opportunities available for the stakeholders. After analyzing these factors, relevant forecasting techniques i.e., the top-down/bottom-up approach were applied to arrive at the market forecast for 2032 for different segments and sub-segments across the major markets. The research methodology adopted to estimate the market size encompasses:

- The industry’s market size, in terms of revenue (USD) and the adoption rate of the MENA heat exchanger market across the major markets domestically

- All percentage shares, splits, and breakdowns of market segments and sub-segments

- Key players in the MENA Heat Exchanger market in terms of products offered. Also, the growth strategies adopted by these players to compete in the fast-growing market

Market Size and Share Validation

Primary Research: In-depth interviews were conducted with the Key Opinion Leaders (KOLs), including Top Level Executives (CXO/VPs, Sales Head, Marketing Head, Operational Head, Regional Head, Country Head, etc.) across major regions. Primary research findings were then summarized, and statistical analysis was performed to prove the stated hypothesis. Inputs from primary research were consolidated with secondary findings, hence turning information into actionable insights.

Split of Primary Participants in Different Countries

Market Engineering

The data triangulation technique was employed to complete the overall market estimation and to arrive at precise statistical numbers for each segment and sub-segment of the MENA heat exchanger market. Data was split into several segments and sub-segments after studying various parameters and trends in the type, material, end-user, and countries of the MENA Heat Exchanger market.

The main objective of the MENA Heat Exchanger Market Study

The current & future market trends of the MENA Heat Exchanger market were pinpointed in the study. Investors can gain strategic insights to base their discretion for investments on the qualitative and quantitative analysis performed in the study. Current and future market trends determined the overall attractiveness of the market at a regional level, providing a platform for the industrial participant to exploit the untapped market to benefit from a first-mover advantage. Other quantitative goals of the studies include:

- Analyze the current and forecast market size of the MENA heat exchanger market in terms of value (USD). Also, analyze the current and forecast market size of different segments and sub-segments.

- Segments in the study include areas of type, material, end-user, and countries.

- Define and analyze the regulatory framework for the MENA heat exchanger

- Analyze the value chain involved with the presence of various intermediaries, along with analyzing customer and competitor behaviors of the industry.

- Analyze the current and forecast market size of the MENA Heat Exchanger market for the major region.

- Major countries of regions studied in the report include UAE, Saudi Arabia, Egypt, Turkey and Rest of MENA

- Company profiles of the MENA Heat Exchanger market and the growth strategies adopted by the market players to sustain in the fast-growing market.

- Deep dive regional level analysis of the industry

Frequently Asked Questions FAQs

Q1: What is the MENA heat exchanger market's current size and growth potential?

Q2: What are the driving factors for the growth of the MENA heat exchanger market?

Q3: Which segment has the largest MENA heat exchanger market share by type?

Q4: What are the emerging technologies and trends in the MENA heat exchanger market?

Q5: Which country will dominate the MENA Heat Exchanger market?

Related Reports

Customers who bought this item also bought

India Decarbonization HVAC Market: Current Analysis and Forecast (2026-2034)

Emphasis on Product Type (Heating Equipment, Ventilation Equipment, Air Conditioning Equipment, Others); Decarbonization Type (Direct, Indirect); Capacity (Up to 5 Tons, 5-20 Tons, Above 20 Tons); End User (Commercial Buildings, Residential Buildings, Industrial Facilities, Healthcare Facilities, Data Centers, Others); and Region/States

Midstream Oil & Gas Filtration Market: Current Analysis and Forecast (2026-2034)

Emphasis on Filter Technology (Coalescer Filters, Cartridge Filters, Mechanical Filters, Bag Filters, Particulate Filters, Activated Carbon Filters, Strainers, and Others); by Application (Gas Processing Plants, Compression Stations, Storage And Distribution, Pipeline Transportation, LNG Processing, and Others); by Filtration Stage (Oil Filtration and Gas Filtration), by End User (Refineries and Petrochemical Industry), and Region/Country

Hydrogen-Powered Hospital Backup Systems Market: Current Analysis and Forecast (2026-2034)

Emphasis on System Type (Portable, Stationary, Hybrid); Power Capacity (Below 100 kW, 100–500 kW, and Above 500 kW); End-User (Public Hospitals, Private Hospitals, Specialty Hospitals, and Emergency Care Facilities); and Region/Country

Wind LiDAR Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Vertical Profiling Wind LiDAR, Ground-Based Wind LiDAR, Nacelle-Mounted Wind LiDAR, Airborne Wind LiDAR, and Others); Component (Sensor, Navigator, Laser, and Others); Location (Onshore and Offshore); Application (Wind Power, Meteorology & Environment, and Aviation); and Region/Country