LGC And VLGC LPG Shipyard Carrier Market: Current Analysis and Forecast (2025-2033)

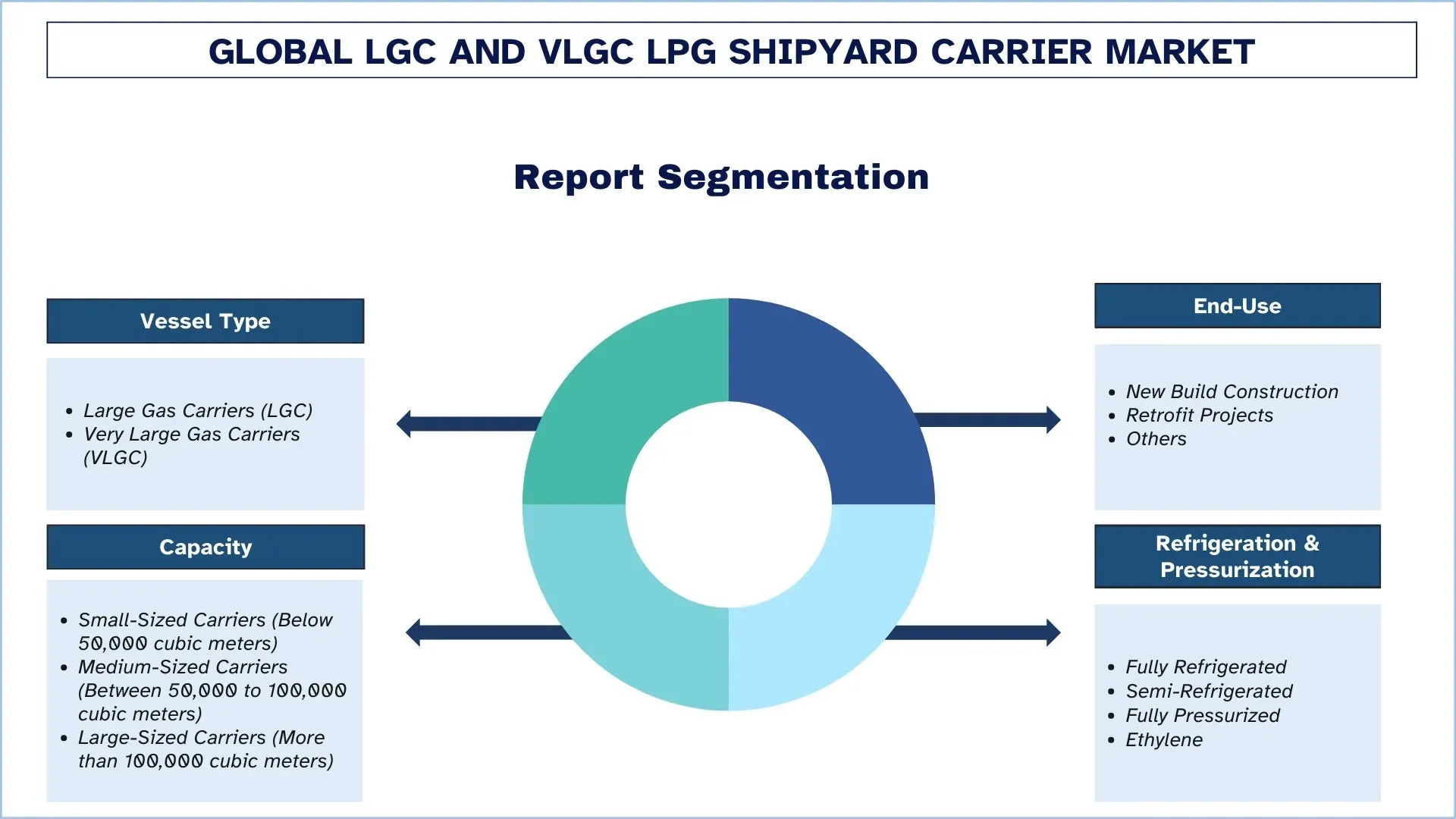

Emphasis on Vessel Type (Large Gas Carriers (LGC) and Very Large Gas Carriers (VLGC)); Capacity (Small-Sized Carriers {Below 50,000 cubic meters}, Medium-Sized Carriers {Between 50,000 to 100,000 cubic meters}, and Large-Sized Carriers {More than 100,000 cubic meters}); End-Use (New Build Construction, Retrofit Projects, and Others); Refrigeration & Pressurization (Fully Refrigerated, Semi-Refrigerated, Fully Pressurized, and Ethylene) and Region/Country

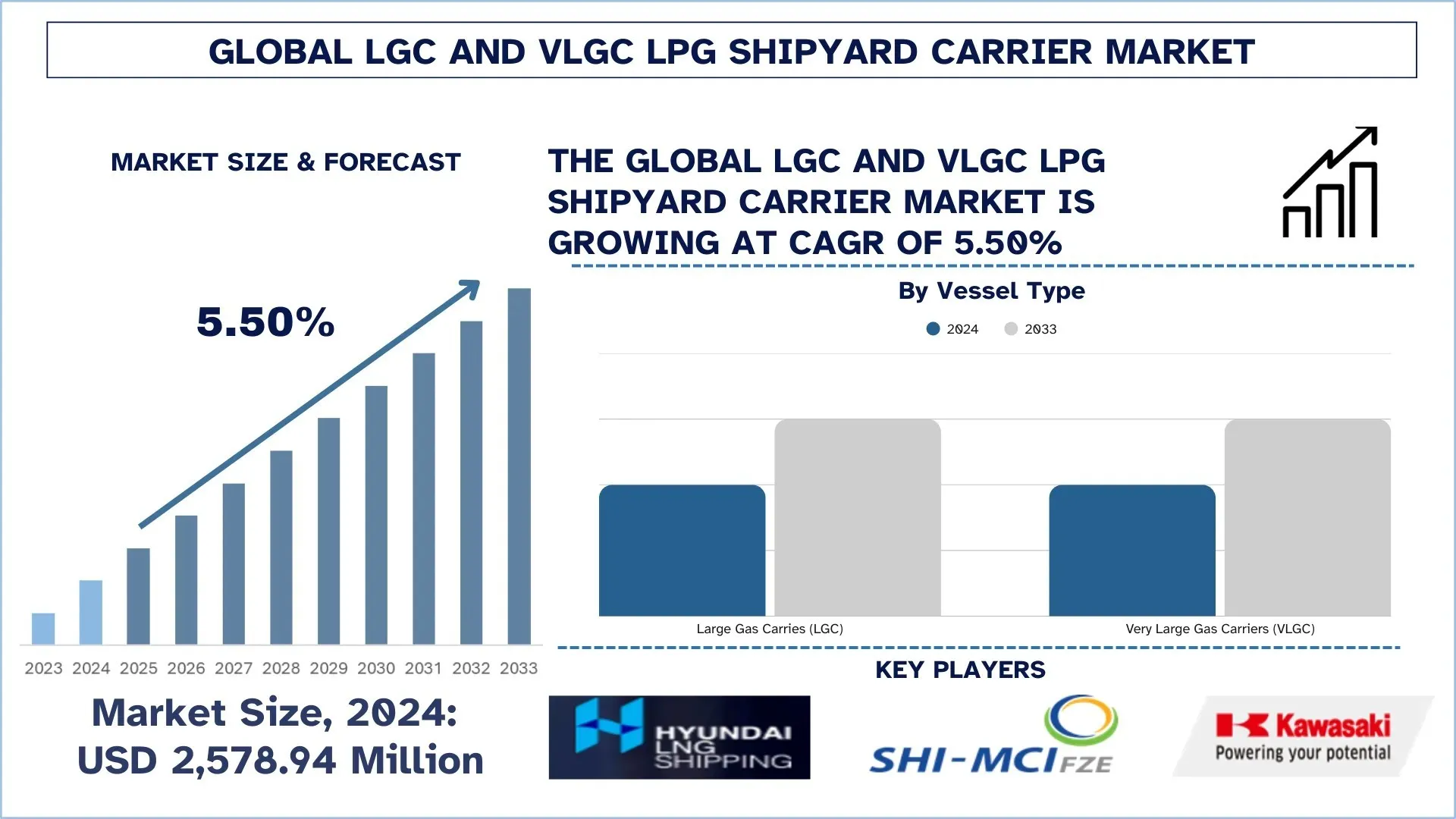

Global LGC and VLGC LPG Shipyard Carrier Market Size & Forecast

The global LGC and VLGC LPG shipyard carrier market was valued at USD 2,578.94 million in 2024 and is expected to grow at a strong CAGR of around 5.50% during the forecast period (2025-2033F), driven by rising LPG trade volumes, stricter IMO emission standards, and the adoption of dual-fuel propulsion systems.

LGC and VLGC LPG Shipyard Carrier Market Analysis

The LGC and VLGC shipyard carriers market is an industry that focuses on designing and manufacturing large and very large fleets that are used for the transportation of liquefied petroleum gas (LPG). The increase in production and manufacturing of shale gas, along with investment in export terminals and partnerships among energy producers and companies, is fueling the growth of the market. Additionally, increasing reliance on energy sources for production and consumption, and the demand for medium-sized carriers that enhance cost-effectiveness and improve route adaptability, is further driving the growth of the market. Moreover, the rigid guidelines for the consumption of green fuel made by the International Marine Organisation (IMO) for the promotion of green fuel encourage owners and manufacturers to integrate a dual-fuel system into their fleets, hence supporting the global market growth.

Global LGC and VLGC LPG Shipyard Carrier Market Trends

This section discusses the key market trends that are influencing the various segments of the global LGC and VLGC LPG shipyard carrier market, as found by our team of research experts.

Rise in Global LPG Trade Volume

The rise in global LPG trade volume is one of the prominent trends in the LGC and VLGC LPG shipyard carrier market, due to increasing energy demand from all over the world. This is boosting the imports of LPG for residential, industrial, and transportation purposes. Countries such as China, India, and Japan are expanding their reliance on LPG as a cleaner fuel alternative to coal and oil, driving demand for large-scale shipments. At the same time, exporters like the United States and Middle Eastern nations are enhancing their infrastructure to handle higher export capacities, supported by strong shale gas production and competitive pricing. The increasing development of export and import terminal infrastructure and vessel innovations further strengthens global trade flows.

LGC and VLGC LPG Shipyard Carrier Industry Segmentation

This section provides an analysis of the key trends in each segment of the global LGC and VLGC LPG shipyard carrier market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Very Large Gas Carriers (VLGC) Segment Dominates the Global LGC and VLGC LPG Shipyard Carrier Market

Based on vessel type, the LGC and VLGC LPG shipyard carrier market is segmented into large gas carriers (LGC) and very large gas carriers (VLGC). In 2024, the very large gas carriers (VLGC) dominated the market as they are commercially preferred by ship operators and owners due to their ability to carry a large amount of cargo more efficiently across long routes, saving time and transportation costs. VLGCs offer a lower per-ton LPG shipping cost compared to LCG. However, LGC is expected to show the fastest growth in the future. With the increasing demand for LPG as a marine fuel in the new trade routes, medium-sized vessels are in more demand, which is further driving the growth of the LGC segment.

The Medium-Sized Carriers (Between 50,000 – 100,000 cubic meters) Segment Dominates the Global LGC and VLGC LPG Shipyard Carrier Market.

Based on capacity, the LGC and VLGC LPG shipyard carrier market is segmented into small-sized carriers (below 50,000 cubic meters), medium-sized carriers (between 50,000 to 100,000 cubic meters), and large-sized carriers (more than 100,000 cubic meters). The medium-sized carriers dominated the market, as it is suitable for both long routes and short trade routes. Moreover, some medium-sized carriers are semi-refrigerated, which enables them to carry LPG and other petrochemicals, thereby increasing their commercial utility. However, due to the expansion of international trade between the US and Asia-Pacific countries, the large-sized carriers (more than 100,000 cubic meters) are showing the fastest growth.

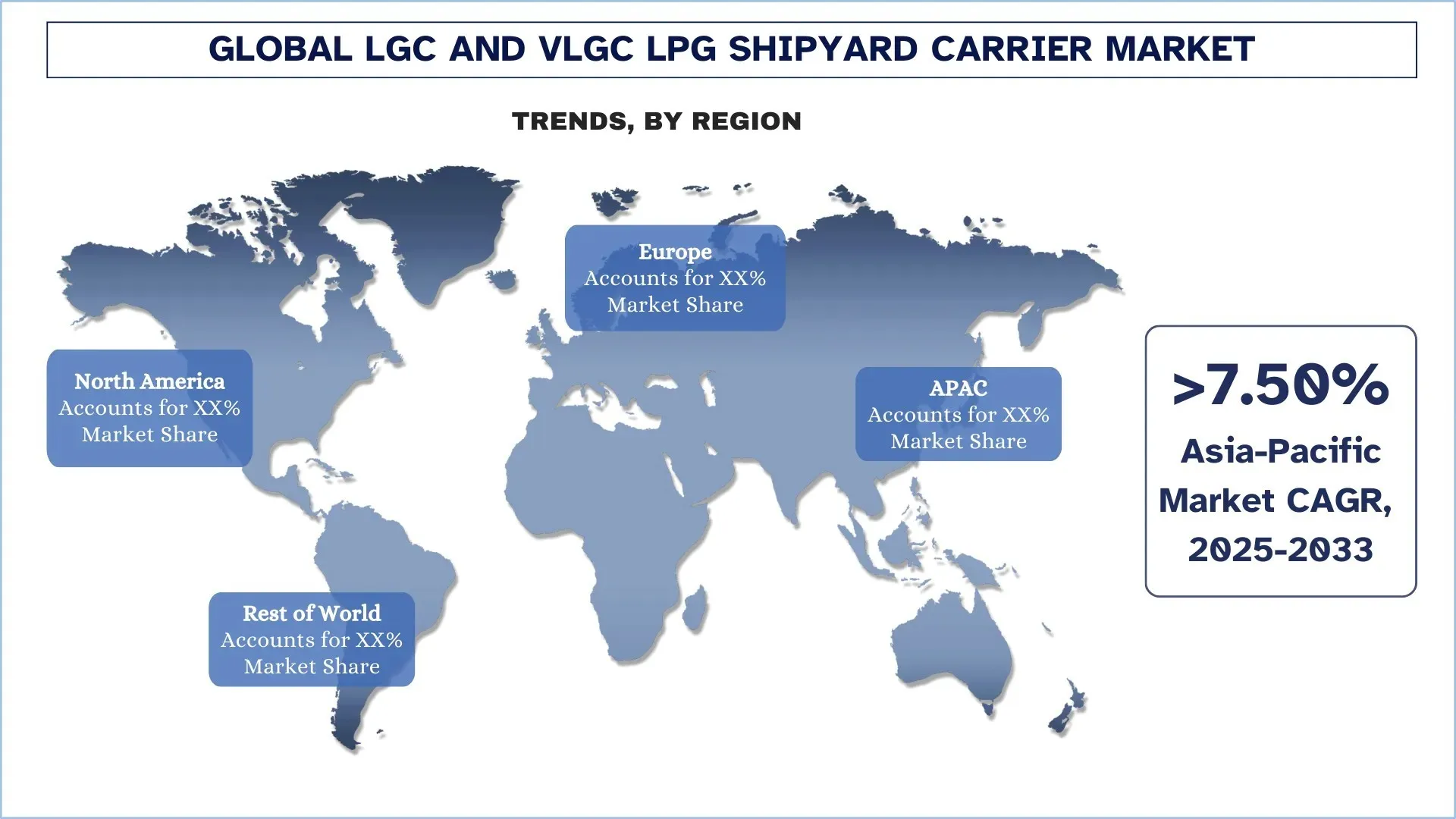

North America holds the largest market share in the global LGC and VLGC LPG Shipyard Carrier market

North America holds the largest share of the LGC and VLGC shipyard carrier market due to the rising demand for clean fuels for consumption and production in the region. Strategic investments in export infrastructure, increasing shale gas production, and partnerships between companies are further driving its market growth. For instance, in February 2025, ONEOK, Inc. and MPLX LP announced a partnership to build an export terminal in Texas City for handling 400,000 barrels of LPG per day. Such a partnership boosts the demand for LGC and VLGC by increasing the export volume and encouraging the use of a dual-propulsion system fleet, thereby driving the market growth.

U.S. held a Dominant share of the North America LGC and VLGC LPG Shipyard Carrier Market in 2024

The USA leads the LGC and VLGC LPG shipyard carrier market, as the region is the largest producer and manufacturer of clean fuels such as LPG and natural gas. Strong export infrastructure and growing partnerships among companies are further driving the market growth in this country. Technological advancements in the U.S. for drilling and shale gas extraction have increased oil and gas extraction, leading to a rise in the manufacturing of LPG. Additionally, factors such as Panama Canal congestion force U.S. VLGCs to take longer routes via the Cape of Good Hope, increasing ton-mile demand and freight rates, leading to further growth in the demand for LGC and VLGC LPG shipyard carriers in the U.S. market.

LGC and VLGC LPG Shipyard Carrier Industry Competitive Landscape

The global LGC and VLGC LPG shipyard carrier market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, geographical expansions, and mergers and acquisitions.

Top LGC and VLGC LPG Shipyard Carrier Market Companies

Some of the major players in the market are HLS CO., LTD., Samsung Heavy Industries Co., Ltd., Kawasaki Heavy Industries, Ltd., Mitsubishi Heavy Industries, Ltd., BW LPG, Dorian LPG (USA) LLC, EXMAR NV, StealthGas Inc., K Shipbuilding Co., Ltd., and HD Hyundai

Recent Developments in the LGC and VLGC LPG Shipyard Carrier Market

In April 2025, BW LPG India announced the construction of the country’s largest LPG import terminal at Mumbai, Jawaharlal Nehru Port. The terminal will be able to offload the latest fourth-generation VLGC in a single discharge operation. Thereby, strengthen India’s energy infrastructure by reducing dependency on small carriers, and making LPG importation faster and cost-effective.

In September 2025, HD Hyundai, a Korean-based shipping manufacturing firm, unveils its environmentally friendly dual-fuel gas vessel design, ready to consume future fuel as well, thereby providing high energy efficiency and producing less harmful gases. By preparing future-proof fuels, HD Hyundai is positioning itself as a leader in sustainable shipbuilding, catering to the rising demand from global shipping companies for eco-friendly vessels.

In July 2024, Kumiai Navigation placed another order for a dual-fuel, ammonia-ready VLGC with Kawasaki Heavy Industries for a seven-year lease, which means that the company will operate it for the next seven years. This highlights how companies are strategically investing in future technologies, and contributing in the development of the LGC and VLGC shipyard carrier market.

Global LGC and VLGC LPG Shipyard Carrier Market Report Coverage

Details | |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 5.50% |

Market size 2024 | USD 2,578.94million |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | The Asia-Pacific region is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, India, and South Korea |

Companies profiled | HLS CO., LTD., Samsung Heavy Industries Co., Ltd., Kawasaki Heavy Industries, Ltd., Mitsubishi Heavy Industries, Ltd., BW LPG, Dorian LPG (USA) LLC, EXMAR NV, StealthGas Inc., K Shipbuilding Co., Ltd., and HD Hyundai |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Vessel Type, By Capacity, By End-Use, By Refrigeration & Pressurization, and By Region/Country |

Reasons to Buy the LGC and VLGC LPG Shipyard Carrier Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional level analysis of the industry.

Customization Options:

The global LGC and VLGC LPG shipyard carrier market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global LGC and VLGC LPG Shipyard Carrier Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global LGC and VLGC LPG shipyard carrier market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the LGC and VLGC LPG shipyard carrier value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global LGC and VLGC LPG shipyard carrier market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including vessel type, capacity, end-use, refrigeration & pressurization, and region within the global LGC and VLGC LPG shipyard carrier market.

The Main Objective of the Global LGC and VLGC LPG Shipyard Carrier Market Study

The study identifies current and future trends in the global LGC and VLGC LPG shipyard carrier market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current and forecast market size of the global LGC and VLGC LPG shipyard carrier market and its segments in terms of value (USD).

LGC and VLGC LPG Shipyard Carrier Market Segmentation: Segments in the study include areas of vessel type, capacity, end-use, refrigeration & pressurization, and region.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the LGC and VLGC LPG shipyard carrier industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the LGC and VLGC LPG shipyard carrier market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global LGC and VLGC LPG shipyard carrier market’s current market size and growth potential?

As of 2024, the global LGC and VLGC LPG shipyard carrier market is valued at USD 2,578.94 million. The market is projected to expand at a CAGR of 5.50% from 2025 to 2033, driven by rising LPG trade volumes, stricter IMO emission standards, and the adoption of dual-fuel propulsion systems.

Q2: Which segment has the largest share of the global LGC and VLGC LPG shipyard carrier market by vessel type category?

The Very Large Gas Carrier (VLGC) segment dominates the market due to its ability to transport large LPG volumes cost-effectively across long-haul international routes. VLGCs provide lower freight rates per ton, higher fuel efficiency, and dual-fuel capability, making them the preferred choice for shipowners and charterers expanding their global fleets.

Q3: What are the driving factors for the growth of the global LGC and VLGC LPG shipyard carrier market?

Top growth drivers of the LGC and VLGC LPG shipyard carrier market include:

• Growing demand for green fuels such as LPG and LNG to meet IMO emission standards.

• Increasing shale gas production, particularly in North America, is boosting LPG export volumes.

• Expansion of port infrastructure and import/export terminals, enabling higher adoption of VLGCs globally.

Q4: What are the emerging technologies and trends in the global LGC and VLGC LPG shipyard carrier market?

Emerging trends in the LGC and VLGC LPG shipyard carrier market include:

• A surge in global LPG trade volumes between the U.S., Asia, and Europe.

• Adoption of dual-fuel and ammonia-ready propulsion systems that improve energy efficiency.

• Digital fleet monitoring, AI-driven ship design, and automation for operational optimization.

• These innovations are redefining competitiveness in the LGC and VLGC market by making vessels more sustainable, cost-efficient, and future-fuel ready.

Q5: What are the key challenges in the global LGC and VLGC LPG shipyard carrier market?

Key challenges in the LGC and VLGC LPG shipyard carrier market include:

• High capital investment is required for building eco-friendly, large-capacity carriers.

• Volatility in raw material prices that impact shipbuilding costs.

• Regulatory compliance costs associated with IMO’s stricter emission guidelines.

Q6: Which region dominates the global LGC and VLGC LPG shipyard carrier market?

North America dominates the market, supported by strong LPG production from shale gas, extensive export infrastructure, and strategic shipping partnerships. The U.S. is the world’s largest exporter of LPG, fueling the demand for VLGCs that connect North America with high-consumption markets in Asia and Europe.

Q7: Who are the key competitors in the global LGC and VLGC LPG shipyard carrier market?

Top players in the LGC and VLGC LPG shipyard carrier industry include:

• HLS CO., LTD.

• Samsung Heavy Industries Co., Ltd.

• Kawasaki Heavy Industries Ltd.

• Mitsubishi Heavy Industries Ltd.

• BW LPG

• Dorian LPG (USA) LLC

• EXMAR NV

• StealthGas Inc.

• K Shipbuilding Co., Ltd.

• HD Hyundai

Q8: What investment opportunities exist in the global LGC and VLGC LPG shipyard carrier market?

Investors can capitalize on rising demand for eco-friendly dual-fuel carriers, expansion of LPG trade routes, and new infrastructure projects in Asia and the Middle East. Additionally, retrofitting older fleets with LPG-ready propulsion systems offers significant cost-effective opportunities.

Q9: How are regulatory policies, such as IMO emission standards, impacting the LGC and VLGC LPG shipyard carrier market?

IMO’s stricter emission norms are driving shipowners to adopt green fuels and dual-fuel propulsion systems. This is accelerating demand for new-build construction and retrofit projects, creating growth avenues for shipyards and operators that prioritize compliance and sustainability.

Related Reports

Customers who bought this item also bought

India Decarbonization HVAC Market: Current Analysis and Forecast (2026-2034)

Emphasis on Product Type (Heating Equipment, Ventilation Equipment, Air Conditioning Equipment, Others); Decarbonization Type (Direct, Indirect); Capacity (Up to 5 Tons, 5-20 Tons, Above 20 Tons); End User (Commercial Buildings, Residential Buildings, Industrial Facilities, Healthcare Facilities, Data Centers, Others); and Region/States

Midstream Oil & Gas Filtration Market: Current Analysis and Forecast (2026-2034)

Emphasis on Filter Technology (Coalescer Filters, Cartridge Filters, Mechanical Filters, Bag Filters, Particulate Filters, Activated Carbon Filters, Strainers, and Others); by Application (Gas Processing Plants, Compression Stations, Storage And Distribution, Pipeline Transportation, LNG Processing, and Others); by Filtration Stage (Oil Filtration and Gas Filtration), by End User (Refineries and Petrochemical Industry), and Region/Country

Hydrogen-Powered Hospital Backup Systems Market: Current Analysis and Forecast (2026-2034)

Emphasis on System Type (Portable, Stationary, Hybrid); Power Capacity (Below 100 kW, 100–500 kW, and Above 500 kW); End-User (Public Hospitals, Private Hospitals, Specialty Hospitals, and Emergency Care Facilities); and Region/Country

Wind LiDAR Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Vertical Profiling Wind LiDAR, Ground-Based Wind LiDAR, Nacelle-Mounted Wind LiDAR, Airborne Wind LiDAR, and Others); Component (Sensor, Navigator, Laser, and Others); Location (Onshore and Offshore); Application (Wind Power, Meteorology & Environment, and Aviation); and Region/Country