Glass Battery Market: Current Analysis and Forecast (2025-2033)

Emphasis on Type (Solid-State Glass Battery, Lithium Glass Battery, and Sodium Glass Battery); Component (Electrolytes and Separators); Application (Consumer Electronics, Electric Vehicles, Energy Storage, Medical Devices, and Others); and Region/Country

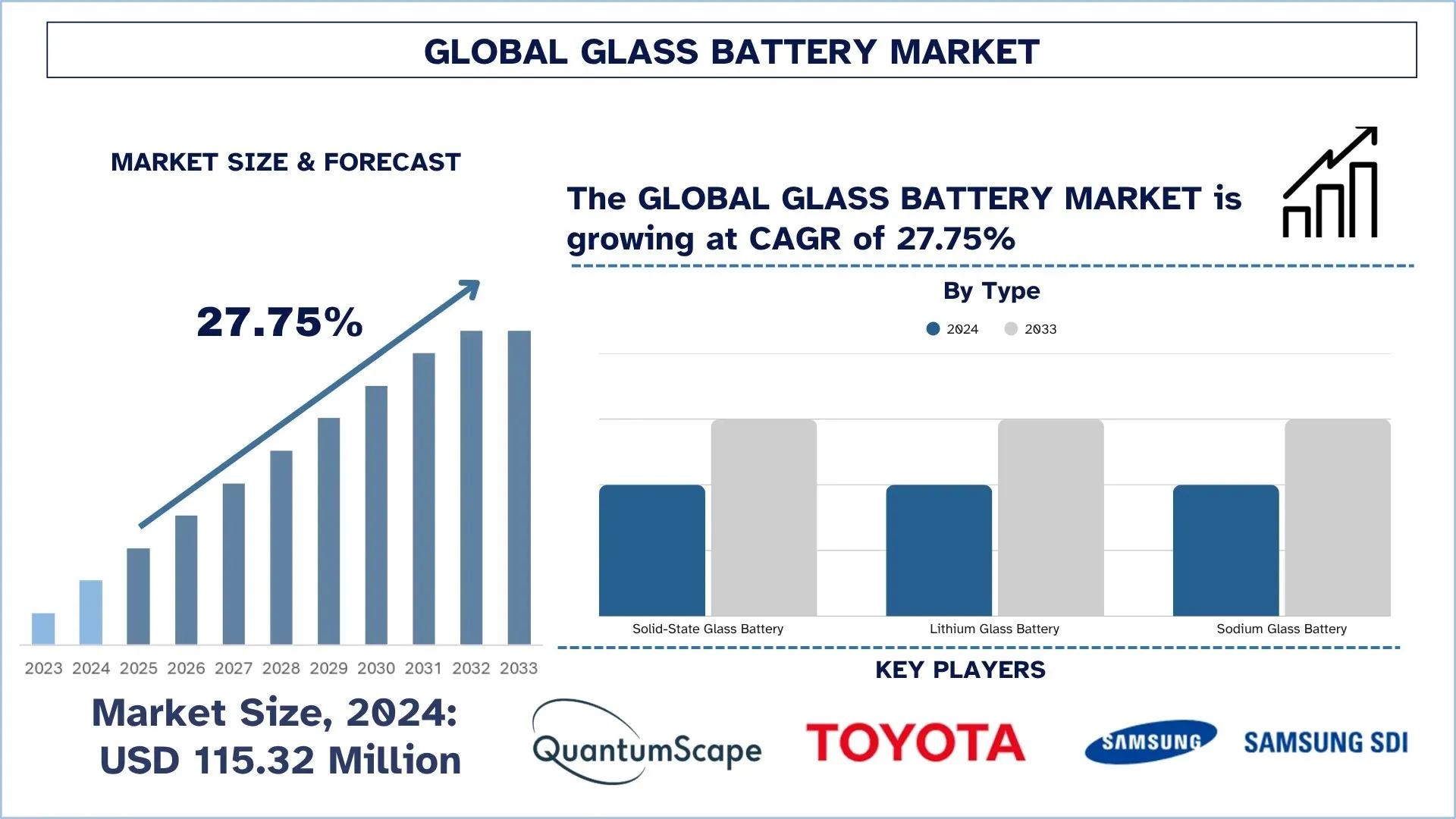

Global Glass Battery Market Size & Forecast

The Global Glass Battery Market was valued at USD 115.32 million in 2024 and is expected to grow at a CAGR of around 27.75% during the forecast period (2025-2033F), driven by the government push for clean energy solutions, escalating demand for portable and efficient consumer electronics, and the increasing demand for electric vehicles.

Glass Battery Market Analysis

The glass battery market is growing at the rate of knots, with an increased number of customers insisting on safer, longer-lasting, and more rapidly charging energy storage options. The solid-state glass electrolyte used in batteries offers a higher energy density, faster charging, and temperature stability than standard lithium-ion. They are non-flammable, thus suitable for electric vehicle applications, aerospace systems, and consumer electronics where safety and strength are imperative. The glass batteries are also more sustainable, as they are capable of handling more charging cycles and consume less toxic material, which is common and abundant. Major manufacturers operating in the industry are scaling up production processes and generating prototypes of advanced mobility as governments accelerate cleaner technologies and safer battery production. Glass batteries are far superior in terms of their performance, safety, and environmental advantages, making them primed to become the next innovation in the transportation, electronics, and energy storage market.

Global Glass Battery Market Trends

This section discusses the key market trends that are influencing the various segments of the global glass battery market, as found by our team of research experts.

Technological Advancements in Solid-State Electrolyte Materials

Glass batteries use an amorphous solid-state electrolyte, which combines the liquid‑like properties of ion transport with the robustness of ceramics. Following 2023, attention focused on chloride, oxy-halide, and sulfide glasses with an open structure and polarized anions, which provide extensive diffusion paths for Li+ or Na+. Crystallization is now prevented by nanoparticle seeding and aliovalent doping, and the 25 °C conductivities are increased, up to beyond 0.1 S cm 1, and f n increases. The most significant advances, however, are the creation of meter-scale roll-to-roll castable films via melt-quenching or ball-milling, minimization of space-charge resistance (by graded interfaces and elastic buffer layers), and the accompanying ability to use separators of thickness below 20 µm and anodeless stacks. These breakthroughs reduce impedance, increase power, and address the manufacturability and safety bottlenecks that previously hindered the development of glass batteries, with early commercial prototypes now shipping watt-hour-sized units. For example, in 2024, Osaka Metropolitan University presented an amorphous sodium oxy-chloride glass, Na2O · 25TaCl4 · 75O1 ·25; nanoparticle embedding raises the room-temperature conductivity to 1.3 × 10^1 S cm^1, and its ductility makes it suitable for scaling up to tape casting in next-generation solid-state sodium cells.

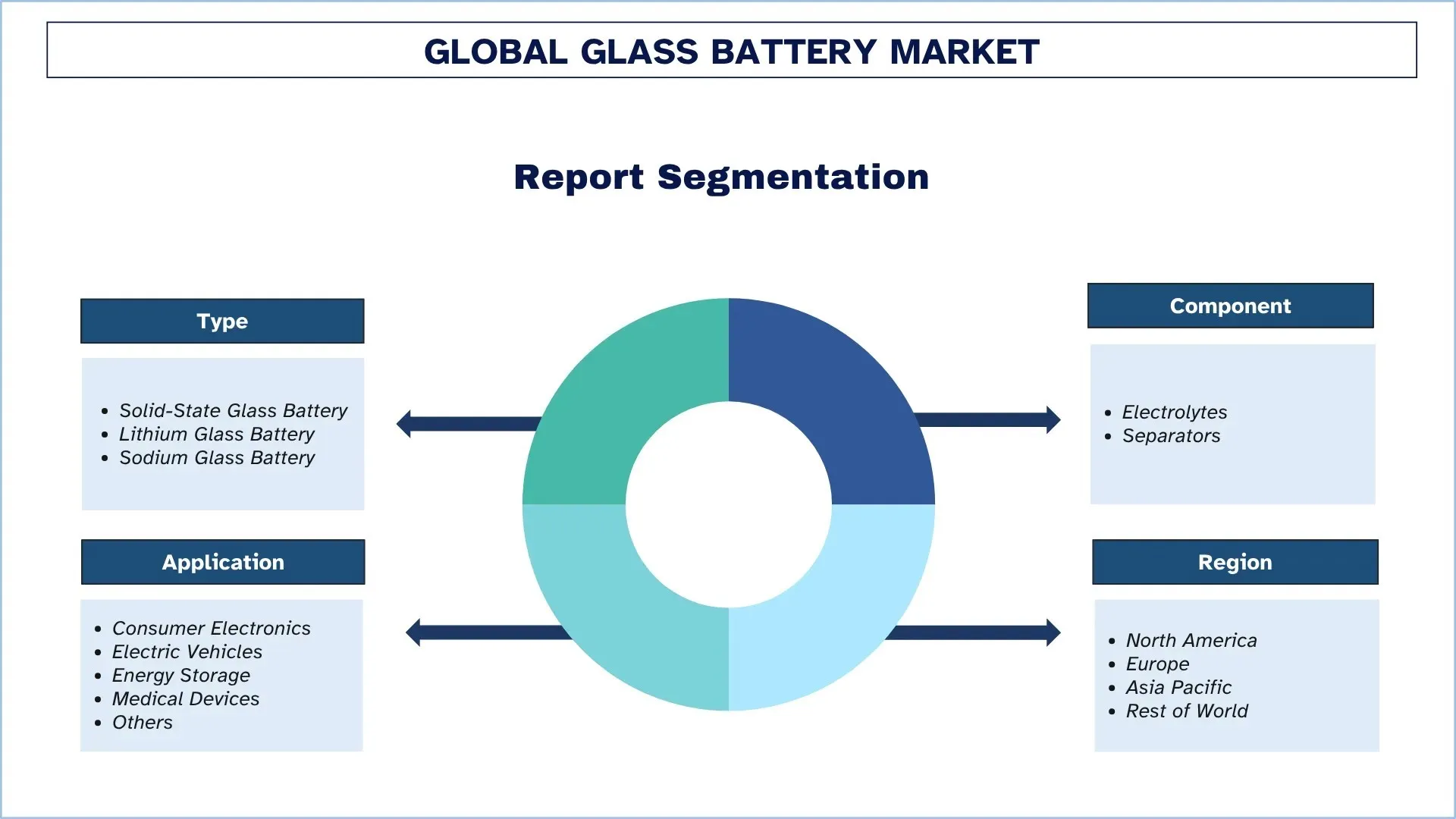

Glass Battery Industry Segmentation

This section provides an analysis of the key trends in each segment of the global glass battery market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Solid-State Battery Market Dominates the Glass Battery Market

Based on type, the glass battery market is segmented into Solid-State Glass Battery, Lithium Glass Battery, and Sodium Glass Battery. In 2024, the Solid-State Glass Battery segment dominated the market and is anticipated to continue its leadership throughout the forecast period. The superior performance of electric vehicles, consumer electronics, and aerospace applications has increased the demand for solid-state glass batteries, driven by their enhanced safety, thermal stability, and energy density. Since this type of device replaces the flammable liquid components with solid-state glass electrolytes, fire concerns are mitigated, and they can operate at higher voltages. With energy storage needed to be more efficient, compact, and durable than ever in industries, the solid-state glass technology stands out as the one that achieves it with faster charging potential and thousands of charging cycles without significant depreciation. Innovative manufacturing processes, such as scalable production processes and thin-film design, allow easy adaptation to miniaturized or high-performance applications. The automobiles, specifically, benefit because of lightweight, thermally stable battery packs that increase the range as well as safety. As an increasing focus is placed on sustainability and energy efficiency, the use of solid-state glass batteries is expected to gain momentum in various industries, making them a viable solution for a sustainable energy and electrification future.

The Electrolytes held the Largest Market Share in the Glass Battery Market.

Based on components, the glass battery market is segmented into Electrolytes and Separators. In 2024, the electrolytes segment held the largest share and is expected to remain at the top for the next few years. Glass electrolytes made of glass are now considered with a lot of potential, due to their potential to push batteries to new heights in terms of safety, efficiency, and durability. Unlike conventional liquid electrolytes, they can be non-flammable by their design, they enable higher voltages to be achieved, and they significantly eliminate the risk of thermal runaway, making glass electrolytes particularly well-suited to high-stakes applications like electric vehicles, aviation, and consumer electronics. The glass electrolytes are also used to make batteries thinner and smaller in dimensions with high energy density, something that perfectly fits the packaging goals in the industry towards lightweight and long-lasting power sources. Besides, the introduction of lithium and sodium-based glass electrolytes provides high-performance and low-cost applications. They are also much more versatile in the variety of battery architectures they can be used in, as well as their relative ease of integration with other solid-state systems, which makes them more appealing. As pressure mounts for safer and more efficient energy storage, the electrolyte component will remain one of the crucial catalysts driving innovation and growth within the glass battery industry.

North America Dominated the Global Glass Battery Market

North America currently leads the glass battery market and is expected to maintain its dominance during the forecast period. The collaboration between the emergence of state-of-the-art development and research avenues, a rapidly growing electric vehicle (EV) sector, and strong government support to clean energy projects primarily powers leadership in this sector. In the United States, some of these companies and startups are at the forefront of developing solid-state and glass battery technology. The commercialization of next-generation batteries has been accelerated by federal incentives under the Inflation Reduction Act as well as an investment by the Department of Energy. At the same time, the robust automotive and aerospace industries are increasingly turning to lightweight, high-performance, and thermally stable battery technologies, which makes glass batteries an even more viable prospect. The presence of national and international leaders in the manufacturing of semiconductors and electronics in the United States and Canada also drives the high-volume demand for compact and reliable energy storage systems. Battery safety, energy density, and environmental compliance commitments show that the North American market will continue at the forefront of creating innovation and ramping up the introduction of glass batteries into EVs, consumer electronics, medical equipment, and renewable energy storage systems.

U.S. held a dominant Share of the North America Glass Battery Market in 2024

The US is becoming a powerhouse in the global glass battery industry, driven forward by ambitious federal policies, including the Bipartisan Infrastructure Law, the Inflation Reduction Act, and the EVs4ALL program at ARPA-E. Venture capital and national lab talent are funneled through innovation corridors extending eastward, from Silicon Valley and Austin to Detroit and Boston, at scale-ups using solid-state systems. The Department of Energy's Loan Programs Office funds the construction of new gigafactories and precursor plants. The EV market of the U.S. is growing fast, which creates a need to find safer, longer-lasting, energy-efficient battery cells, making glass batteries with their solid ion conductors, high heat resistance, and high energy density a potentially technological future.

Glass Battery Industry Competitive Landscape

The global glass battery market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top Glass Battery Manufacturing Companies

Some of the major players in the market are QuantumScape Corporation, Toyota Motor Corporation, SAMSUNG SDI, Solid Power Inc., Ilika, Hydro-Québec, Nippon Electric Glass Co., Ltd., AGC Inc., Factorial Inc., and Ensurge Micropower ASA.

Recent Developments in the Glass Battery Market

In 2025, during the first quarter (Q1), the total sales of electric vehicles reached 4.1 million units, with a notable increase of 29%, compared to the same period last year.

In July 2025, Lyten, an enterprise based in Silicon Valley, announced a transaction to buy the Northvolt facility in Poland, a Dwa energy-storage-system plant located in Gdańsk, the biggest European BESS factory in Europe. The 25,000 m² site, starting in 2023 and closed after Northvolt's bankruptcy in March 2025, consists of enough equipment to produce up to 6 GWh of electricity per annum and has spare capacity to grow to 10 GWh. Lyten will restart production, retrofit the line with its glass-ceramic lithium-sulfur cells, and commence delivery of what it terms the first Li-S powered BESS in the world, with over USD 200 million in new funding to complete the transaction in Q3 2025.

Global Glass Battery Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 27.75% |

Market size 2024 | USD 115.32 Million |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | North America is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, South Korea, and India |

Companies profiled | QuantumScape Corporation, Toyota Motor Corporation, SAMSUNG SDI, Solid Power Inc., Ilika, Hydro-Québec, Nippon Electric Glass Co., Ltd., AGC Inc., Factorial Inc., and Ensurge Micropower ASA. |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Type; By Component; By Application; By Region/Country |

Reasons to Buy Glass Battery Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional-level analysis of the industry.

Customization Options:

The global glass battery market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global Glass Battery Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global glass battery market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the glass battery value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global glass battery market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including type, component, application, and regions within the global glass battery market.

The Main Objective of the Global Glass Battery Market Study

The study identifies current and future trends in the global glass battery market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current market size and forecast the market size of the global glass battery market and its segments in terms of value (USD).

Glass Battery Market Segmentation: Segments in the study include areas of type, component, application, and regions.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the glass battery industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the glass battery market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global glass battery current market size and its growth potential?

The global glass battery market was valued at USD 115.32 million in 2024 and is expected to grow at a CAGR of 27.75% during the forecast period (2025-2033).

Q2: Which segment has the largest share of the global glass battery market by type?

The solid-state glass battery segment dominated the market and is expected to maintain its leadership throughout the forecast period, driven by the growing demand in electric vehicles, consumer electronics, and aerospace applications.

Q3: What are the driving factors for the growth of the global glass battery market?

• Government Push for Cleaner Energy Solutions: Government incentives, emissions targets, and generous funding accelerate R&D, pilot lines, and domestic production of non‑flammable, high‑energy glass batteries, positioning them as cornerstone technologies in national decarbonization strategies.

• Escalating Demand for Portable and Efficient Consumer Electronics: Consumers demand lighter gadgets with longer runtimes and faster charging; glass batteries provide superior energy density, safety, and cycle life, prompting OEMs to redesign smartphones and wearables around solid‑state power.

• Increasing Demand for Electric Vehicles: EV makers seek safer, higher‑range cells to satisfy buyers and regulators; glass solid‑state batteries raise energy density by ~20%, cut fire risk, and enable rapid charging, accelerating adoption.

Q4: What are the emerging technologies and trends in the global glass battery market?

• Technological Advancements In Solid‑State Electrolyte Materials: Breakthrough glassy chloride, oxy‑halide, and sulfide chemistries now achieve >0.1 S cm⁻¹ conductivity, ultra‑thin separators, and anodeless stacks, slashing impedance and unlocking scalable roll‑to‑roll manufacturing for high‑power cells.

• Lack of Widespread Commercial Production Facilities: Joint ventures pair OEM capital, vehicle platforms, and supply‑chain muscle with start‑ups’ proprietary glass‑electrolyte IP, accelerating prototype validation, de‑risking gigafactory investment, and synchronizing cell formats with next‑generation EV architectures.

Q5: What are the key challenges in the global glass battery market?

• High Production Cost: Glass solid‑state batteries rely on expensive precursor chemicals, precision thin‑film deposition, and stringent quality control; until economies of scale mature, unit costs remain multiples higher than conventional lithium‑ion packs.

• Lack of Widespread Commercial Production Facilities: Most current output stems from pilot lines and small batch fabs; limited throughput constrains supply, inflates lead times, and discourages downstream integration by automakers and consumer electronics giants.

Q6: Which region dominates the global glass battery market?

North America currently leads the glass battery market and is expected to maintain its dominance during the forecast period. The collaboration between the emergence of state-of-the-art development and research avenues, a rapidly growing electric vehicle (EV) sector, and strong government support to clean energy projects primarily powers leadership in this sector.

Q7: Who are the key players in the global glass battery market?

Some of the key companies include:

• QuantumScape Corporation

• Toyota Motor Corporation

• SAMSUNG SDI

• Solid Power Inc.

• Ilika

• Hydro-Québec

• Nippon Electric Glass Co., Ltd.

• AGC Inc.

• Factorial Inc.

• Ensurge Micropower ASA

Q8: What intellectual‑property strategies are companies using to secure and monetize glass‑battery breakthroughs?

Targeted Patenting: Firms are filing narrow, chemistry‑specific patents on glass electrolyte formulations, electrode interfaces, and roll‑to‑roll fabrication steps to block competitors while preserving trade secrets on process parameters.

Cross‑Licensing & Pools: Major players enter cross-license agreements or join patent pools to avoid litigation, accelerate standardization, and gain access to complementary IP such as high‑voltage cathode coatings.

Defensive Publishing: Start‑ups sometimes publish non‑critical know‑how to create prior art, preventing rivals from patenting incremental improvements and lowering overall IP risk.

Q9: How are supply‑chain partnerships evolving to secure critical inputs for glass‑battery production?

• Vertical Integration: Cell makers are acquiring or taking equity stakes in lithium‑ and sodium‑salt refineries, glass‑precursor producers, and thin‑film equipment vendors to lock in feedstock and tooling.

• Long‑Term Off‑Take Agreements: Multi‑year contracts with mining firms and specialty‑glass suppliers guarantee volume and price stability, enabling predictable scaling of gigafactory output.

• Regional Co‑Location: To shorten lead times, companies co‑locate separator casting, electrolyte sintering, and pack‑assembly plants near raw‑material sources and major EV or electronics hubs.

Related Reports

Customers who bought this item also bought

India Decarbonization HVAC Market: Current Analysis and Forecast (2026-2034)

Emphasis on Product Type (Heating Equipment, Ventilation Equipment, Air Conditioning Equipment, Others); Decarbonization Type (Direct, Indirect); Capacity (Up to 5 Tons, 5-20 Tons, Above 20 Tons); End User (Commercial Buildings, Residential Buildings, Industrial Facilities, Healthcare Facilities, Data Centers, Others); and Region/States

Midstream Oil & Gas Filtration Market: Current Analysis and Forecast (2026-2034)

Emphasis on Filter Technology (Coalescer Filters, Cartridge Filters, Mechanical Filters, Bag Filters, Particulate Filters, Activated Carbon Filters, Strainers, and Others); by Application (Gas Processing Plants, Compression Stations, Storage And Distribution, Pipeline Transportation, LNG Processing, and Others); by Filtration Stage (Oil Filtration and Gas Filtration), by End User (Refineries and Petrochemical Industry), and Region/Country

Hydrogen-Powered Hospital Backup Systems Market: Current Analysis and Forecast (2026-2034)

Emphasis on System Type (Portable, Stationary, Hybrid); Power Capacity (Below 100 kW, 100–500 kW, and Above 500 kW); End-User (Public Hospitals, Private Hospitals, Specialty Hospitals, and Emergency Care Facilities); and Region/Country

Wind LiDAR Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Vertical Profiling Wind LiDAR, Ground-Based Wind LiDAR, Nacelle-Mounted Wind LiDAR, Airborne Wind LiDAR, and Others); Component (Sensor, Navigator, Laser, and Others); Location (Onshore and Offshore); Application (Wind Power, Meteorology & Environment, and Aviation); and Region/Country