Merchant Hydrogen Market: Current Analysis and Forecast (2025-2033)

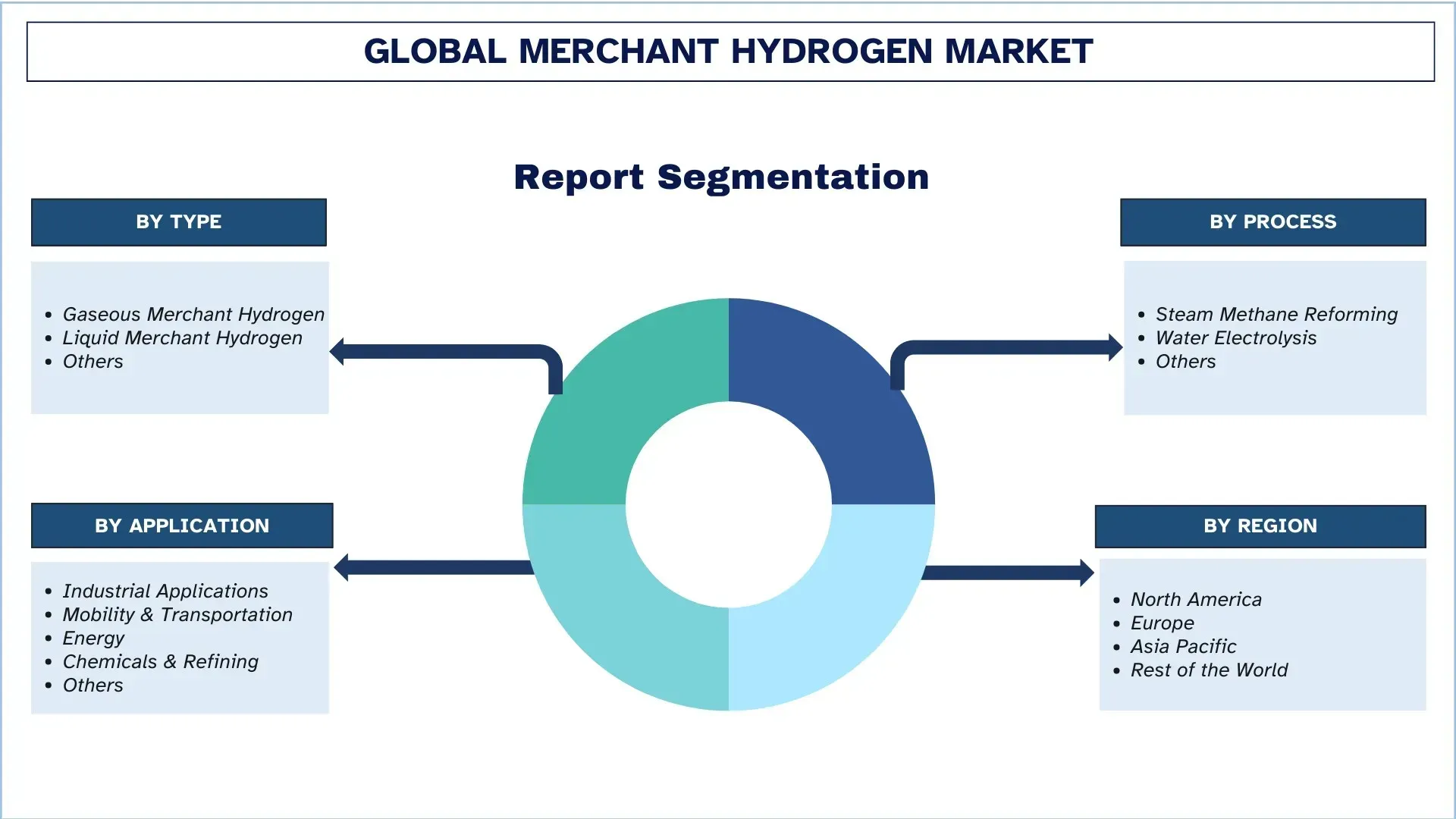

Emphasis on Type (Gaseous Merchant Hydrogen, Liquid Merchant Hydrogen, and Others); Process (Steam Methane Reforming, Water Electrolysis, and Others); Application (Industrial Applications, Mobility & Transportation, Energy, Chemicals & Refining, and Others); and Region/Country

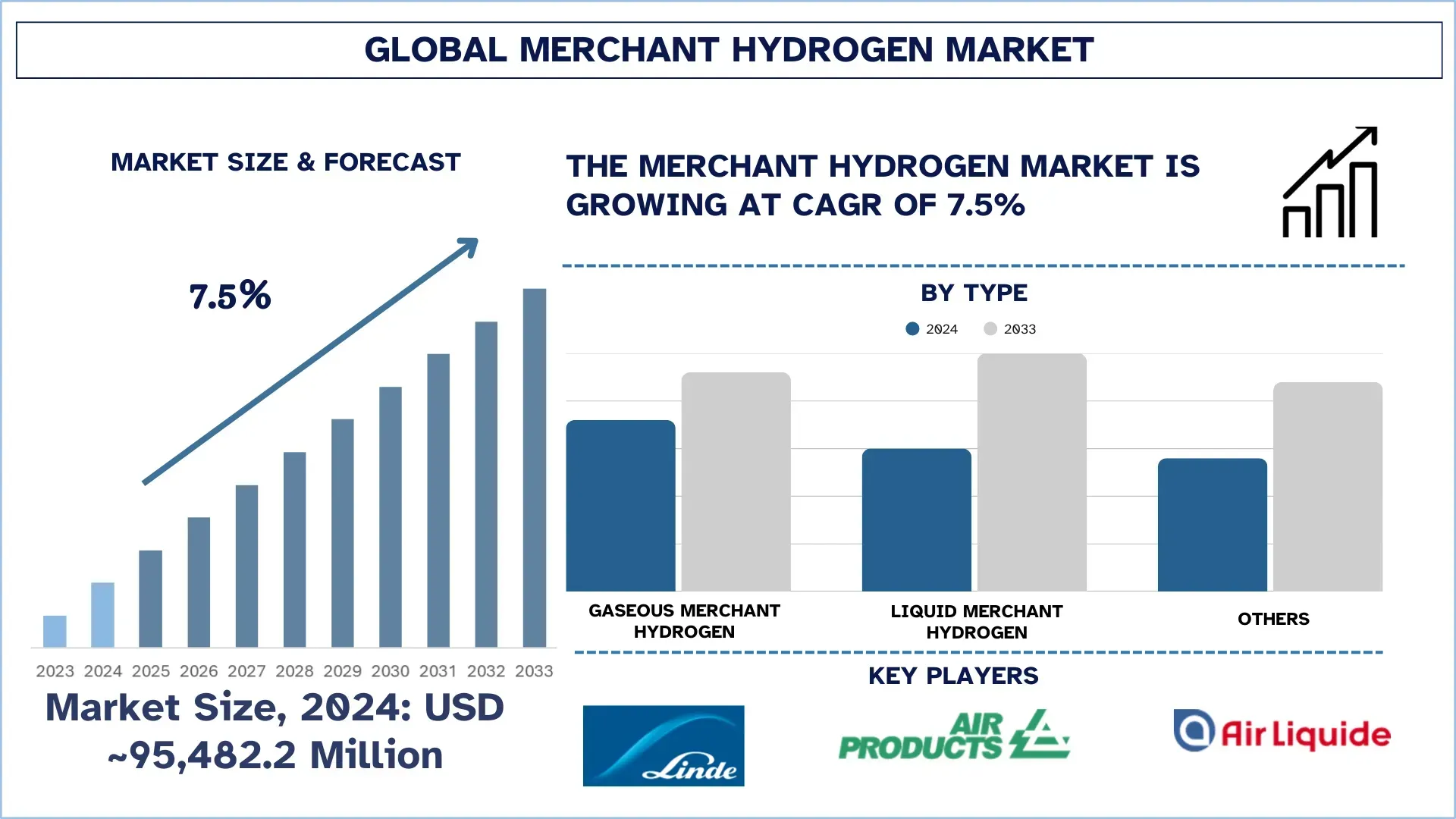

Global Merchant Hydrogen Market Size & Forecast

The Global Merchant Hydrogen Market was valued at USD ~95482.2 million in 2024 and is expected to grow at a strong CAGR of around 7.5% during the forecast period (2025-2033F), driven by growing demand for clean energy solutions, supported by global decarbonization targets and government incentives.

Merchant Hydrogen Market Analysis

Merchant hydrogen is hydrogen generated at central facilities and provided to external customers. It is usually delivered in gaseous or liquid form via pipelines, tube trailers, or cryogenic tankers for use by industries such as refining, chemicals, steelmaking, electronics, energy storage, and transportation. Merchant hydrogen can be manufactured through steam methane reforming, water electrolysis, or other mature processes and may be classified as grey, blue, or green based on its carbon footprint. The merchant hydrogen market is expanding as the world's demand for clean and sustainable energy solutions continues to grow due to concerns about climate change and the goal of achieving net-zero emissions. Governments around the world are introducing supportive policies, subsidies, and carbon reduction mandates, which have been driving industries to switch from fossil fuels to low-carbon hydrogen.

Global Merchant Hydrogen Market Trends

This section discusses the key market trends that are influencing the various segments of the global Merchant Hydrogen market, as found by our team of research experts.

Shift from Grey Hydrogen to low-carbon Blue and Green Hydrogen: The Latest Trend in the Merchant Hydrogen Market

One of the major trends in the merchant hydrogen market is the transition from grey hydrogen produced from fossil fuels without the removal of carbon to low-carbon blue and green hydrogen. Blue hydrogen utilizes carbon capture, utilization, and storage (CCUS) technologies to dramatically lower emissions, and green hydrogen is created through renewable-powered electrolysis with zero carbon emissions used during the process. This shift is fueled by global decarbonization goals, tighter emission standards, and increasing corporate sustainability commitments. Governments and industries are pouring assets into the integration of renewable energy, CCUS infrastructure, and large-scale electrolyzer deployment, making blue and green hydrogen key solutions towards a cleaner energy future.

Merchant Hydrogen Industry Segmentation

This section provides an analysis of the key trends in each segment of the global merchant hydrogen market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Gaseous Merchant Hydrogen Segment Dominates the Global Merchant Hydrogen Market

Based on the type category, the market is categorized into gaseous merchant hydrogen, liquid merchant hydrogen, and others. Among these, gaseous merchant hydrogen has the highest market share due to its widespread application in industrial processes such as refining, chemicals, and electronics, as well as its easier generation and distribution via compressed gas cylinders, tube trailers, and pipelines, without the need for energy-intensive liquefaction. However, the Liquid Merchant Hydrogen is expected to be the fastest-growing type because of its increased adoption in mobility and transportation.

The Chemicals & Refining Segment Dominates the Global Merchant Hydrogen Market.

Based on the application category, the market is segmented into industrial applications, mobility & transportation, energy, chemicals & refining, and others. Among these, chemicals & refining is the largest segment of the merchant hydrogen market as hydrogen is an important feedstock for petroleum refining (hydrocracking, desulphurization) and ammonia/methanol. This segment has a large proven demand base, underpinned by a large-scale pipeline and onsite supply infrastructure from merchant producers. However, Mobility & Transportation is anticipated to grow at the highest rate in the forecast period, owing to the global trend toward clean fuels and fast-paced development of hydrogen fuel cell vehicles (buses, trucks, trains, and ships).

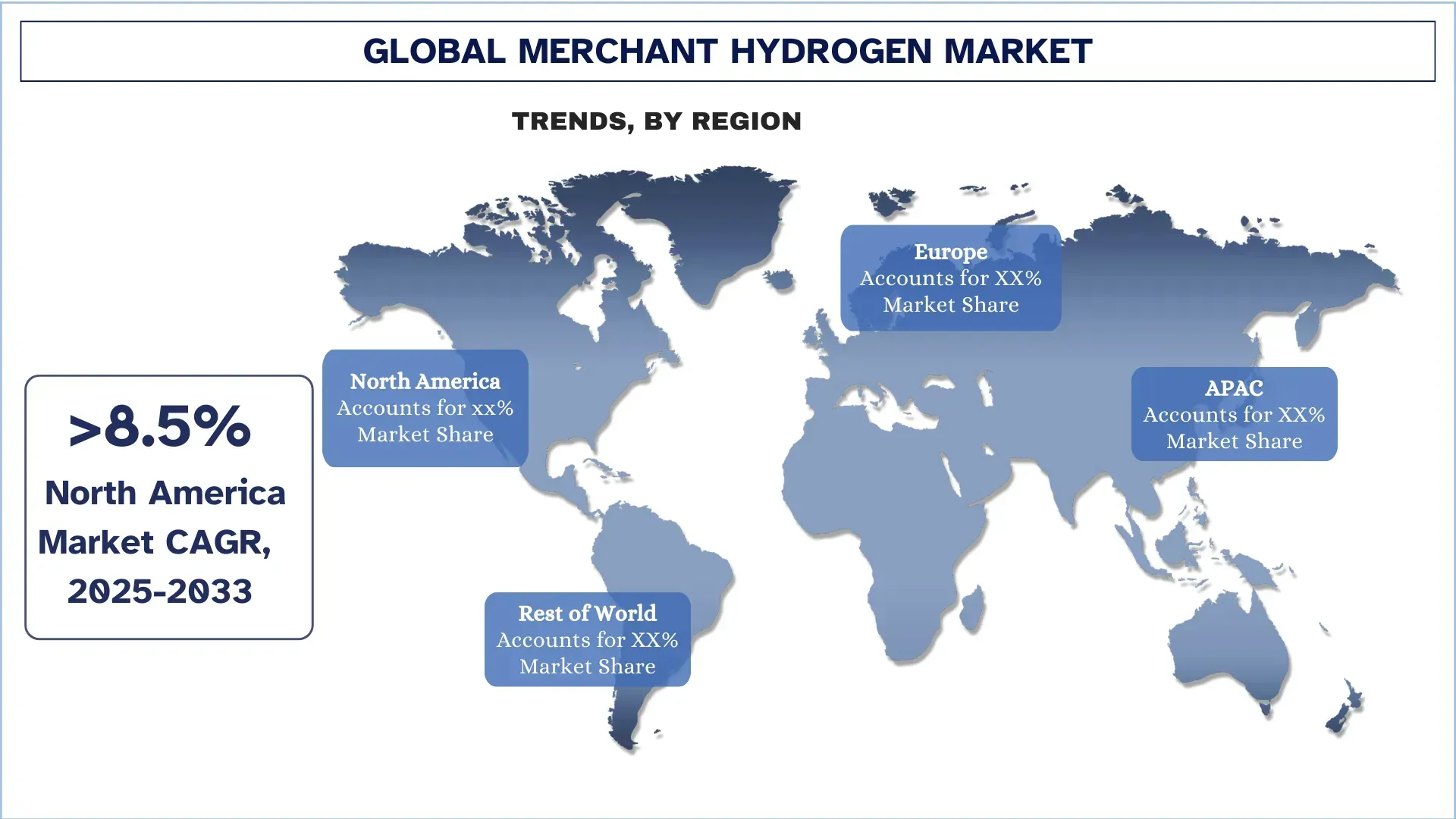

Asia-Pacific holds the largest market share in the global Merchant Hydrogen market

The Asia-Pacific region dominates the global merchant hydrogen market, owing to its strong industrial presence, high energy demand, and robust government policies and initiatives to support hydrogen manufacturing. Along with this, the region has substantial hydrogen demand in the refinery, chemicals, and steel industries, as well as growing use in fuel cell vehicles and power generation. With several hydrogen production capacities, infrastructure, and renewable-powered green hydrogen initiatives, the region continues to establish its dominance in the global market, positioning Asia-Pacific as a strategic center for hydrogen production, consumption, and technological advancements.

China held a Dominant share of the Asia-Pacific Merchant Hydrogen Market in 2024

China dominated the Asia-Pacific merchant hydrogen market in 2024, with its vast industrial demand, supportive government policies, and substantial investments in hydrogen infrastructure contributing to its significant position in the market. The country is moving forward with large-scale production projects, including both grey and green hydrogen, as a part of its decarbonization and energy security strategy. The rapid expansion of hydrogen refueling stations, especially in the public transport and heavy-duty vehicle markets, as well as integration into the refining, chemical, and steel-making industries, has further consolidated China's leading role in the market.

Merchant Hydrogen Industry Competitive Landscape

The global merchant hydrogen market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, geographical expansions, and mergers and acquisitions.

Top Merchant Hydrogen Market Companies

Some of the major players in the market are Linde Plc., Air Products and Chemicals, Inc., Air Liquide, FuelCell Energy, Inc., Coregas, Messer, Plug Power Inc., TotalEnergies, Uniper SE, and Iwatani Corporation.

Recent Developments in the Merchant Hydrogen Market

In December 2024, Axpo and its partners, through the joint venture H2Uri, broke ground on a second green hydrogen plant in Bürglen, central Switzerland. Powered by adjacent hydropower and supported by hydropower infrastructure, the 2 MW facility is expected to begin operations in 2026 and will supply clean hydrogen to power a passenger vessel on Lake Lucerne, among other applications, advancing Switzerland’s hydrogen transition.

In December 2023, Linde announced that it has increased the liquid hydrogen production capacity at its facility in McIntosh, Alabama. Linde’s McIntosh facility will now produce up to 30 tons per day of liquid hydrogen for the local merchant market. The plant will meet increasing demand for hydrogen from Linde’s existing and new customers in end markets including manufacturing and electronics. It will also supply hydrogen to Linde’s space launch and mobility customers.

Global Merchant Hydrogen Market Report Coverage

Details | |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 7.5% |

Market size 2024 | USD ~95,482.2 million |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | The North America region is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, and India. |

Companies profiled | Linde Plc., Air Products and Chemicals, Inc., Air Liquide, FuelCell Energy, Inc., Coregas, Messer, Plug Power Inc., TotalEnergies, Uniper SE, and Iwatani Corporation. |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Type, By Process, By Application, and By Region/Country |

Reasons to Buy the Merchant Hydrogen Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional level analysis of the industry.

Customization Options:

The Global Merchant Hydrogen Market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global Merchant Hydrogen Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global merchant hydrogen market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the merchant hydrogen value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global merchant hydrogen market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including type, process, application, and regions within the global merchant hydrogen market.

The Main Objective of the Global Merchant Hydrogen Market Study

The study identifies current and future trends in the global merchant hydrogen market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current and forecast market size of the global merchant hydrogen market and its segments in terms of value (USD).

Merchant Hydrogen Market Segmentation: Segments in the study include areas of type, process, application, and region.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the merchant hydrogen industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the merchant hydrogen market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global merchant hydrogen market’s current market size and growth potential?

As of 2024, the global merchant hydrogen market is valued at approximately USD ~95,482.2 million and is expected to grow at a CAGR of 7.5% from 2025 to 2033. This growth is fueled by rising demand for clean energy, international decarbonization commitments, and strong government incentives supporting hydrogen production and infrastructure expansion.

Q2: Which segment has the largest share of the global merchant hydrogen market by type category?

The gaseous merchant hydrogen segment holds the largest share of the global Merchant Hydrogen market, primarily due to its cost-effectiveness, easier storage and transportation, and widespread use in industrial applications such as refining and chemical manufacturing.

Q3: What are the driving factors for the growth of the global merchant hydrogen market?

Top growth drivers of the merchant hydrogen market include:

• Rising global demand for clean, sustainable energy solutions.

• Strong government incentives and subsidies for hydrogen production.

• Technological advancements are reducing production and distribution costs.

Q4: What are the emerging technologies and trends in the global merchant hydrogen market?

Emerging trends in the merchant hydrogen market include:

• A global shift from grey hydrogen to low-carbon blue and green hydrogen.

• Large-scale expansion of electrolyzer manufacturing capacity to support green hydrogen production.

Q5: What are the key challenges in the global merchant hydrogen market?

Key challenges in the merchant hydrogen market include:

• High cost of green hydrogen production compared to fossil-based hydrogen.

• Infrastructure, regulatory, and safety concerns related to hydrogen storage, handling, and transportation.

Q6: Which region dominates the global merchant hydrogen market?

The Asia-Pacific dominates the global merchant hydrogen market due to strong industrial demand, government-backed hydrogen strategies, and large-scale investments in hydrogen production and infrastructure.

Q7: Who are the key competitors in the global merchant hydrogen market?

Top players in the merchant hydrogen industry include:

• Linde Plc.

• Air Products and Chemicals, Inc.

• Air Liquide

• FuelCell Energy, Inc.

• Coregas

• Messer

• Plug Power Inc.

• TotalEnergies

• Uniper SE

• Iwatani Corporation

Q8: What are the investment opportunities in the global merchant hydrogen market?

Investment opportunities in the merchant hydrogen market span across green hydrogen production projects, hydrogen refueling infrastructure, storage and transportation solutions, and advanced electrolyzer technologies. With supportive government policies and increasing demand from industrial and mobility sectors, the market presents high-growth potential for strategic investors.

Q9: How are government policies and regulations influencing the merchant hydrogen market?

Government policies, such as tax credits, subsidies, carbon pricing, and renewable energy mandates, are accelerating hydrogen production and adoption. Regulatory frameworks are also shaping safety standards, infrastructure development, and certification schemes for low-carbon hydrogen, directly impacting market growth and investment strategies.

Related Reports

Customers who bought this item also bought

India Decarbonization HVAC Market: Current Analysis and Forecast (2026-2034)

Emphasis on Product Type (Heating Equipment, Ventilation Equipment, Air Conditioning Equipment, Others); Decarbonization Type (Direct, Indirect); Capacity (Up to 5 Tons, 5-20 Tons, Above 20 Tons); End User (Commercial Buildings, Residential Buildings, Industrial Facilities, Healthcare Facilities, Data Centers, Others); and Region/States

Midstream Oil & Gas Filtration Market: Current Analysis and Forecast (2026-2034)

Emphasis on Filter Technology (Coalescer Filters, Cartridge Filters, Mechanical Filters, Bag Filters, Particulate Filters, Activated Carbon Filters, Strainers, and Others); by Application (Gas Processing Plants, Compression Stations, Storage And Distribution, Pipeline Transportation, LNG Processing, and Others); by Filtration Stage (Oil Filtration and Gas Filtration), by End User (Refineries and Petrochemical Industry), and Region/Country

Hydrogen-Powered Hospital Backup Systems Market: Current Analysis and Forecast (2026-2034)

Emphasis on System Type (Portable, Stationary, Hybrid); Power Capacity (Below 100 kW, 100–500 kW, and Above 500 kW); End-User (Public Hospitals, Private Hospitals, Specialty Hospitals, and Emergency Care Facilities); and Region/Country

Wind LiDAR Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Vertical Profiling Wind LiDAR, Ground-Based Wind LiDAR, Nacelle-Mounted Wind LiDAR, Airborne Wind LiDAR, and Others); Component (Sensor, Navigator, Laser, and Others); Location (Onshore and Offshore); Application (Wind Power, Meteorology & Environment, and Aviation); and Region/Country