DNA Data Storage Market: Current Analysis and Forecast (2026-2034)

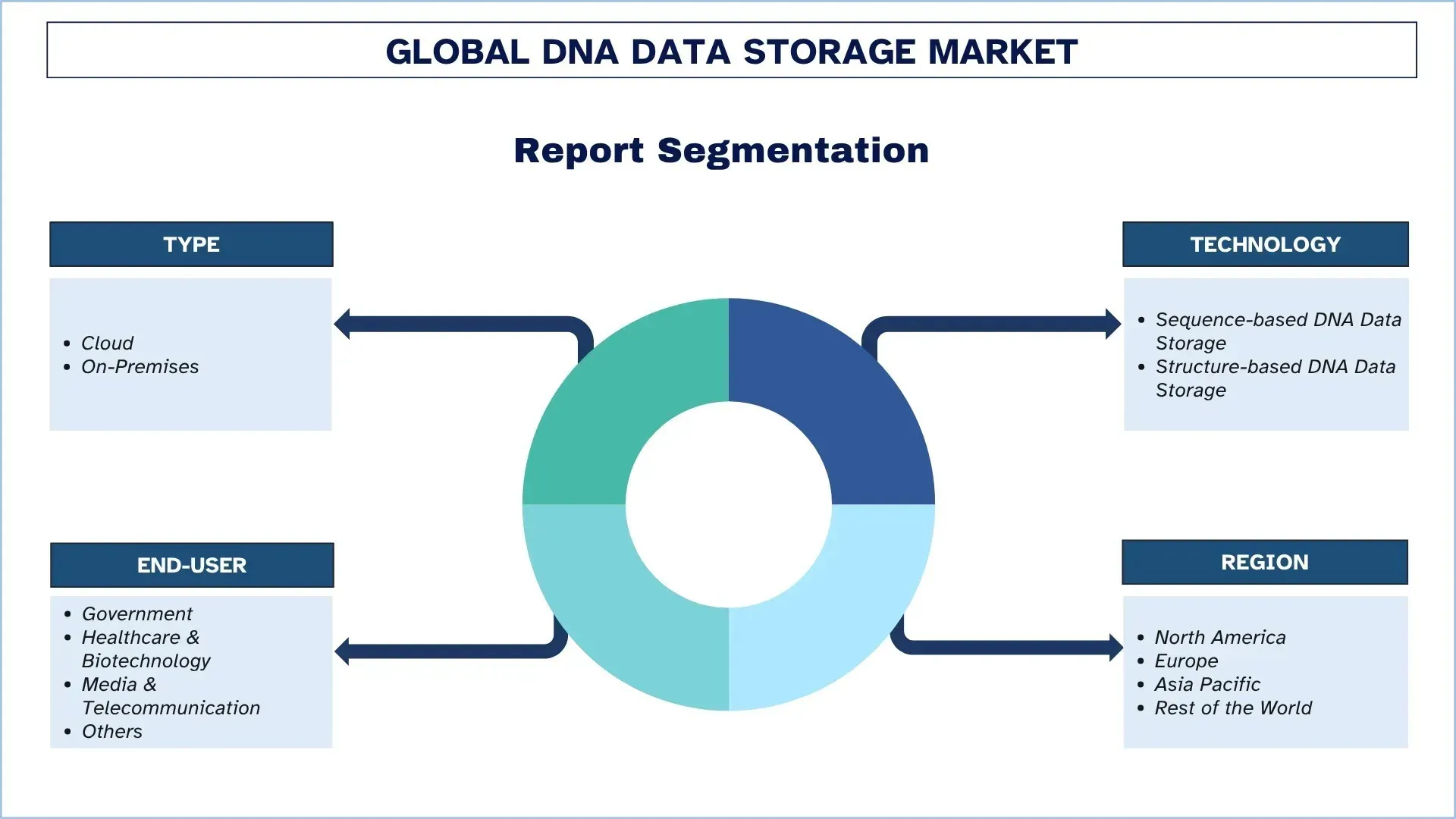

Emphasis on Type (Cloud and On-Premises); Technology (Sequence-based DNA Data Storage and Structure-based DNA Data Storage); End-User (Government, Healthcare & Biotechnology, Media & Telecommunication, and Others); and Region/Country

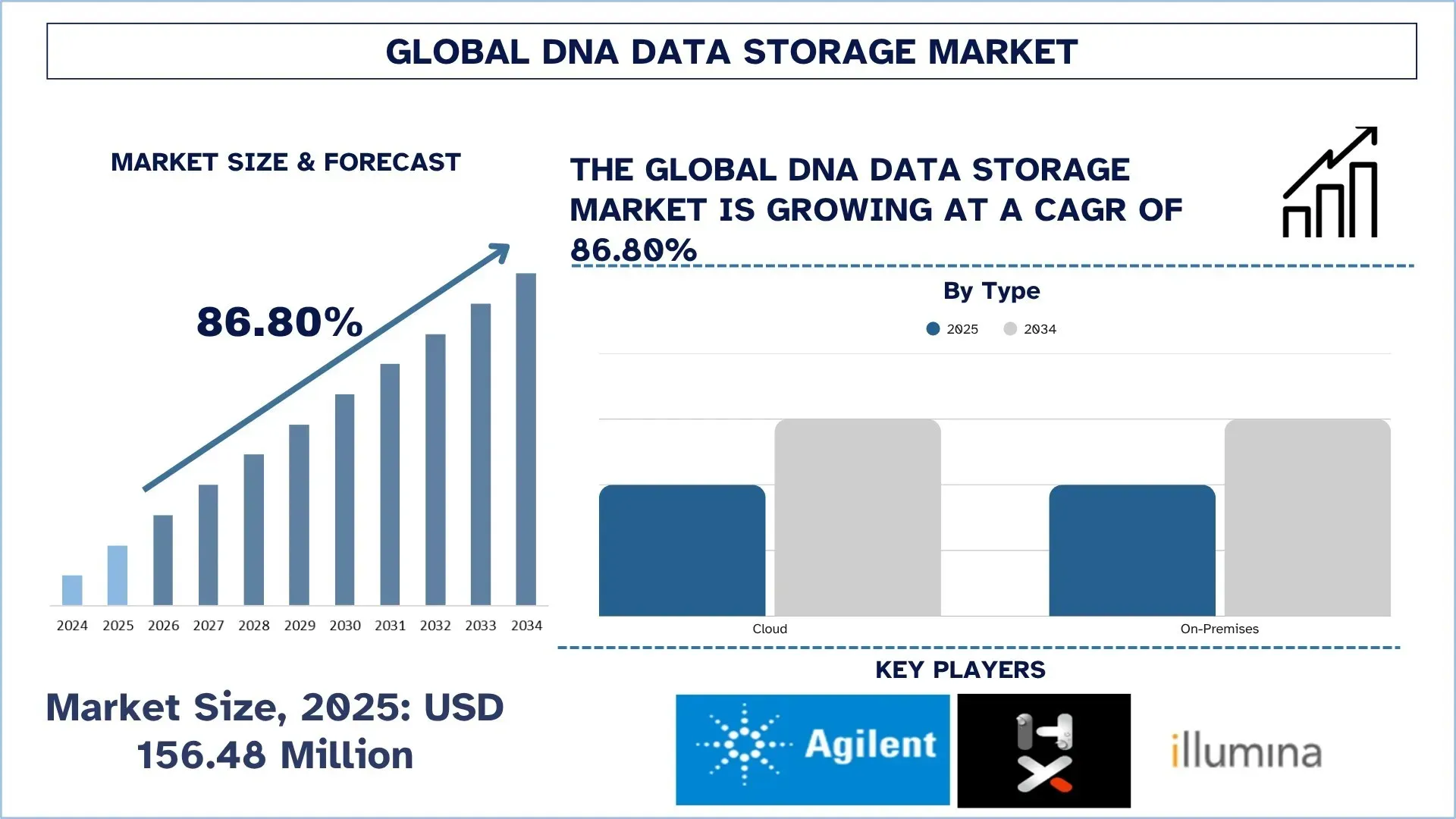

Global DNA Data Storage Market Size & Forecast

The global DNA Data Storage Market was valued at USD 156.48 million in 2025 and is expected to grow at a strong CAGR of around 86.80% during the forecast period (2026-2034F), driven by the growing need to store data in ultra-high-density, long-term, and energy-efficient archival storage, the surging amount of data produced worldwide, and the rising need to minimize the use of power and infrastructure footprint in data centers.

DNA Data Storage Market Analysis

DNA data storage is a next-generation memory and storage archiving technology that encodes digital information in synthetic DNA molecules, enabling very high-density storage and the retention of data over very long durations without constant power. It provides an interesting trade-off of storage permanence, space efficiency, and long-term sustainability, and is one of the promising solutions to traditional archival media. This technology involves DNA synthesis, sequencing, and decoding to write, store, and retrieve data and has the potential to provide ultra-compact data retention, low-energy standby, and long-term cold storage service. DNA data storage application facilitates archival preservation over time, optimization of physical storage space, and minimizing energy reliance, and it assists businesses and institutions to meet the increasing demands of storing large volumes of data that are rarely accessed. These are being designed to be used in research, cloud, and hyperscale storage, government archives, healthcare data repositories, media libraries, and other data-intensive settings.

The forces behind this rise are the growing need to store data in ultra-high-density, long-term, and energy-efficient archival storage, the surging amount of data produced worldwide, and the rising need to minimize the use of power and infrastructure footprint in data centers. Furthermore, the reality that AI loads, cloud systems, and digital institutions are creating unprecedented amounts of cold data is also conducive to market demand as companies are in search of permanent solutions to traditional tape and disk-based archive systems. Other market forces are the development of DNA synthesis and sequencing technologies, the growing investment in molecular storage research, and the transition to enzymatic synthesis, multiplexed writing, and automated architecture of the DNA writing to enhance scalability and reduce costs. Increased partnership among biotechnology and data infrastructure companies and research institutions, and increasing interest in future-ready storage systems to support AI, IoT, and large-scale digital preservation, are further contributing to market growth.

Global DNA Data Storage Market Trends

This section discusses the key market trends that are influencing the various segments of the global DNA Data Storage market, as found by our team of research experts.

Shift Toward Enzymatic Synthesis and High-Throughput Automation

One of the most significant technology trends that has influenced the DNA data storage market is the shift to a less traditional and more chemical-writing workflow, to enzymatic, multiplexed, and more automated DNA writing methods. The significance of this shift is that the long-term commercial viability of the market hinges on reducing synthesis costs, increasing process efficiency, and creating systems capable of accommodating vast archival data volumes compared to current laboratory-scale methods. Enzymatic synthesis, parallel writing, and automated handling have been identified as the most popular paths to practical scale, as reported in the industry. The tendency is already reflected in recent developments. The enzymatic and multiplexed synthesis is becoming a core innovation frontier in the market. In August 2025, Catalog published an article titled “Demonstration of a Scalable DNA Computing Platform: Writing and Selection”, which supports the assertion that the competitive direction of the market is focused on scalable writing architecture instead of proof-of-concept storage per se. Also, in March 2026, following the sale of the assets of Catalog to Biomemory, which announced that the combined platform would combine enzymatic DNA-block assembly with scalable high-speed printing and high-throughput reading. Interestingly, the companies positioned the architecture as a shift away from base-by-base synthesis, which further fuelled the market push towards faster, more industrialized, data-center-deployable DNA writing systems.

DNA Data Storage Industry Segmentation

This section provides an analysis of the key trends in each segment of the global DNA Data Storage market report, along with forecasts at the global, regional, and country levels for 2026-2034.

The On-Premises segment held a significant share during the forecast period (2026-2034).

Based on type, the Global DNA Data Storage market is segmented into Cloud and On-Premises. In 2025, the On-Premises segment held a significant share of the market. This is to a large degree due to the fact that DNA data storage deployments are still in a relatively early phase of commercialization and are more likely to be implemented in a controlled setting like a research organization, government archives, healthcare repositories, and large enterprises where high levels of data security, infrastructure control, and regulatory compliance are required. It is preferable in these environments as it enables organizations to handle sensitive archival information at the point and to tailor storage processes and combine DNA-based at the point with long-term preservation approaches within the organization. It also more readily finds support in the continued technological advancements in the areas of DNA synthesis, sequencing, and retrieval systems, which are being tested and implemented first in specific, institution-led settings.

The Sequence-based DNA Data Storage Segment Dominates the Global DNA Data Storage Market.

Based on technology, the Global DNA Data Storage market is segmented into Sequence-based DNA Data Storage and Structure-based DNA Data Storage. In 2025, the Sequence-based DNA Data Storage segment held a significant share of the market. This is mainly because it is the most proven and most studied method for encoding digital information in DNA and is more in line with current developments in DNA synthesis, sequencing, and decoding. It is more popular because it offers a better commercialization route, is more compatible with existing biotechnology infrastructure, and has broader validation in archival storage studies and pilot-scale implementations. The segment also enjoys continued innovation in enzymatic synthesis, multiplexed writing, and automated data retrieval workflow, which keeps on enhancing scalability and cost effectiveness.

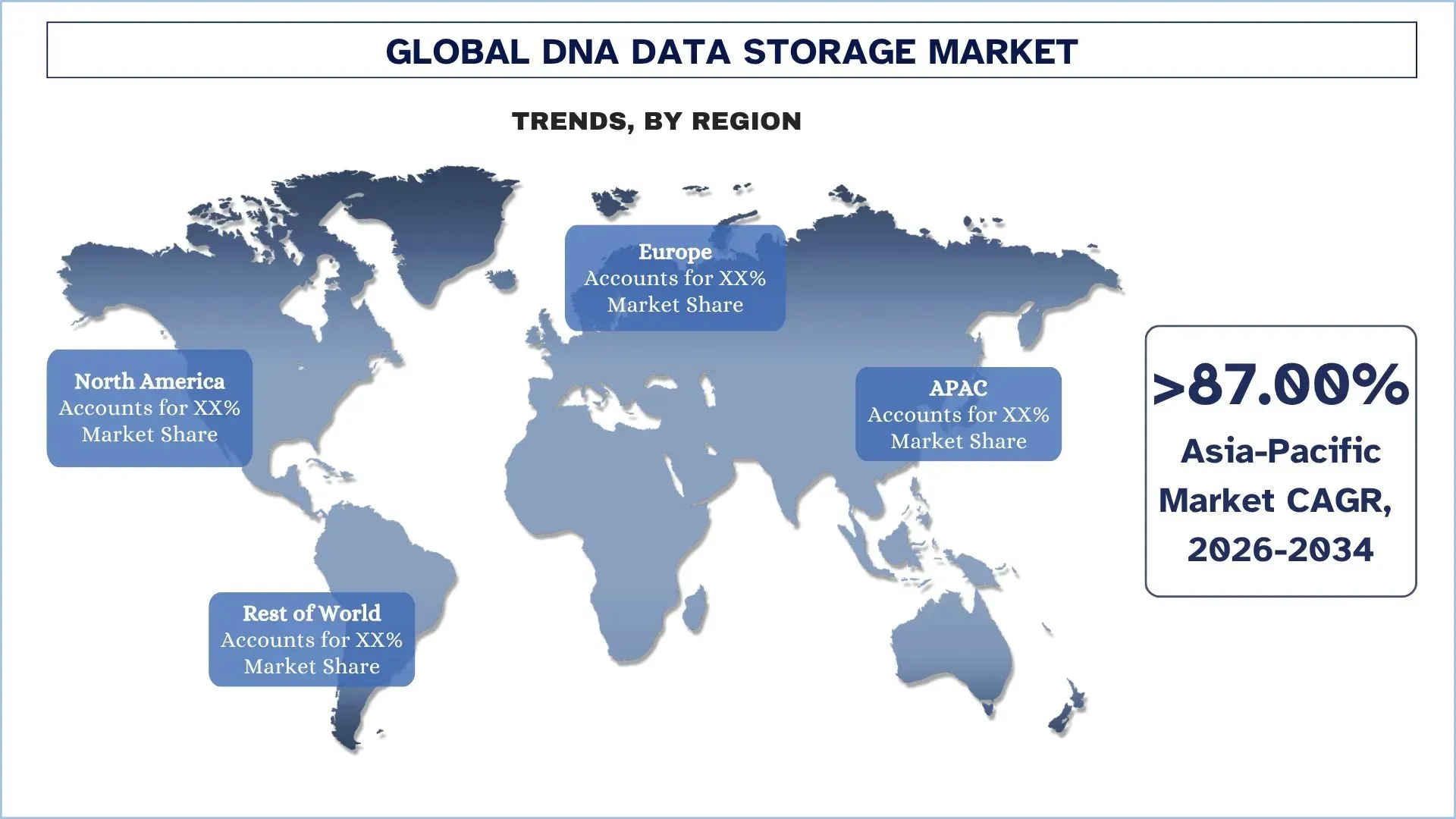

North America holds the largest market share in the global DNA Data Storage market

As of 2025, North America ruled the world DNA Data Storage market due to the high biotechnology and data infrastructure ecosystem in the region, early adoption of advanced archival storage technologies, and several top research institutions, technology firms, and DNA storage innovators. The market in the area is growing due to the rising demand for long-term, high-density, and energy-efficient data storage in the healthcare sector, government, research, cloud infrastructure, and enterprise data management. Moreover, the increased interest in innovation in DNA synthesis and sequencing, and automated molecular storage workflow, is increasing the uptake of DNA data storage in North America. The region is also benefiting from increased investment in next-generation data preservation systems, strong academic-industrial collaboration, and rising demand for long-term storage systems capable of managing enormous volumes of cold data.

The United States held a dominant share of the North American DNA Data Storage Market in 2025

In 2025, the U.S market dominated the worldwide as well as the North America DNA Data Storage market due to the strong base of biotechnology and digital infrastructure in the country, the intensive investment made by technology firms and academic research consortia, and the existence of domestically-oriented innovators specializing in DNA synthesis, sequencing, and automated archival storage processes. The market in the country is growing due to the rising demand for high-density, long-term, durable, and energy-efficient data archiving in the healthcare, government, defense, research, and enterprise sectors. Moreover, the growing interest in automated and high-throughput systems to write and read DNA and the ongoing development of the DNA Storage project by Microsoft and a silicon-based high-throughput DNA synthesis platform by Twist Biosciences is driving use in the U.S.

DNA Data Storage Industry Competitive Landscape

The global DNA Data Storage market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, geographical expansions, and mergers and acquisitions.

Top DNA Data Storage Market Companies

Some of the major players in the market are Agilent Technologies, Inc., Helixworks Technologies, Ltd., Illumina, Inc., Microsoft, Iridia Inc., Twist Bioscience, Catalog, Thermo Fisher Scientific Inc., Micron Technology, Inc., and Eurofins Genomics LLC.

Recent Developments in the DNA Data Storage Market

In July 2025, the Library of Congress announced it is undertaking a pilot project to store and migrate collections data using synthetic DNA and has plans to further collaborate with other government stakeholders related to this endeavor.

In April 2026, GenScript Biotech and Mimulus announced a multi-year collaboration to commercially scale DNA-based data storage as the AI era arrives. The specified objective is to create industrial-scale molecular archival storage capable of storing data in DNA without electricity post-encoding, and the companies aim to achieve significant cost savings by 2030.

In March 2026, imec and Atlas Data Storage also noted that more rapid data generation in the AI era is stretching existing storage media to the limits of capacity, sustainability, cost, and long-term reliability, which supports the need to develop new methods of archiving.

Global DNA Data Storage Market Report Coverage

Details | |

Base year | 2025 |

Forecast period | 2026-2034 |

Growth momentum | Accelerate at a CAGR of 86.80% |

Market size 2025 | USD 156.48 million |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | The North America region is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, and India. |

Companies profiled | Agilent Technologies, Inc., Helixworks Technologies, Ltd., Illumina, Inc., Microsoft, Iridia Inc., Twist Bioscience, Catalog, Thermo Fisher Scientific Inc., Micron Technology, Inc., and Eurofins Genomics LLC. |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Type, By Technology, By End-User, and By Region/Country |

Reasons to Buy the DNA Data Storage Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional level analysis of the industry.

Customization Options:

The global DNA Data Storage Market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global DNA Data Storage Market Analysis (2024-2034)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global DNA Data Storage market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the DNA Data Storage value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global DNA Data Storage market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including type, technology, end-user, and regions within the global DNA Data Storage market.

The Main Objective of the Global DNA Data Storage Market Study

The study identifies current and future trends in the global DNA Data Storage market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current and forecast market size of the global DNA Data Storage market and its segments in terms of value (USD).

DNA Data Storage Market Segmentation: Segments in the study include areas of type, technology, end-user, and region.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the DNA Data Storage industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the DNA Data Storage market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the current market size and growth potential of the global DNA Data Storage market?

The global DNA Data Storage market is valued at USD 156.48 million in 2025, driven by the rising demand for ultra-high-density, long-term, and energy-efficient archival storage, increasing global data generation, and ongoing advances in DNA synthesis, sequencing, and automated data writing technologies.

Q2: Which segment has the largest share of the global DNA Data Storage market by Type?

The On-Premises segment currently leads the market, supported by early adoption in research institutions, government archives, healthcare organizations, and large enterprises that require greater data security and regulatory compliance.

Q3: What are the driving factors for the growth of the global DNA Data Storage market?

Key growth drivers include the explosive growth in global digital and archival data volumes, continuous advancements in DNA synthesis, sequencing, and error-correction technologies, and the rising need for sustainable, long-life, and high-density archival storage solutions.

Q4: What are the emerging technologies and trends in the global DNA Data Storage market?

Major trends include the shift toward enzymatic synthesis and high-throughput DNA writing, growing focus on standards, metadata schemas, and manageable interfaces, and the emergence of pilot archival deployments and secure vaulting models.

Q5: What are the key challenges in the global DNA Data Storage market?

Major challenges include the high cost of DNA synthesis and sequencing workflows, slow read/write speeds and random-access limitations, and the lack of standardization, interoperability, and governance clarity, which continue to restrict large-scale commercialization.

Q6: Which region dominates the global DNA Data Storage market?

North America dominates the market due to its strong biotechnology and digital infrastructure ecosystem, early adoption of advanced archival storage technologies, robust research and development activity, and the presence of key DNA storage innovators and academic-industry collaborations.

Q7: Who are the key competitors in the global DNA Data Storage market?

Top players in the DNA Data Storage industry include:

• Agilent Technologies, Inc.

• Helixworks Technologies, Ltd.

• Illumina, Inc.

• Microsoft

• Iridia Inc.

• Twist Bioscience

• Catalog

• Thermo Fisher Scientific Inc.

• Micron Technology, Inc.

• Eurofins Genomics LLC

Q8: What opportunities are emerging for new entrants and technology providers in this market?

Key opportunities include the expansion of DNA data storage in government, defense, and national archive preservation use cases, rising adoption across healthcare, biotechnology, and genomics data archiving, and strong growth potential in the Asia-Pacific region, driven by expanding digital infrastructure and genomics investments.

Q9: How is digital transformation influencing the DNA Data Storage market?

Digital transformation is increasing the volume of long-term archival data generated across AI, cloud, healthcare, government, and enterprise systems. As organizations expand data-intensive infrastructure, demand is rising for storage solutions that are compact, durable, and energy-efficient, which is supporting interest in DNA data storage. This shift is also encouraging companies and research institutions to develop scalable DNA writing, sequencing, and archival platforms for future data preservation needs.

Related Reports

Customers who bought this item also bought

India IT and BPO Services Market: Current Analysis and Forecast (2026-2034)

Emphasis on Service Type (IT Services, BPO Services, Engineering & R&D Services); Outsourcing Type (Onshore, Offshore, Nearshore); Organization Size (Large Enterprises, SMEs); End-User Industry (BFSI, IT & Telecom, Healthcare, Retail & E-commerce, Manufacturing, Others); and Region/States

Gi-Fi Technology Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Display Devices and Network Infrastructure Devices); Technology (System on chip and Integrated Circuit Chip); Application (Consumer Electronics, Commercial, and Networking); and Region/Country

DNA Data Storage Market: Current Analysis and Forecast (2026-2034)

Emphasis on Type (Cloud and On-Premises); Technology (Sequence-based DNA Data Storage and Structure-based DNA Data Storage); End-User (Government, Healthcare & Biotechnology, Media & Telecommunication, and Others); and Region/Country

Cloud Service Brokerage Market: Current Analysis and Forecast (2026-2034)

Emphasis on Service Type (Integration and Support, Automation and Orchestration, Billing and Provisioning, Migration and Customization, Security and Compliance, and Others); Platform (Internal Brokerage Enablement and External Brokerage Enablement); Deployment (Private, Public, and Hybrid); Enterprise Size (Large Enterprises, and Small & Medium-Sized Enterprises); End-Use (IT & Telecom, BFSI, Government & Public Sector, Healthcare, Consumer Goods & Retail, Manufacturing, Energy & Utilities, and Others); and Region/Country