India Decarbonization HVAC Market: Current Analysis and Forecast (2026-2034)

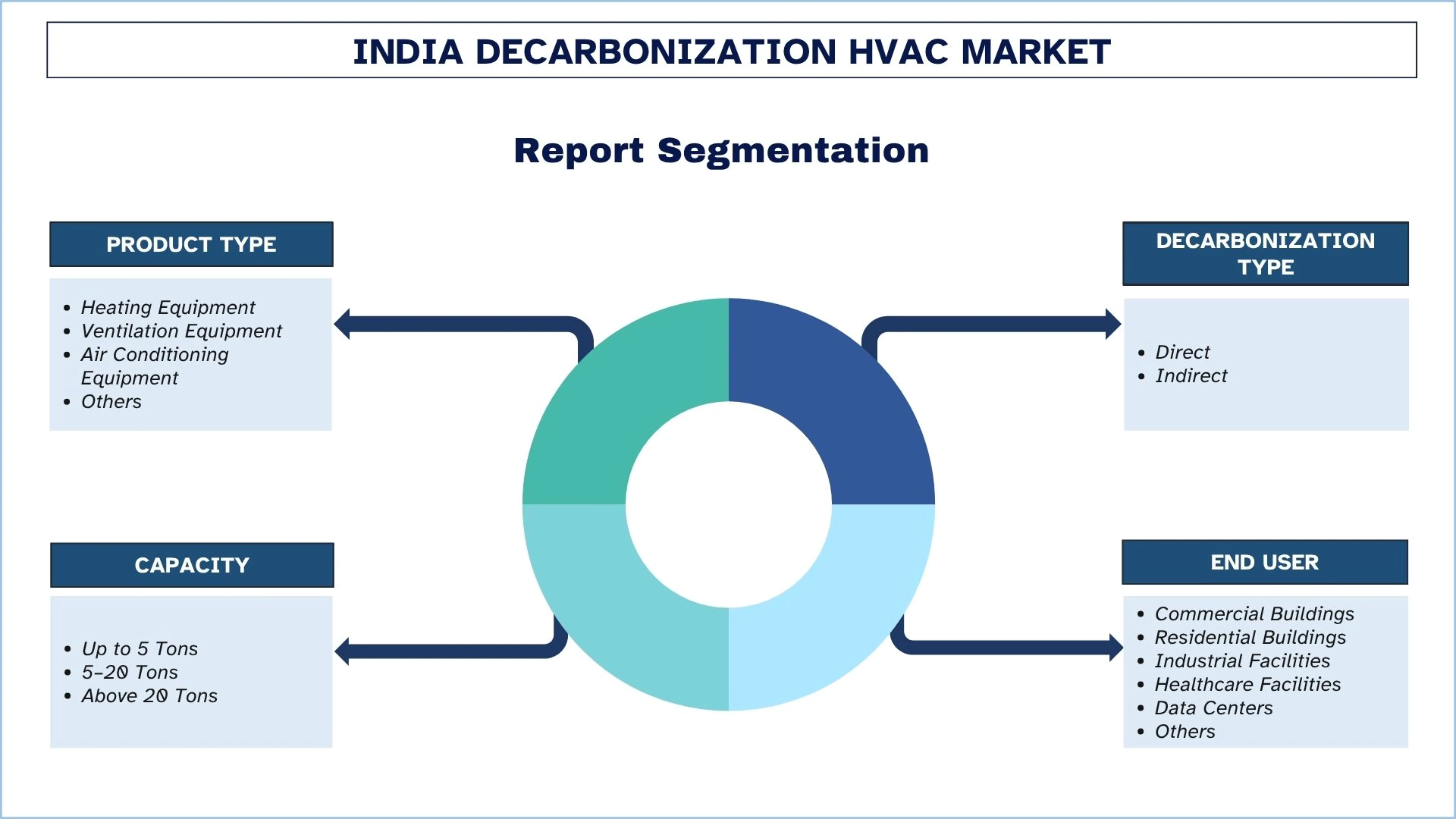

Emphasis on Product Type (Heating Equipment, Ventilation Equipment, Air Conditioning Equipment, Others); Decarbonization Type (Direct, Indirect); Capacity (Up to 5 Tons, 5-20 Tons, Above 20 Tons); End User (Commercial Buildings, Residential Buildings, Industrial Facilities, Healthcare Facilities, Data Centers, Others); and Region/States

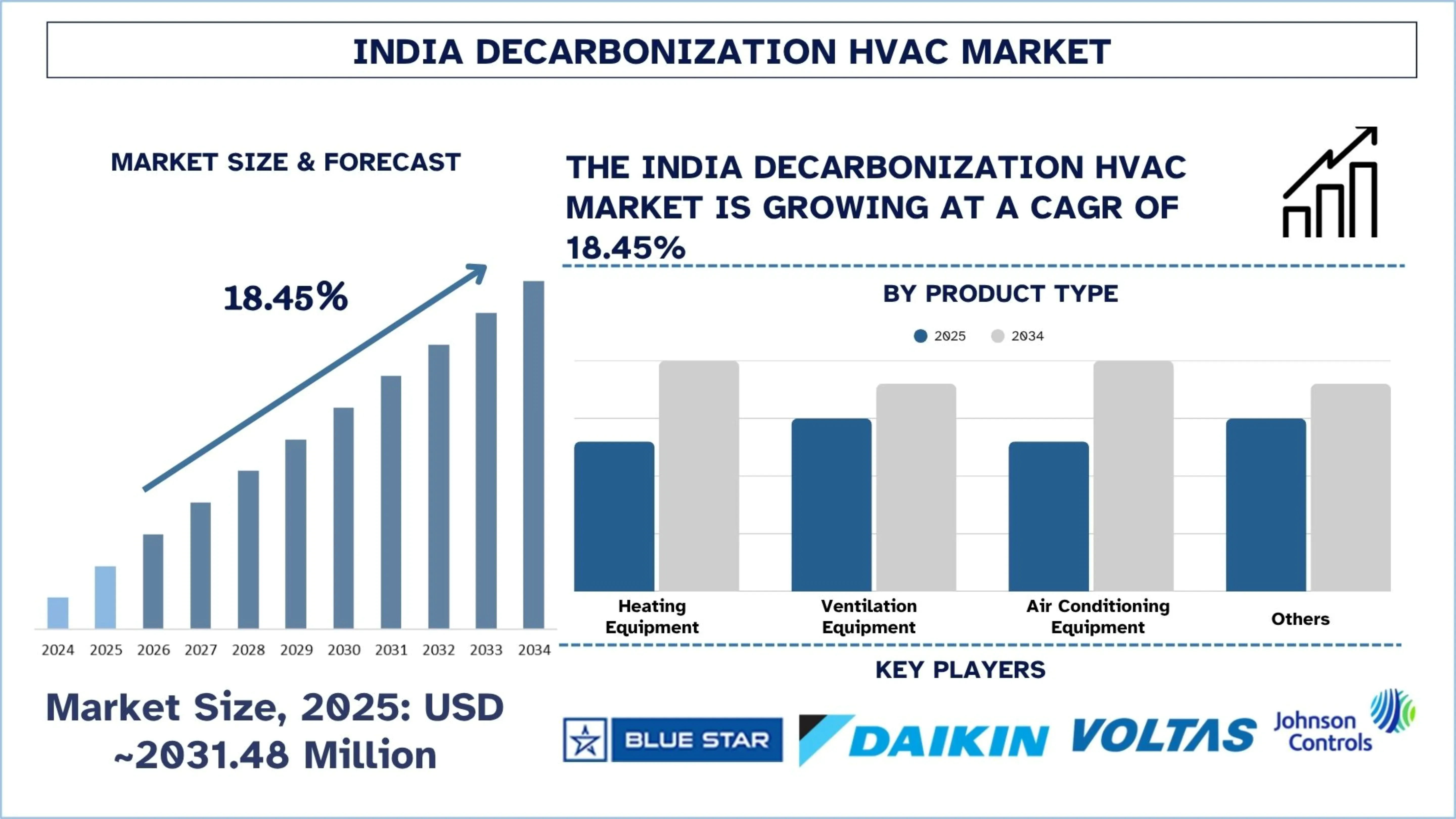

India Decarbonization HVAC Market Size & Forecast

The India Decarbonization HVAC Market was valued at USD 2031.48 million in 2025 and is expected to grow at a strong CAGR of around 18.45% during the forecast period (2026-2034F), driven by rising commercial building energy-efficiency requirements and the expansion of green building certifications across India.

India Decarbonization HVAC Market Analysis

Decarbonization in HVAC refers to heating, ventilation, and air conditioning systems that minimize carbon emissions by enhancing energy efficiency, reducing electricity use, and replacing high-carbon refrigerants with less harmful alternatives. These technologies are inverter-driven cooling systems, heat pumps, smart controls, and low-global-warming-potential refrigerants.

The implementation is growing rapidly in India by large-scale installation of inverter-based air conditioning, variable refrigerant flow systems, intelligent building automation, heat recovery systems, and sophisticated chillers in commercial buildings, data centers, medical facilities, and industrial infrastructure. Also, smart sensors, predictive maintenance platforms, rooftop solar-linked cooling systems, and energy management software are currently being adopted to optimize operating efficiency. Moreover, manufacturers are localizing the production of high-efficiency compressors, systems that can use low-GHG (greenhouse gas) refrigerants, modular HVAC systems, and low-efficiency norms to meet growing domestic demand, tightening efficiency standards, and broader green building standards.

For instance, on March 12, 2026, LG Electronics (LG) debuted compressor solutions tailored for the Indian market at ACREX 2026 – a leading heating, ventilation, and air conditioning (HVAC) and building automation exhibition in South Asia at the Bombay Exhibition Center in Mumbai. Developed in response to India’s growing air-conditioning demand and rising energy-efficiency standards, the new lineup is designed for residential and commercial applications and reflects LG’s continued focus on localized product development and manufacturing.

The Residential HVAC zone will highlight new rotary compressor solutions for the 1- to 2-ton range, which represents a major segment of India’s residential air conditioning market. These compressors are engineered for inverter-driven residential systems, balancing energy efficiency and cost competitiveness while reflecting local market requirements.

India Decarbonization HVAC Market Trends

This section discusses the key market trends that are influencing the various segments of the India Decarbonization HVAC market, as found by our team of research experts.

Shift Towards Electrification of HVAC Systems

The trend toward the electrification of HVAC Systems is a significant development in the Indian decarbonization of the HVAC market, with end users increasingly abandoning traditional fossil-fuel-reliant heating and cooling systems in favor of electrically powered, high-efficiency systems. Also, the shift is driving the use of inverter-based air conditioning, electric heat pumps, and high-tech variable refrigerant flow systems in commercial and industrial buildings. Moreover, the electrification helps reduce operational emissions and enhances interoperability with renewable power integration and smart energy management systems. Furthermore, the rising trend of green buildings, high-quality infrastructure, and institutional projects with energy performance requirements drives the growth of the market. For instance, on February 14, 2025, LG Electronics announced expanded HVAC initiatives focused on decarbonization and electrification through its new ES business division, highlighting advanced chillers, inverter heat pumps, and energy-efficient thermal solutions for commercial and residential applications. The company also showcased oil-free centrifugal chillers and cold-climate heat pump technologies designed to improve efficiency and reduce carbon emissions in next-generation buildings and data centers.

Decarbonization HVAC Industry Segmentation

This section provides an analysis of the key trends in each segment of the India Decarbonization HVAC market report, along with forecasts at the regional and state levels for 2026-2034.

The air conditioning equipment market held the dominant share of the Decarbonization HVAC Market in 2025.

Based on the product type, the market is segmented into heating equipment, ventilation equipment, air conditioning equipment, and others. Among these, the air conditioning equipment market held the dominant share of the market in 2025. This is mainly due to energy-consuming HVAC applications in commercial buildings, residential developments, healthcare facilities, and institutional infrastructure. The shift from traditional systems to inverter-based and low-emission air conditioning systems is accelerating product innovation, localized production, and the adoption of efficient cooling systems. Therefore, this provides long-term growth opportunities as organizations increase portfolios in line with energy-efficiency laws and refrigerant conversion requirements. For instance, on February 12, 2026, Panasonic Life Solutions India (PLSIND), a leading diversified technology company, announced the launch of its 2026 lineup of Residential Air Conditioners engineered specifically to tackle the country’s extreme weather conditions. Designed for reliable performance, the new range reflects Panasonic’s focus on delivering durable, energy-efficient, and climate-resilient cooling solutions tailored for Indian homes.

The data centers' decarbonization HVAC market is expected to grow with a significant CAGR during the forecast period (2026-2034.

Based on the end user, the market is segmented into commercial buildings, residential buildings, industrial facilities, healthcare facilities, data centers, and others. Among these, the data centers' decarbonization HVAC market is expected to grow with a significant CAGR during the forecast period (2026-2034). The growth drivers in the Indian HVAC decarbonization sector are cooling reliability and energy performance, which are critical in high-density digital infrastructure. The trend of increasing hyperscale investments and cloud expansion is driving the demand for precision cooling, modular chillers, and smart thermal management systems. This is driving high-value prospects of advanced HVAC implementation, where the efficiency of operation has a direct impact on long-term infrastructure economics. For instance, on March 10, 2026, Voltas Limited expanded its presence in India’s data centre cooling market by strengthening its focus on precision cooling, high-capacity chillers, and engineered thermal management systems designed for high-density digital infrastructure. The move aligns with rising demand from hyperscale facilities, where cooling efficiency, uptime reliability, and energy optimization are becoming critical growth drivers for the data center segment in India.

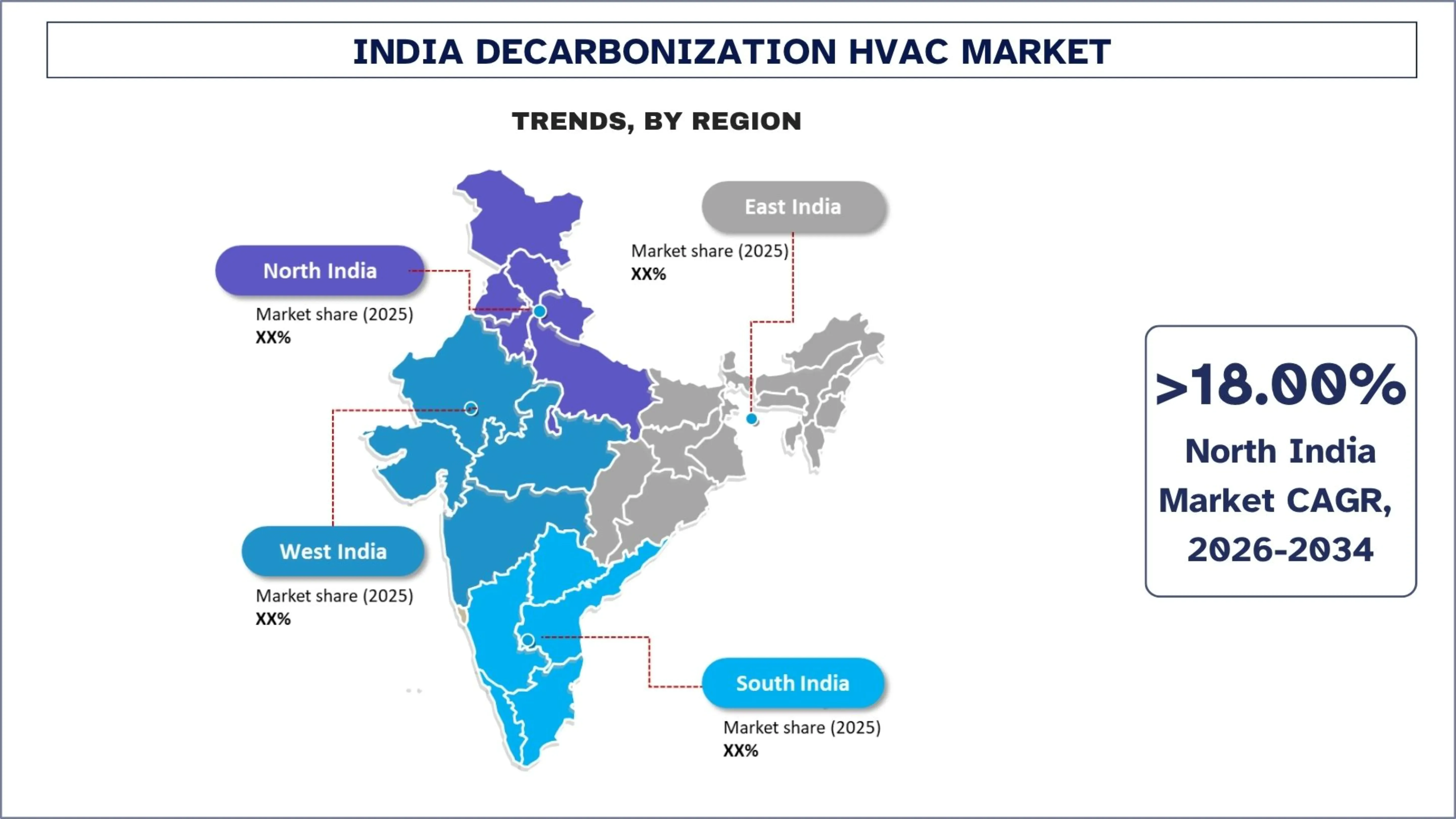

North India leads the Decarbonization HVAC Market in 2025.

North India led the regions of the Indian decarbonization HVAC market, owing to high demand from real estate, government infrastructure development, healthcare facilities, and large government buildings in major cities such as Delhi, Noida, and Gurugram. Also, the high summer temperatures and long cooling periods significantly drive energy use in HVAC systems, thereby promoting the rapid adoption of energy-saving air conditioning systems, intelligent controls, and refrigerant-efficient technologies. Additionally, the high retrofit activity in office complexes, hotels, and institutional facilities, where the replacement of conventional systems is gaining momentum, is also advantageous to the region. The mass development of metro rails, modernization of airports, and commercial buildings still necessitate high-quality cooling systems aligned with energy-efficiency goals. All of these contribute to North India being a robust contributor to both demand volume and technology adoption in decarbonized HVAC implementation.

For example, on March 25, 2026, LGE India committed to expanding clean energy adoption across its manufacturing operations. LGE India, one of India’s leading consumer electronics brands, signed long-term solar Power Purchase Agreements (PPAs) with Hinduja Renewables Energy Private Limited (HREPL) and Sunsure Energy. LGE India will source solar power for its Greater Noida and Pune manufacturing facilities, thereby reducing its carbon footprint while strengthening its transition towards sustainable manufacturing. As part of these tie-ups, LGE India signed a 9.80 megawatt peak (MWp) solar PPA with HREPL for its Pune manufacturing facility and an 11 MWp solar PPA with Sunsure Energy for its Greater Noida facility. LGE India will source approximately 3.21 crore units (32.1 million) of renewable energy annually for both facilities, collectively offsetting around 0.61 million metric tonnes of CO2e over the project lifetime.

India Decarbonization HVAC Industry Competitive Landscape

The India Decarbonization HVAC market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, and mergers and acquisitions.

Top India Decarbonization HVAC Companies

Some of the major players in the market are Carrier, Blue Star Limited, Daikin Airconditioning India Pvt. Ltd. (DAIKIN INDUSTRIES, Ltd.), Voltas (Tata Group), Johnson Controls, LG Electronics, Danfoss, Panasonic Life Solutions India Pvt. Ltd. (Panasonic Holdings Corporation), Trane, and Mitsubishi Electric Corporation.

Recent Developments in the India Decarbonization HVAC Market

On February 6, 2026, Mitsubishi Electric India, a global leader in electrical and electronic equipment, inaugurated its new air conditioner and compressor manufacturing facility today, in Chennai, Tamil Nadu. The Chennai facility has been developed with a total investment of approximately INR 2,100 crore (USD 226.6 million), underscoring Mitsubishi Electric India’s long-term commitment to strengthening its manufacturing footprint in the country.

On March 19, 2025, Copeland, a global provider of sustainable climate solutions, inaugurated a new state-of-the-art Engineering and Technology Center in Pune, Maharashtra, as part of its broader INR 500 crore (~USD 54.0 million) India investment plan. This new Engineering and Technology Center will focus on advancing energy-efficient and low-GWP and natural refrigerant technologies for global deployments across the HVAC and Refrigeration industry.

India Decarbonization HVAC Market Report Coverage

Details | |

Base year | 2025 |

Forecast period | 2026-2034 |

Growth momentum | Accelerate at a CAGR of 18.45% |

Market size 2025 | USD ~2031.48 million |

Regional analysis | North India, South India, East India, and West India |

Major contributing region | West India is expected to grow at the highest CAGR during the forecasted period. |

Companies profiled | Carrier, Blue Star Limited, Daikin Airconditioning India Pvt. Ltd. (DAIKIN INDUSTRIES, Ltd.), Voltas (Tata Group), Johnson Controls, LG Electronics, Danfoss, Panasonic Life Solutions India Pvt. Ltd. (Panasonic Holdings Corporation), Trane, and Mitsubishi Electric Corporation |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Product Type, By Decarbonization Type, By Capacity, By End User, By Region |

Reasons to Buy the India Decarbonization HVAC Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional level analysis of the industry.

Customization Options:

The India Decarbonization HVAC Market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the India Decarbonization HVAC Market Analysis (2024-2034)

We analyzed the historical market, estimated the current market, and forecasted the future market of the India Decarbonization HVAC market to assess its application in major regions in India. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the Decarbonization HVAC value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the India-Decarbonization HVAC market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including product type, decarbonization type, capacity, end user, and regions within the India Decarbonization HVAC market.

The Main Objective of the India Decarbonization HVAC Market Study

The study identifies current and future trends in the India Decarbonization HVAC market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current market size and forecast the market size of the India Decarbonization HVAC market and its segments in terms of value (USD).

Decarbonization HVAC Market Segmentation: Segments in the study include areas of product type, decarbonization type, capacity, end user, and regions.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the Decarbonization HVAC industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as North India, South India, East India, and West India.

Company Profiles & Growth Strategies: Company profiles of the Decarbonization HVAC market and the growth strategies adopted by the market players to sustain in the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the India Decarbonization HVAC market’s current market size and growth potential?

The India Decarbonization HVAC market was valued at USD ~2031.48 million in 2025 and is expected to grow at a CAGR of 18.45% during the forecast period (2026-2034). This steady growth is primarily supported by rising demand for energy-efficient cooling systems, stricter building energy regulations, expansion of green commercial infrastructure, and increasing adoption of low-emission HVAC technologies across industrial and institutional sectors.

Q2: Which segment has the largest share of the India Decarbonization HVAC market by product type?

The air conditioning equipment segment accounts for the largest market share in the India Decarbonization HVAC market due to its widespread deployment across commercial buildings, residential developments, healthcare facilities, and institutional infrastructure. High replacement demand for inverter-based systems and increasing preference for efficient cooling technologies continue to strengthen this segment’s market leadership.

Q3: What are the driving factors for the growth of the India Decarbonization HVAC market?

Major growth drivers include rising demand for energy-efficient buildings, increasing government regulations on HVAC efficiency, rapid urbanization, expansion of commercial real estate, growth in data center infrastructure, and accelerated adoption of low-global-warming-potential refrigerants. The transition toward electrified HVAC systems is also contributing significantly to long-term market expansion.

Q4: What are the emerging technologies and trends in the India Decarbonization HVAC market?

Key trends shaping the market include electrification of HVAC systems, adoption of variable refrigerant flow technology, integration of smart building controls, predictive maintenance through IoT-enabled systems, use of low-GWP refrigerants, and deployment of AI-based energy optimization platforms. Heat pumps and modular cooling systems are also gaining traction across advanced infrastructure projects.

Q5: What are the key challenges in the India Decarbonization HVAC market?

The sector faces challenges such as high upfront investment costs, limited skilled workforce for advanced HVAC installation, slow retrofit adoption in older buildings, dependence on imported high-efficiency components, and fluctuating electricity costs affecting operational economics. These factors can delay wider adoption despite strong long-term market potential.

Q6: Which region dominates the India Decarbonization HVAC market?

North India dominates the market due to strong commercial construction activity, government infrastructure projects, healthcare expansion, and high cooling demand generated by extreme summer temperatures. Major urban centers continue to drive large-scale deployment of energy-efficient HVAC systems across offices, retail, hospitality, and institutional facilities.

Q7: Who are the key players in the India Decarbonization HVAC market?

Some of the leading companies in the India Decarbonization HVAC Industry include:

• Carrier

• Blue Star Limited

• Daikin Airconditioning India Pvt. Ltd. (DAIKIN INDUSTRIES, Ltd.)

• Voltas (Tata Group)

• Johnson Controls

• LG Electronics

• Danfoss

• Panasonic Life Solutions India Pvt. Ltd. (Panasonic Holdings Corporation)

• Trane

• Mitsubishi Electric Corporation

Q8: How is government policy influencing investment in India’s decarbonized HVAC industry?

Government policy influences investment through energy-efficiency standards, refrigerant transition regulations, green building codes, and broader sustainability targets, which encourage the adoption of advanced HVAC technologies across public and private infrastructure.

Q9: Why are businesses investing in decarbonization-focused HVAC systems in India?

Businesses are investing in decarbonized HVAC systems to reduce long-term energy costs, improve compliance with sustainability targets, lower carbon emissions, and enhance operational efficiency in commercial, industrial, and digital infrastructure assets.

Related Reports

Customers who bought this item also bought

India Decarbonization HVAC Market: Current Analysis and Forecast (2026-2034)

Emphasis on Product Type (Heating Equipment, Ventilation Equipment, Air Conditioning Equipment, Others); Decarbonization Type (Direct, Indirect); Capacity (Up to 5 Tons, 5-20 Tons, Above 20 Tons); End User (Commercial Buildings, Residential Buildings, Industrial Facilities, Healthcare Facilities, Data Centers, Others); and Region/States

Midstream Oil & Gas Filtration Market: Current Analysis and Forecast (2026-2034)

Emphasis on Filter Technology (Coalescer Filters, Cartridge Filters, Mechanical Filters, Bag Filters, Particulate Filters, Activated Carbon Filters, Strainers, and Others); by Application (Gas Processing Plants, Compression Stations, Storage And Distribution, Pipeline Transportation, LNG Processing, and Others); by Filtration Stage (Oil Filtration and Gas Filtration), by End User (Refineries and Petrochemical Industry), and Region/Country

Hydrogen-Powered Hospital Backup Systems Market: Current Analysis and Forecast (2026-2034)

Emphasis on System Type (Portable, Stationary, Hybrid); Power Capacity (Below 100 kW, 100–500 kW, and Above 500 kW); End-User (Public Hospitals, Private Hospitals, Specialty Hospitals, and Emergency Care Facilities); and Region/Country

Wind LiDAR Market: Current Analysis and Forecast (2025-2033)

Emphasis on Product Type (Vertical Profiling Wind LiDAR, Ground-Based Wind LiDAR, Nacelle-Mounted Wind LiDAR, Airborne Wind LiDAR, and Others); Component (Sensor, Navigator, Laser, and Others); Location (Onshore and Offshore); Application (Wind Power, Meteorology & Environment, and Aviation); and Region/Country