Aeroderivative Sensor Market: Current Analysis and Forecast (2025-2033)

Emphasis on Sensor Type (Temperature Sensors, Pressure Sensors, Vibration Sensors, Flame Sensors, and Others); Service Provider (OEMs and Aftermarket); End-User (Industrial, Marine, Aerospace & Defense, Power & Energy, and Oil & Gas); and Region/Country

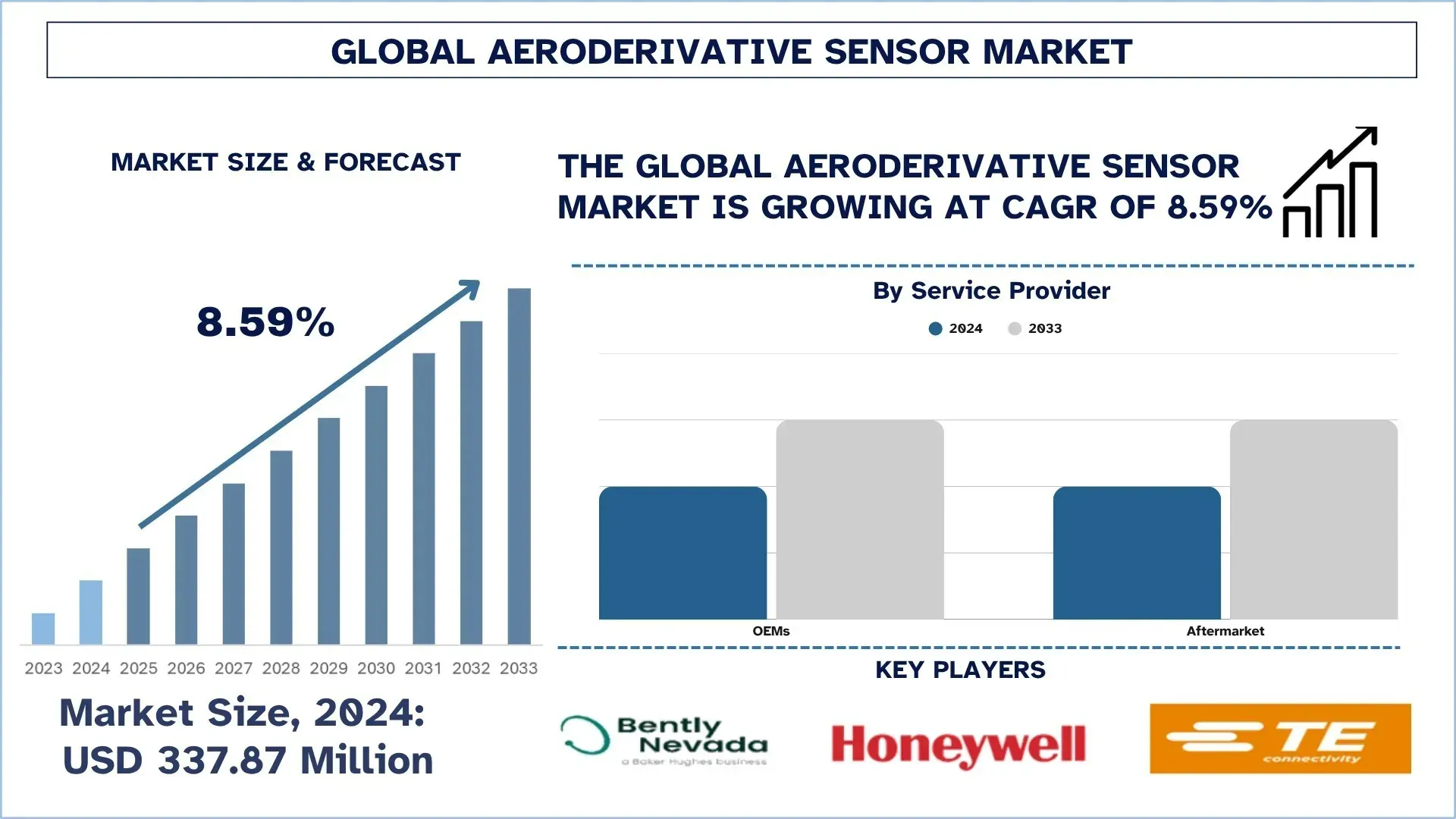

Global Aeroderivative Sensor Market Size & Forecast

The Global Aeroderivative Sensor Market was valued at USD 337.87 million in 2024 and is expected to grow at a strong CAGR of around 8.59% during the forecast period (2025-2033F), driven by advancements in high-temperature and miniaturized sensor technologies, rising focus on operational efficiency & asset lifecycle management, and growing retrofitting of aging turbine infrastructure.

Aeroderivative Sensor Market Analysis

The aeroderivative sensor market is showing rapid growth, driven by increasing demand for efficient turbine monitoring and predictive maintenance solutions. The market is moderately consolidated, with leading companies prioritizing innovation, digital integration, and strategic partnerships to enhance their competitive edge. Along with this, growth is mainly supported by expansion in power generation, oil and gas, marine, and industrial sectors. For instance, in September 2023, Baker Hughes unveiled Druck hydrogen-rated pressure sensors designed for gas turbines and hydrogen applications, providing improved accuracy, durability, and reliability and supporting the growing adoption of advanced sensing technologies in the energy and industrial sectors. Furthermore, the adoption of IoT-based and smart sensor technologies is improving operational efficiency and data accuracy. At the same time, regional growth trends show strong demand in North America and rapid growth in the Asia-Pacific region, driven by industrialization and energy infrastructure development.

Global Aeroderivative Sensor Market Trends

This section discusses the key market trends that are influencing the various segments of the global aeroderivative sensor market, as found by our team of research experts.

Rising Adoption of Wireless and Smart Sensors

Rising adoption of wireless and smart sensors is reshaping the aeroderivative sensor market by enabling real-time monitoring, improved data accuracy, and enhanced operational efficiency. These sensors reduce the need for complex wiring, lowering installation and maintenance costs while increasing deployment flexibility. At the same time, the integration with Industrial IoT platforms allows seamless data transmission, remote diagnostics, and predictive maintenance capabilities. In addition, smart sensors equipped with advanced analytics and self-diagnostic features improve the reliability and performance of aeroderivative systems. For instance, in October 2024, Yokogawa Electric Corporation introduced an explosion-proof wireless steam trap monitoring device, allowing remote monitoring across large areas and predictive maintenance. This solution utilizes Industrial IoT and LoRaWAN communication, boosting operational efficiency, minimizing energy losses, and facilitating real-time equipment tracking across industrial sites. Simultaneously, the ongoing digital transformation across diverse sectors is fueling the worldwide embrace of wireless and intelligent sensor technologies.

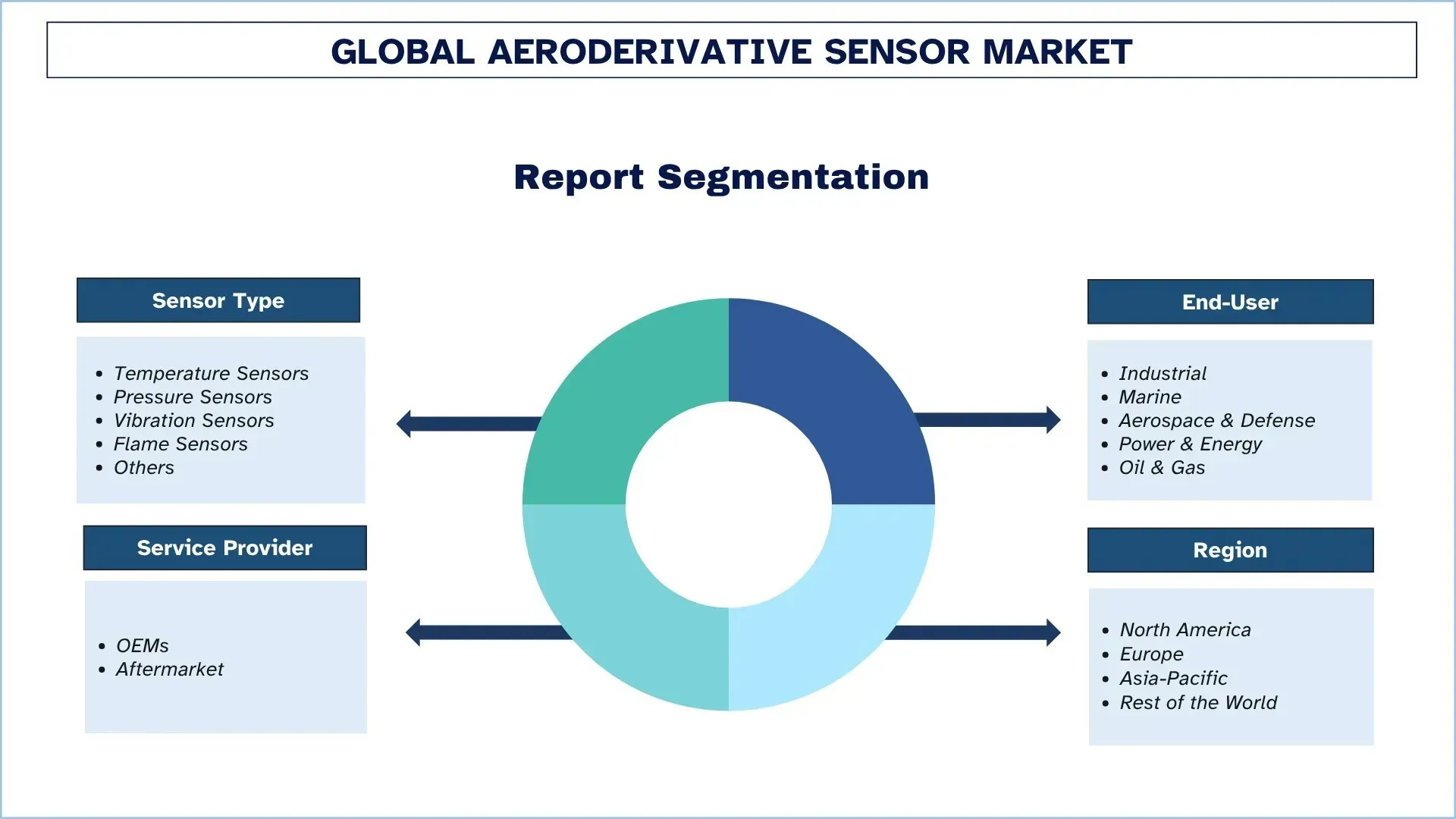

Aeroderivative Sensor Industry Segmentation

This section provides an analysis of the key trends in each segment of the global aeroderivative sensor market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Flame Sensors Dominates the Global Aeroderivative Sensor Market

Based on sensor type, the market is categorized into temperature sensors, pressure sensors, vibration sensors, flame sensors, and others. In 2024, Flame sensors hold the largest share of the aeroderivative sensor market due to their important role in ensuring combustion safety, real-time flame detection, and regulatory compliance in gas turbines, making them indispensable across power generation and oil & gas applications. Their reliability in preventing hazardous failures further strengthens adoption. However, vibration sensors are showing the fastest growth due to rising emphasis on predictive maintenance, condition monitoring, and digitalization of turbine operations. Furthermore, the increasing integration with advanced analytics and industrial IoT systems is driving demand for vibration sensors to minimize downtime, optimize performance, and reduce operational costs.

OEMs dominate the Global Aeroderivative Sensor Market.

Based on the service provider, the market is categorized into OEMs and the aftermarket. OEMs hold the largest share of the aeroderivative sensor market because they integrate sensors during initial equipment manufacturing, ensuring system compatibility, reliability, and compliance with performance standards. Additionally, their strong presence is supported by long-term contracts and direct relationships with end users. However, the aftermarket segment is showing the fastest growth due to the increasing installed base of turbines and rising demand for maintenance, repair, and replacement. At the same time, rising adoption of predictive maintenance, along with cost-effective retrofit solutions and flexibility offered by third-party providers, is further accelerating aftermarket growth across global energy and industrial sectors.

North America holds the largest market share in the global aeroderivative sensor market

North America accounts for the largest share of the aeroderivative sensor market because of the widespread use of aeroderivative gas turbines across power, oil and gas, and industrial sectors. For example, in July 2025, GE Vernova collaborated with Crusoe to deliver 29 aeroderivative gas turbines for AI data centers, producing approximately 1 GW of power. This showcases strong regional growth demand. Along with this, the region benefits from advanced energy infrastructure, early technology adoption, and a strong network of leading turbine and sensor manufacturers. On the contrary, a high focus on operational efficiency, safety standards, and predictive maintenance drives demand for advanced sensing solutions. Furthermore, ongoing investments in upgrading aging infrastructure and increasing deployment of flexible power systems further support market growth, while established service networks significantly enhance aftermarket demand across the region.

The U.S. held a Dominant share of the North America Aeroderivative Sensor Market in 2024

The United States holds the largest share of the aeroderivative sensor market, propelled by substantial investments in energy infrastructure and large-scale deployment of aeroderivative gas turbines in power generation and industrial applications. For instance, in May 2024, GE Vernova secured a major order in Tennessee to deliver turbines generating around 850 MW, demonstrating the increasing demand for reliable power. Additionally, the rapid growth of AI-powered data centers is increasing the need for reliable and adaptable power solutions, which in turn is promoting the use of turbines. The presence of major manufacturers and a strong focus on innovation further strengthen market leadership. Furthermore, extensive adoption of digital technologies and predictive maintenance solutions, along with strict safety regulations and continuous upgrades in power systems, is fueling demand for advanced sensor technologies nationwide.

Aeroderivative Sensor Industry Competitive Landscape

The global aeroderivative sensor market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, geographical expansions, and mergers and acquisitions.

Top Aeroderivative Sensor Market Companies

Some of the major players in the market are Bently Nevada (Baker Hughes), Honeywell International Inc., TE Connectivity, AMETEK.Inc., Danfoss, Conax Technologies, PCB Piezotronics, Inc. (Amphenol Corporation), Kulite Semiconductor Products, Inc., Kistler Group, and Collins Aerospace.

Recent Developments in the Aeroderivative Sensor Market

In May 2024, Teledyne’s OLCT 100‑XP‑MS detectors feature MEMS sensors, enabling precise multi‑gas detection, high reliability, and operational safety, enhancing aeroderivative turbine monitoring and industrial energy system performance in harsh environments.

In February 2024, I‑care launched the Wi‑care 130 G23 wireless vibration sensor, offering high‑precision triaxial measurements, three simultaneous analyses, longer battery life, and ATEX certification to enhance predictive maintenance and condition monitoring across industrial and energy equipment.

Global Aeroderivative Sensor Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 8.59% |

Market size 2024 | USD 337.87 million |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | The North America region is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, and India. |

Companies profiled | Bently Nevada (Baker Hughes), Honeywell International Inc., TE Connectivity, AMETEK.Inc., Danfoss, Conax Technologies, PCB Piezotronics, Inc. (Amphenol Corporation), Kulite Semiconductor Products, Inc., Kistler Group, and Collins Aerospace |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Sensor Type, By Service Provider, By End-User, and By Region/Country |

Reasons to Buy the Aeroderivative Sensor Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional level analysis of the industry.

Customization Options:

The global aeroderivative sensor market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global Aeroderivative Sensor Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global aeroderivative sensor market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the aeroderivative sensor value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global aeroderivative sensor market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including sensor type, service provider, end-user, and region within the global aeroderivative sensor market.

The Main Objective of the Global Aeroderivative Sensor Market Study

The study identifies current and future trends in the global aeroderivative sensor market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current and forecast market size of the global aeroderivative sensor market and its segments in terms of value (USD).

Aeroderivative Sensor Market Segmentation: Segments in the study include areas of sensor type, service provider, end-user, and region.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the aeroderivative sensor industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the aeroderivative sensor market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global aeroderivative sensor market’s current market size and growth potential?

The global aeroderivative sensor market was valued at USD 337.87 million in 2024 and is projected to grow at a CAGR of 8.59% from 2025 to 2033. Rising demand for gas turbines, high-precision monitoring solutions, and smart sensor technologies is fueling market expansion, making it a key investment opportunity for businesses in industrial, marine, aerospace, and energy sectors.

Q2: Which segment has the largest share of the global aeroderivative sensor market by sensor type?

Flame sensors currently hold the largest share of the global aeroderivative sensor market due to their critical role in gas turbine safety and efficiency. Their dominance is driven by growing demand in power generation, oil & gas, and aerospace industries, where precise flame detection ensures reliable operations and regulatory compliance.

Q3: What are the driving factors for the growth of the global Aeroderivative Sensor market?

Top growth drivers of the Aeroderivative Sensor market include:

• Increasing Demand for Gas Turbines Across Industries

• Increasing Demand for Efficient Monitoring Solutions Across Various Industries

• Growing Demand for Miniaturized and High-Precision Sensors

Q4: What are the emerging technologies and trends in the global Aeroderivative Sensor market?

Emerging trends in the Aeroderivative Sensor market include:

• Rising Adoption of Wireless and Smart Sensors

• Integration of IoT and AI in Sensor Technology

Q5: What are the key challenges in the global aeroderivative sensor market?

Key challenges in the aeroderivative sensor market include:

• High Development and Installation Cost

• Technical Limitations

Q6: Which region dominates the global aeroderivative sensor market?

North America dominates the global aeroderivative sensor market, driven by:

• Strong presence of key sensor manufacturers

• High adoption of advanced gas turbine technologies

• Substantial investments in industrial automation, aerospace, and energy sectors

• The region remains a strategic hub for R&D and market expansion.

Q7: Who are the key competitors in the global aeroderivative sensor market?

Top players in the aeroderivative sensor industry include:

• Bently Nevada (Baker Hughes)

• Honeywell International Inc.

• TE Connectivity

• AMETEK.Inc.

• Danfoss

• Conax Technologies

• PCB Piezotronics, Inc. (Amphenol Corporation)

• Kulite Semiconductor Products, Inc.

• Kistler Group

• Collins Aerospace

Q8: What investment opportunities exist in the global aeroderivative sensor market?

The aeroderivative sensor market presents lucrative investment opportunities due to growing adoption in power generation, oil & gas, aerospace, and industrial applications. Investors can capitalize on emerging trends such as wireless smart sensors, IoT-enabled monitoring, and high-precision sensor technologies. Expansion in APAC and increasing gas turbine installations globally also offer high-growth potential for stakeholders seeking long-term returns.

Q9: What are the future growth prospects and technology trends in aeroderivative sensors?

The future of aeroderivative sensors is shaped by advancements in AI, IoT, and wireless technology. Demand is rising for compact, high-accuracy sensors with predictive analytics capabilities. Key trends include digital twin integration, cloud-based monitoring, and enhanced safety compliance. Businesses investing in these technologies are positioned to achieve operational excellence, improve energy efficiency, and capture significant market share globally.

Related Reports

Customers who bought this item also bought

Aeroderivative Sensor Market: Current Analysis and Forecast (2025-2033)

Emphasis on Sensor Type (Temperature Sensors, Pressure Sensors, Vibration Sensors, Flame Sensors, and Others); Service Provider (OEMs and Aftermarket); End-User (Industrial, Marine, Aerospace & Defense, Power & Energy, and Oil & Gas); and Region/Country

Kamikaze Drone Market: Current Analysis and Forecast (2026-2034)

Emphasis on Type (Fixed-wing System and Rotary-wing System); Range (Short range(10-20km), Medium range(20-100km), and Long range(>100km)); Platform (Ground based, Airborne, and Naval); Autonomy (Man in the loop and Fully Autonomous); and Region/Country

Counter-Unmanned Aerial System Market: Current Analysis and Forecast (2025-2033)

Emphasis on Platform (Ground-Based Systems, Airborne Systems, and Naval / Maritime Systems); Technology (Radar, RF, EO/IR, Laser, Kinetic, and Others); End-Use (Defense & Military, Homeland Security & Law Enforcement, Critical Infrastructure, and Commercial & Industrial); and Region/Country

Middle East & Africa Turboprop Aircraft Market: Current Analysis and Forecast (2025-2033)

Emphasis By Aircraft Type (Light Turboprop Aircraft, Medium Turboprop Aircraft, and Heavy Turboprop Aircraft), by End-User (Government & Defense, Commercial Operators, and Private Operators), By Country (Saudi Arabia, UAE, Egypt, South Africa, Turkey, Israel, and the Rest of Middle East & Africa)