Space Sensors and Actuators Market: Current Analysis and Forecast (2025-2033)

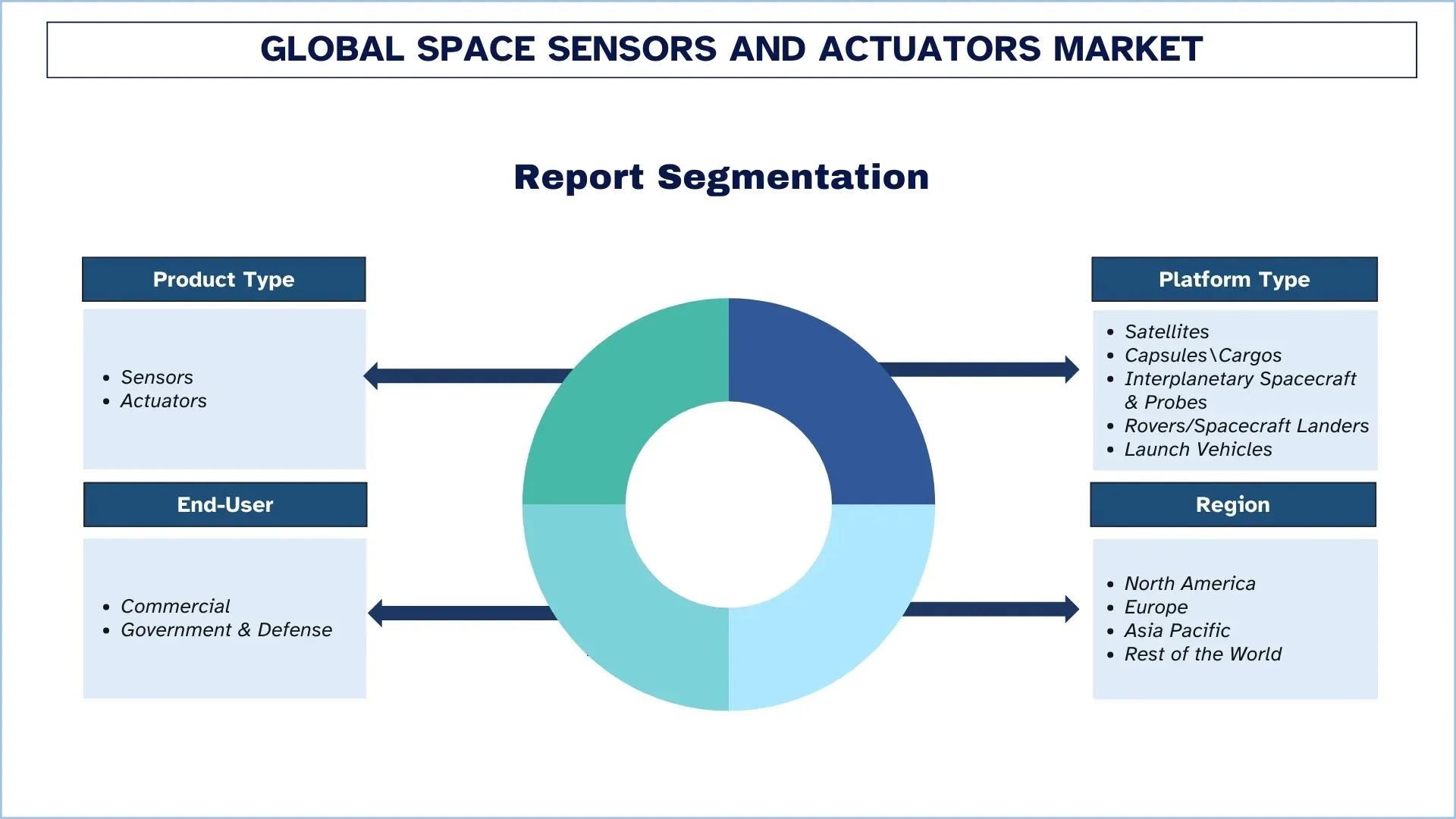

Emphasis on Product Type (Sensors and Actuators); Platform Type (Satellites, Capsules\Cargos, Interplanetary Spacecraft & Probes, Rovers/Spacecraft Landers, and Launch Vehicles); End-User (Commercial and Government & Defense); and Region/Country

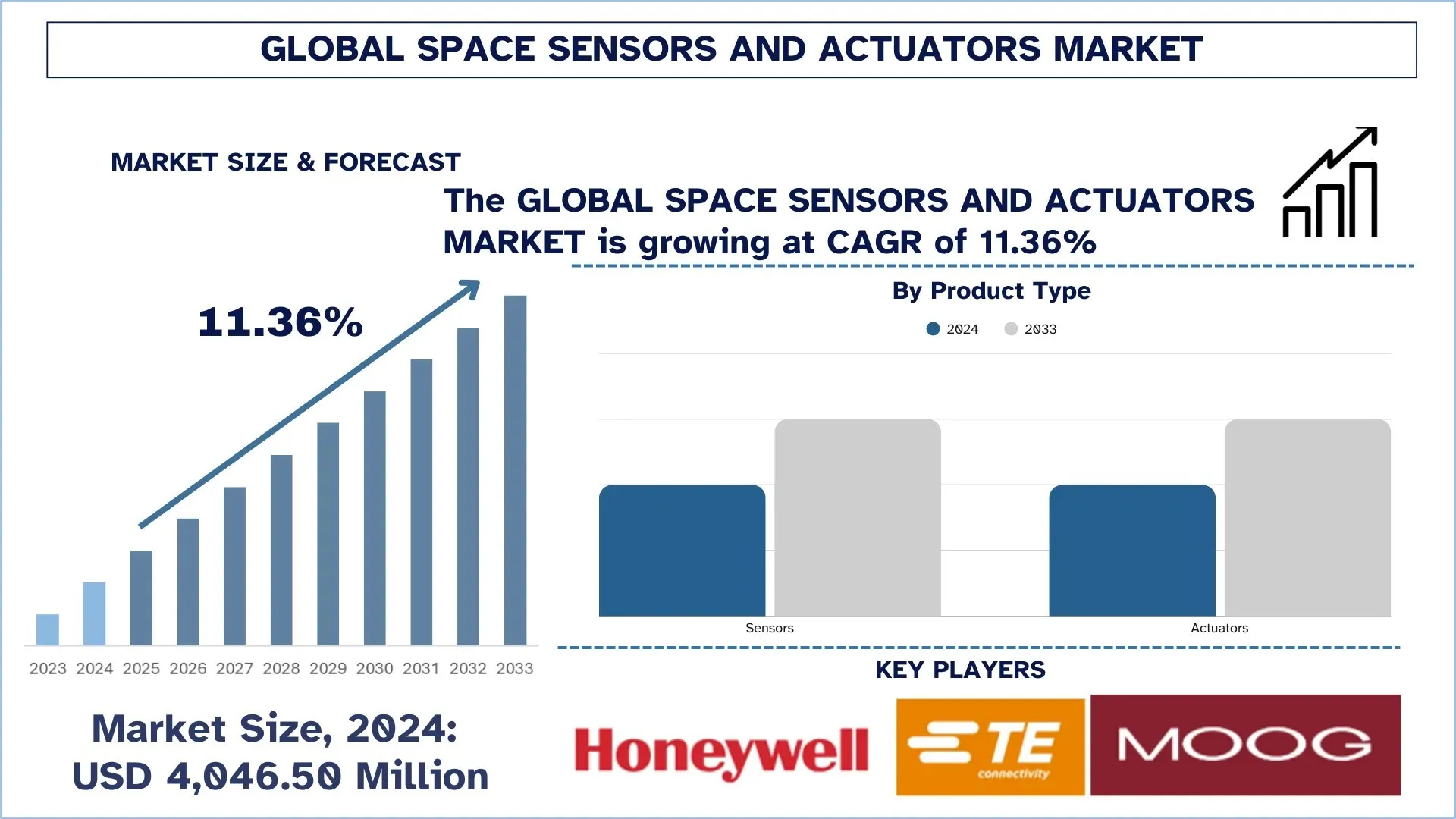

Global Space Sensors and Actuators Market Size & Forecast

The global space sensors and actuators market was valued at USD 4,046.50 million in 2024 and is expected to grow at a steady CAGR of around 11.36% during the forecast period (2025-2033F), driven by rising satellite deployments and increasing mission complexity, which are pushing demand for high-precision sensing and motion-control subsystems.

Space Sensors and Actuators Market Analysis

The space sensors and actuators market is experiencing robust growth worldwide, driven by an increase in the number of satellite launches and greater investment in space-based services across both commercial and government projects. The high-performance sensing and accurate motion-control components that spacecraft manufacturers are focusing on are aimed at enhancing the navigation, stabilization, and pointing accuracies of payloads, as well as the reliability of the entire mission. Moreover, other trends, including the rise of smallsat constellations, increasing the number of Earth observation applications, and increasing the rate of launch, are driving up demand. Suppliers are aggressively implementing mission-specific solutions, i.e., radiation-tolerant inertial sensors, star trackers, magnetometers, reaction wheels, and propulsion-related actuators, but are also focusing more on lightweight designs, miniaturization, and high durability. Meanwhile, the cost-effectiveness, legacy of qualification, and customization are also major differentiators, with vendors struggling to sustain various mission profiles and to meet the sustainability needs of long-term performance worldwide.

Global Space Sensors and Actuators Market Trends

This section discusses the key market trends that are influencing the various segments of the global space sensors and actuators market, as found by our team of research experts.

Miniaturization and SWaP-Optimized Sensor/Actuator Designs for Smallsats

The industry is becoming more CubeSat-based, where tighter size-weight-power (SWaP) constraints are required of it without compromising either pointing accuracy or quality. OEMs are also moving towards compact, integrated GNC/ADCS building blocks combining sensors, actuators, and onboard processing into one package to make integration simpler and hasten the production process- a direction NASA points out as one of the major state-of-the-art directions in small spacecraft development. This drive is reflected in recent product actions: in June 2025, Honeywell announced its HG3900 all-silicon MEMS IMU to provide tactical/near-nav capability in a smaller, lower-power package, and in September 2025, it unveiled a second-generation commercial Reaction Wheel Assembly to enable the realization of high-volume constellation operations at cost. In the flight hardware, component miniaturization is also apparent: ASPINA lists a CubeSat-sized reaction wheel with a mass of 71 g, and Teledyne has flown the Speedster HyViSI focal plane arrays on the NASA BlackCAT CubeSat launch in January 2026. Therefore, the miniaturization and SWaP-optimized sensor/actuator design for smallsats is seen as a key trend in the global space sensors and actuators market.

Space Sensors and Actuators Industry Segmentation

This section provides an analysis of the key trends in each segment of the global space sensors and actuators market report, along with forecasts at the global, regional, and country levels for 2025-2033.

The Sensor Segment Dominates the Global Space Sensors and Actuators Market

Based on the product type, the market is categorized into sensors and actuators. In 2024, sensors hold the largest share of the global space sensors and actuators market. They are required in nearly all spacecraft subsystems, as they facilitate navigation, attitude control, thermal control, power control, and payload control. Components such as star trackers, gyroscopes, sun sensors, magnetometers, and pressure/temperature sensors are common to all types of satellites, with sensor acquisition a core competency in new satellite construction and upgrades. Moreover, the rapid expansion of Earth observation and communication satellite constellations is increasing the number of sensors, thereby enhancing the growth of this segment.

The Satellites Market Dominates the Global Space Sensors and Actuators Market.

Based on the platform type, the market is categorized into satellites, capsules/cargos, interplanetary spacecraft & probes, rovers/spacecraft landers, and launch vehicles. The satellites constitute the largest portion of the world's space sensors and actuators market in 2024, with a very high number of deployments for communications, Earth observation, navigation, and defense missions. To provide fine pointing and station-keeping, satellite buses have large sensor suites to measure attitude, thermal control, and power, and actuators, such as reaction wheels, magnetorquers, and propulsion controls. In addition, the swift development of the LEO constellations and the growing replacement of aging fleets are increasing the segment's recurring demand, strengthening its position. In the meantime, the fastest growth is likely to be observed within the interplanetary spacecrafts and probes during the forecast period, which are facilitated by an increase in deep-space exploration programs and increased complexity in the missions. With the need for long-duration navigation, trajectory correction, and instrument pointing, these platforms demand high-quality and radiation-tolerant sensors and high-precision actuators, driving demand for advanced, mission-qualified components around the world.

Asia-Pacific Shows the Fastest Growing Region in the Global Space Sensors and Actuators Market

Asia-Pacific is becoming the region with the highest growth rate in space sensors and actuators as governments and commercial players accelerate their satellite deployments and increase domestic manufacturing and launch frequencies in several countries. The region's growth is being solidified by the race to deploy LEO broadband and Earth-observation capabilities that heighten the recurring demand for attitude determination sensors (star trackers, gyros, magnetometers) and actuators (reaction wheels, magnetorquers, propulsion controls) with high precision in new batches of satellites. In addition to the speed of mission in China, other fast-growing markets, like India, which is amassing private participation, with the help of industrial investments and policy-driven sectoral opening, are boosting local build-and-launch capacity. There is also growing regional cooperation evident, with Astroscale Japan's involvement with Indian space startups, and this can be considered a general ecosystem buildout that drives ongoing demand for subsystems.

China held a Dominant share of the Asia-Pacific Space Sensors and Actuators Market in 2024

China holds the largest share in the Asia-Pacific region because of its intense production of satellite constellations, growing constellation programs, and strong state support for spacecraft, payloads, and launch vehicles. Recent events show the magnitude and sustainability of such a demand: Reuters reported the launch of the first satellites of the Shanghai Spacecom constellation of a thousand sails (Qianfan/SpaceSail), highlighting ongoing pipelines of multi-launches that carry masses of sensors and actuators. China is also becoming more capable of launching larger bundles of satellites in space. Reuters has noted the launch of the Long March 8A, which can launch more satellites in a single mission to accelerate constellation deployment. China is already the center of space sensor and actuator demand in the region, as the country has recorded the highest year of launch activity and publicly indicated that it would continue targeting large constellations.

Space Sensors and Actuators Industry Competitive Landscape

The global space sensors and actuators market is competitive, with several global and international market players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, geographical expansions, and mergers and acquisitions.

Top Space Sensors and Actuators Market Companies

Some of the major players in the market are Honeywell International Inc., TE Connectivity, Moog Company, AMETEK, Inc., Texas Instruments Incorporated, Airbus, Safran, Collins Aerospace, RUAG Group (Beyond Gravity), and Analog Devices, Inc.

Recent Developments in the Space Sensors and Actuators Market

In June 2025, Moog Inc. opened a new space and defense facility in Elma, New York, expanding its production of spacecraft components and electromechanical systems. The site enhances Moog’s capacity for assembling and testing precision space actuation and control hardware.

In June 2025, BAE Systems and Hanwha Systems signed an MoU to co-develop a multi-sensor satellite system combining ultra-wideband RF sensors from BAE and synthetic aperture radar (SAR) technology from Hanwha.

In June 2025, the US Space Systems Command awarded BAE Systems a USD 1.2 billion contract to deliver 10 satellites in the Resilient Missile Warning and Tracking (RMWT) MEO Echo 2 program. The satellites will also have electro-optical/infrared sensors to monitor ballistic and hypersonic threats, and they will also have advanced onboard data processing and crosslink communication.

Global Space Sensors and Actuators Market Report Coverage

Report Attribute | Details |

Base year | 2024 |

Forecast period | 2025-2033 |

Growth momentum | Accelerate at a CAGR of 11.36% |

Market size 2024 | USD 4,046.50 million |

Regional analysis | North America, Europe, APAC, Rest of the World |

Major contributing region | The North America region is expected to dominate the market during the forecast period. |

Key countries covered | U.S., Canada, Germany, U.K., Spain, Italy, France, China, Japan, and India. |

Companies profiled | Honeywell International Inc., TE Connectivity, Moog Company, AMETEK, Inc., Texas Instruments Incorporated, Airbus, Safran, Collins Aerospace, RUAG Group (Beyond Gravity), and Analog Devices, Inc. |

Report Scope | Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Demand and Supply Side Analysis; Competitive Landscape; Company Profiling |

Segments Covered | By Product Type, By Platform Type, By End-User, and By Region/Country |

Reasons to Buy the Space Sensors and Actuators Market Report:

The study includes market sizing and forecasting analysis confirmed by authenticated key industry experts.

The report briefly reviews overall industry performance at a glance.

The report covers an in-depth analysis of prominent industry peers, primarily focusing on key business financials, type portfolios, expansion strategies, and recent developments.

Detailed examination of drivers, restraints, key trends, and opportunities prevailing in the industry.

The study comprehensively covers the market across different segments.

Deep dive regional level analysis of the industry.

Customization Options:

The global space sensors and actuators market can further be customized as per the requirements or any other market segment. Besides this, UnivDatos understands that you may have your own business needs; hence, feel free to contact us to get a report that completely suits your requirements.

Table of Content

Research Methodology for the Global Space Sensors and Actuators Market Analysis (2023-2033)

We analyzed the historical market, estimated the current market, and forecasted the future market of the global space sensors and actuators market to assess its application in major regions worldwide. We conducted exhaustive secondary research to gather historical market data and estimate the current market size. To validate these insights, we carefully reviewed numerous findings and assumptions. Additionally, we conducted in-depth primary interviews with industry experts across the space sensors and actuators value chain. After validating market figures through these interviews, we used both top-down and bottom-up approaches to forecast the overall market size. We then employed market breakdown and data triangulation methods to estimate and analyze the market size of industry segments and sub-segments.

Market Engineering

We employed the data triangulation technique to finalize the overall market estimation and derive precise statistical numbers for each segment and sub-segment of the global space sensors and actuators market. We split the data into several segments and sub-segments by analyzing various parameters and trends, including product type, platform type, end-user, and regions within the global space sensors and actuators market.

The Main Objective of the Global Space Sensors and Actuators Market Study

The study identifies current and future trends in the global space sensors and actuators market, providing strategic insights for investors. It highlights regional market attractiveness, enabling industry participants to tap into untapped markets and gain a first-mover advantage. Other quantitative goals of the studies include:

Market Size Analysis: Assess the current and forecast market size of the global space sensors and actuators market and its segments in terms of value (USD).

Space Sensors and Actuators Market Segmentation: Segments in the study include areas of product type, platform type, end-user, and region.

Regulatory Framework & Value Chain Analysis: Examine the regulatory framework, value chain, customer behavior, and competitive landscape of the space sensors and actuators industry.

Regional Analysis: Conduct a detailed regional analysis for key areas such as Asia Pacific, Europe, North America, and the Rest of the World.

Company Profiles & Growth Strategies: Company profiles of the space sensors and actuators market and the growth strategies adopted by the market players to sustain the fast-growing market.

Frequently Asked Questions FAQs

Q1: What is the global space sensors and actuators market’s current market size and growth potential?

As of 2024, the global space sensors and actuators market was valued at USD 4,046.50 million and is expected to grow at a CAGR of 11.36% from 2025 to 2033, driven by rising satellite deployments and increasing mission complexity, which are pushing demand for high-precision sensing and motion-control subsystems.

Q2: Which segment has the largest share of the global space sensors and actuators market by product type?

The sensor segment dominated the global market due to its critical role in attitude determination, navigation, thermal monitoring, and payload operations, enabling spacecraft performance across diverse mission platforms.

Q3: What are the driving factors for the growth of the global space sensors and actuators market?

Top growth drivers of the space sensors and actuators market include:

• Rising LEO Constellation Deployments and Replenishment Cycles

• Growing Defense Demand for Resilient Navigation and Precision Pointing

• Increasing Space Debris Mitigation Requirements and Mission Assurance Needs

Q4: What are the emerging technologies and trends in the global space sensors and actuators market?

Emerging trends in the space sensors and actuators market include:

• Miniaturization and SWaP-Optimized Sensor/Actuator Designs for Smallsats

• Shift Toward Autonomous Operations Using Advanced Sensing and Control

Q5: What are the key challenges in the global space sensors and actuators market?

Key challenges in the global space sensors and actuators market are:

• Long Qualification Cycles and High Reliability/Radiation Compliance Burden

• Supply-Chain Constraints and Long Lead Times for Space-Grade Components

Q6: Which region dominates the global space sensors and actuators market?

North America dominated the global space sensors and actuators market, driven by its deep, end-to-end space ecosystem from spacecraft primes and subsystem suppliers to test/qualification infrastructure and high-throughput manufacturing for LEO programs.

Q7: Who are the key competitors in the global space sensors and actuators market?

Top players in the space sensors and actuators industry include:

• Honeywell International Inc.

• TE Connectivity

• Moog company

• AMETEK.Inc.

• Texas Instruments Incorporated

• Airbus

• Safran

• Collins Aerospace

• RUAG Group (Beyond Gravity)

• Analog Devices, Inc.

Q8: How are spacecraft OEMs selecting suppliers for space sensors and actuators?

OEMs prioritize flight heritage, radiation tolerance, reliability data, SWaP performance, and qualification readiness, while also evaluating lead times, cost, and integration support for specific mission profiles.

Q9: How is procurement changing with the rise of LEO constellations compared to traditional missions?

Constellations are shifting demand toward standardized, high-volume components with repeatable quality and faster delivery, while traditional deep-space and defense missions continue to require customized, ultra-reliable hardware.

Related Reports

Customers who bought this item also bought

Aeroderivative Sensor Market: Current Analysis and Forecast (2025-2033)

Emphasis on Sensor Type (Temperature Sensors, Pressure Sensors, Vibration Sensors, Flame Sensors, and Others); Service Provider (OEMs and Aftermarket); End-User (Industrial, Marine, Aerospace & Defense, Power & Energy, and Oil & Gas); and Region/Country

Kamikaze Drone Market: Current Analysis and Forecast (2026-2034)

Emphasis on Type (Fixed-wing System and Rotary-wing System); Range (Short range(10-20km), Medium range(20-100km), and Long range(>100km)); Platform (Ground based, Airborne, and Naval); Autonomy (Man in the loop and Fully Autonomous); and Region/Country

Counter-Unmanned Aerial System Market: Current Analysis and Forecast (2025-2033)

Emphasis on Platform (Ground-Based Systems, Airborne Systems, and Naval / Maritime Systems); Technology (Radar, RF, EO/IR, Laser, Kinetic, and Others); End-Use (Defense & Military, Homeland Security & Law Enforcement, Critical Infrastructure, and Commercial & Industrial); and Region/Country

Middle East & Africa Turboprop Aircraft Market: Current Analysis and Forecast (2025-2033)

Emphasis By Aircraft Type (Light Turboprop Aircraft, Medium Turboprop Aircraft, and Heavy Turboprop Aircraft), by End-User (Government & Defense, Commercial Operators, and Private Operators), By Country (Saudi Arabia, UAE, Egypt, South Africa, Turkey, Israel, and the Rest of Middle East & Africa)